|

|

|

|

|

|

|

|

|

Daily Intelligence Briefing

|

|

|

|

|

|

|

|

|

|

|

|

|

Identifying Change-Driven Investment Themes – Five sections, explained here.

|

|

|

|

|

|

We bring you our Daily Intelligence Briefing courtesy of McAlinden Research Partners. The report is provided to Hedge Connection members for free. Below is snapshot, login to view the full report. Not a member? Join today. McAlinden Research Partners is offering a complimentary one-month subscription to receive the Daily Intelligence Briefing – to Hedge Connection clients/friends. Activate yours by contacting Rob@mcalindenresearch.com and mentioning “Sent by Hedge Connection”

|

|

|

|

|

|

|

I. Today’s Thematic Investment Idea

A deep dive into a market driver with alpha generating potential.

|

|

|

US Auto Market Slapped by September Meltdown →

|

|

|

Summary: US auto sales fell strongly in September, with a number of major brands experiencing double digit declines for the month. While foreign automakers bore the brunt of the data, General Motors and US auto suppliers are being wracked by the ongoing GM workers’ strike to the tune of millions of dollars per day. Additionally, inventories continue to build and auto loan terms are lengthening to record levels as affordability for middle-class buyers erodes. Read more +

|

|

|

|

|

|

|

|

|

|

|

|

II. Updates of Themes on MRP’s Radar

Follow-up analysis of key market drivers monitored by MRP.

|

|

|

|

|

|

|

Food & Beverage: How a 25% tariff on food and beverage from the EU will impact the US

|

|

|

Cannabis: Mexican Senate Leader Says Marijuana Will Be Legalized This Month

|

|

|

Banks: Half euro zone banks wouldn’t survive cash drought: ECB

|

|

|

Aviation SHORT: Southwest Airlines pilots sue Boeing over 737 Max grounding

|

|

|

Gold: China’s Gold-Buying Spree Tops 100 Tons During Trade War

|

|

|

Oil: Platts: OPEC Oil Production Falls Most In 17 Years After Saudi Oil Attacks

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

IV. Active Thematic Ideas

MRP’s active long and short themes, with an archive of follow-up reports.

|

|

|

See Them Here →

|

|

|

|

|

|

|

|

|

|

V. Macroeconomic Indicators

Key data releases relevant to MRP’s Active Thematic Ideas.

|

|

|

See Them Here →

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

THEME ALERT: AN ACTIVE MRP THEME

|

|

|

US Auto Market Slapped by September Meltdown

|

|

|

|

|

|

|

|

|

|

|

|

US auto sales fell strongly in September, with a number of major brands experiencing double digit declines for the month. While foreign automakers bore the brunt of the data, General Motors and US auto suppliers are being wracked by the ongoing GM workers’ strike to the tune of millions of dollars per day. Additionally, inventories continue to build and auto loan terms are lengthening to record levels as affordability for middle-class buyers erodes.

|

|

|

|

|

|

September was yet another downbeat month in the auto sector. Overall, light vehicle sales totaled 1,268,871 in the month, reflecting a 12% year-over-year decline. According to Cox Automotive, annual industry sales are 1.4% lower than in 2018 through the first nine months of the year.

MRP previously forecast a weak September for the auto sector, considering it had only 23 selling days (the fewest possible for a month) and excluded Labor Day, considered a part of August selling this year. However, automakers can’t entirely blame the calendar considering sales numbers for some of the largest auto brands still managed to dip below dreadful analyst estimates.

Toyota and Honda, for instance, saw sales fall 16.5% and 14.1% YoY vs expected declines of 11.9% and 4.6%, respectively. Even on a daily selling rate basis, as Bloomberg reports, total Toyota deliveries were down 9.2%. Lexus, a division of Toyota, saw the worst of the decline as sales crashed 23%. Nissan and Honda rounded out the September slump in Japanese-made auto sales sinking 17.6%, and 14%, respectively.

Even makes that had been on extended winning streaks saw their runs snapped in September. Hyundai had seen 13 consecutive months of YoY gains in their sales, but September sales fell 9.0%. Similarly, Subaru’s remarkable 93-month streak suffered the same fate as sales fell 9.4%.

The “Big 3” American automakers were more of a mixed bag, though. Ford, Fiat Chrysler Automotive (FCA), and General Motors (GM) now post only quarterly sales results instead of monthly, so it had been some time since investors got a look into actual sales figures. Zack’s Equity Research reports that Ford sales declined 4.9% in the third quarter while FCA saw deliveries come in just about flat with the previous year. GM broke from the trend as Q3 sales actually increased 6.3%.

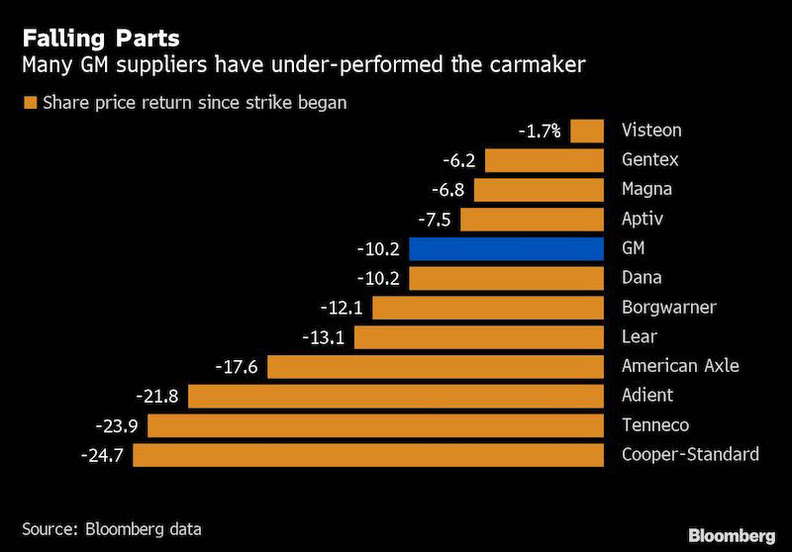

Despite the positive data, General Motors stock is down more than 10% since the close of trading on September 13, the Friday before the more than 46,000 GM employees represented by United Auto Workers (UAW) began a strike that is the longest since 1970 and still ongoing. Some had speculated that a resolution was nearing last week but, since a package of proposals the union presented on Saturday were rejected, “negotiations have taken a turn for the worse”, according to Terry Dittes, vice president and director of the UAW’s GM department. “They reverted back to their last rejected proposal and made little change,” he said. The strike has halted factory output at more than 30 GM plants in the U.S., stifled production for auto-parts suppliers and resulted n costs of anywhere from $50 – 100 million per day to GM as well as an additional $1 – 2 million for big suppliers like American Axle, Lear Corp, and Tenneco. Anderson Economic Group, cited by Barron’s, estimated GM’s cumulative lost profits would total $660 million through Sunday, and the longer the strike goes, the more daily costs increase.

While sales are slowing, inventories continue to burst at the seams. Days to turn, the average number of days a new vehicle sits on a dealer lot before being sold to a retail customer, expanded to 75 days through September 22., up one day from August, and 7 days from a year prior; a 60-to-65-day supply is considered healthy. With outgoing model-year vehicles clogging their lots, automakers had to pony up record incentives of more than $4,100 a vehicle in the third quarter, according to researchers at J.D. Power and LMC Automotive. Last month, MRP noted just 8% of new vehicles on dealership lots in early August were 2020 models, according to research site CarGurus.com. In the same month last year, the latest models accounted for 19% of overall inventory.

Although incentives are rising, they have failed to cancel out the persistently rising sticker prices. As a result, auto loan terms continue to lengthen. According to the Wall Street Journal, about a third of auto loans for new vehicles taken in the first half of 2019 had terms of longer than six years, and the average loan now stretches for a record 69 months, according to credit-reporting firm Experian PLC. A decade ago, that number was less than 10%. The median-income U.S. household with a four-year loan, 20% down and a payment under 10% of gross income—a standard budget—could afford a car worth $18,390, excluding taxes, according to an analysis by personal-finance website Bankrate.com. But the size of the average auto loan has grown by about a third over the past decade to $32,119 for a new car, according to Experian. Longer loan terms mean that consumers hold onto their cars longer or, as a third of new-car buyers who trade in their cars now do, roll debt from old vehicles into their new loans, according to car-shopping site Edmunds.

MRP has highlighted lengthening loan terms, underwater equity, and increasing subprime lending as negative drags on the auto industry over the last 2 years now, and these trends look set to continue as many Americans are having a very difficult time affording the cars they’re purchasing. Data from the Federal Reserve Bank of New York shows that subprime auto loan originations totaled $32.7 billion in the second quarter, a 3-year high, while USA Today reports the average buyer pays $920 in annual financing costs alone – namely, loan interest – which is up from $744 in 2018.

Additional headwinds persist for international automakers. Pressure from the US-China trade war, weakening economic conditions, and high costs of innovation for carmakers are now expected to cost the global industry nearly 35 million vehicle sales, worth a cumulative $770 billion, over the next 5 years, according to Germany’s Center for Automotive Research (CAR). CAR has estimated that global car and SUV sales will fall from a high of 84.4 million in 2017 to just 77.3 million in 2020. Another report, cited by Forbes, from S&P Global Ratings said the world’s light vehicle sales look set to fall by between 2 and 3% this year with virtually no growth between 2020 and 2021. Additionally, S&P expects annual light vehicle sales in China to fall 7%-9% this year. U.S. sales will slip 3% and decline up to 2% in Europe.

|

|

|

|

|

|

|

THEME ALERT

|

|

|

Due to the continuing negative trend of new vehicle sales around the world, as well as declining affordability and trade tensions taking a toll, MRP is reaffirming its Short Autos theme. Investors can gain exposure to the theme via the First Trust NASDAQ Global Auto ETF (CARZ). Since we launched the short theme on October 12, 2017, CARZ has declined 25% versus a 15% rise in the S&P 500.

|

|

|

|

|

|

|

|

|

|

|

|

Autos (CARZ) vs S&P 500 (SPY)

|

|

|

|

|

|

|

|

|

|

|

|

|

Source material for today’s market insight…

|

|

|

|

|

|

|

|

|

|

|

|

Autos

The Seven-Year Auto Loan: America’s Middle Class Can’t Afford Its Cars

Car loans that are increasingly stretched out are a pronounced sign that some American middle class buyers can’t afford a middle-class lifestyle. Just 18% of U.S. households had enough liquid assets to cover the cost of a new car, according to a Wall Street Journal analysis of 2016 data from the Fed’s triennial Survey of Consumer Finances, a proportion that hasn’t changed much in recent years.

Even a conservative car loan often won’t do it. The median-income U.S. household with a four-year loan, 20% down and a payment under 10% of gross income—a standard budget—could afford a car worth $18,390, excluding taxes, according to an analysis by personal-finance website Bankrate.com.

Last year, investors bought a record $107 billion of bonds backed by cars, according to the Securities Industry and Financial Markets Association, a trade group. That is the first issuance record since 2005 and nearly triple the amount two decades earlier.

The outstanding pile of auto bonds swelled to a record $264 billion. So far this year, dealerships made an average of $982 per new vehicle on finance and insurance versus $381 on the actual sale, according to J.D. Power, a data and analytics company. A decade earlier, financing brought in $516 per car and the sale made dealers $837.

Read the full article from The Wall Street Journal +

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Autos

Why buying a new car is more expensive than ever

AAA’s annual cost-of-car-ownership study, released Thursday, found that a 24% increase in average financing costs on new cars contributed to a 4.9% overall increase in the expense of owning a new vehicle.

Altogether, it costs the average American about $9,282 per year, or $773.50 per month, to own a new vehicle when factoring in fuel, maintenance, depreciation, insurance and borrowing costs, according to AAA. That’s up from $8,849 in 2018.

The average amount borrowed per new vehicle purchased in August was $32,590, up 5.2% from a year earlier.

Read the full article from USA Today +

|

|

|

Autos

GM strike ripples across economy, raising new recession fears

Eighty-five tractor trailers full of hoods, bumpers and other assorted parts sat, unloaded, in Lansing, Michigan, this week — more evidence of the cost of the General Motors Co. strike that has shut down most of its North American plants and idled 46,000 workers.

The automaker itself has already lost more than $1 billion in earnings before interest and taxes, according to one analyst estimate. GM’s bigger parts suppliers are losing as much as $2 million a day by the same measurement. Workers at smaller parts makers across the U.S. are sending employees home.

The walkout has forced American Axle & Manufacturing Holdings Inc. to lay off workers at its largest driveline plant in the U.S. The company, which was spun off from GM in 1994, still relies on the automaker for 39% of its revenue. CEO David Dauch told Bloomberg last week his company may adjust its full-year earnings outlook if the strike continues for “an extended period of time.” Its stock has fallen 18% since the labor action began on Sept. 16.

Read the full article from Crain’s Chicago Business +

|

|

|

|

|

|

Autos

U.S./China Tariff War Will Lose Auto Industry Sales Worth $770 Billion: Report

Auto sales are coming under huge pressure from the tariff war between China and the U.S. and the global industry will lose sales over the next 5 years worth nearly $770 billion because of this and other problems, according to Germany’s Center for Automotive Research (CAR).

“In the worldwide car (and SUV) market in the years 2018 to 2024 cumulative sales slumps of more than 35 million vehicles worth 700 billion euros ($769 billion) will have to be absorbed. A good 80% of the losses accrue to China,” CAR director Professor Ferdinand Dudenhoeffer said.

CAR’s Dudenhoeffer said President Trump’s tariff wars are destroying national wealth in Europe, particularly Germany’s. The huge loss of sales means there will be a significant withdrawal of capital from the industry, which will make it more difficult to meet the high costs of electrification. Dudenhoeffer said German manufacturers should reach out to China and build up contacts which will secure the industry’s prosperity.

Read the full article from Forbes +

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Select a theme to see when and why we added it. Also included is a link to all recent Market Insight reports we’ve written about that theme, allowing you to track its progress.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

US Consumer Credit Beats Expectations

Consumer credit in the United States went up by USD 17.9 billion in August 2019, beating market expectations of a USD 15.3 billion rise. Revolving credit including credit card borrowing declined USD 2 billion, following a downwardly revised USD 9.4 billion climb in July. In addition, non-revolving credit including loans for education and automobiles rose USD 19.9 billion, after an upwardly revised USD 13.7 billion increase in the previous month.

Year-on-year, consumer credit growth moderated to 5.2 percent in August from 6.7 percent in July

Click here to access the data +

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

United Kingdom House Price Index Slows

The Halifax House Price Index in the UK rose 1.1 percent year-on-year in the three months to September 2019, slowing from a 1.8 percent gain in the previous month and below market expectations of 1.6 percent. It was the weakest annual house price growth since the three months to April 2013.

Click here to access the data +

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Brazil New Vehicle Registrations and Exports Down MoM

New vehicle registrations in Brazil fell 3.3 percent over a month earlier to 235 thousand units in September 2019, after a 0.3 percent drop in August. Meantime, exports of vehicles went down 0.2 percent to 37 thousand.

Year-on-year, new vehicle registrations jumped 10.1 percent while exports slipped 7.1 percent.

Considering the first nine months of the year, new vehicle registrations surged 9.9 percent to 2.0 million units while exports declined 35.6 percent to 338 thousand units.

Click here to access the data +

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mexico Gross Fixed Investment Falls for Sixth Straight Month

Gross fixed investment in Mexico fell 7.6 percent year-on-year in July 2019, following a downwardly revised 8.7 percent decline in the previous month. It was the sixth consecutive monthly decrease in private investment.

Click here to access the data +

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Germany Factory Orders Decline More than Expected

Germany’s industrial orders dropped 0.6 percent from a month earlier in August 2019, compared to market expectations of a 0.3 percent decline and following a revised 2.1 percent plunge in July. The decline was mainly due to a 2.6 percent fall in domestic demand, while foreign orders grew 0.9 percent, boosted by demand from both the Euro area (1.5 percent) and other countries (0.4 percent).

Click here to access the data +

|

|

|

|

|

|

|

|

|

|

|

|

MARKET INSIGHT UPDATES: SUMMARIES

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Food & Beverage

How a 25% tariff on food and beverage from the EU will impact the US

Starting Oct. 18, the Trump administration plans to place 25% import tariffs on $7.5 billion worth of foods and beverages from the European Union. The final product list from the Office of the U.S. Trade Representative includes single-malt whiskey, olives, butter, cheese and olive oil. Most of the tariffs will be on products from France, Germany, Spain and the United Kingdom, the USTR said in a release.

“The increased costs to consumers on imported foods will be dramatic,” The Specialty Foods Association said. “The cheese/charcuterie board that currently cost you $45 will put you back $60 after tariffs.” Almost $3.4 billion in imports is about to be affected by tariffs on Scotch whiskey, liqueurs and wine, the group said, and 13,000 jobs could be lost.

The U.S. beef industry might also be nervous. In August, the U.S. and the EU agreed to nearly triple the annual amount of duty-free, hormone-free U.S. beef allowed into the EU during the next seven years. That deal still needs approval from the European Parliament, which may be tougher to achieve with these new tariffs in place.

Read the full article from Food Dive +

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cannabis

Mexican Senate Leader Says Marijuana Will Be Legalized This Month

The Senate leader of Mexico’s ruling party said that the lawmakers will vote on a bill to legalize marijuana for adult use by the end of the month.

Last year, the court ruled that the country’s ban on personal possession, use and cultivation of marijuana was unconstitutional and said the government must formally legalize those activities by October. Many key lawmakers have said the country should go even further by legally regulating cannabis sales and production as well.

Mario Delgado Carrillo, the coordinator of the MORENA party’s bench in the Chamber of Deputies, filed legislation to legalize and regulate cannabis last week, but he proposed having the government run the market to prevent large marijuana firms from monopolizing the industry. Neither Monreal nor President Andrés Manuel López Obrador are in favor of having a state-controlled cannabis program, however, according to El Universal. And Carrillo later clarified that his bill was designed to reflect a personal preference. Monreal said that he’s willing to incorporate certain ideas from the lawmaker’s proposal, however.

Read the full article from Marijuana Moment +

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Banks

Half euro zone banks wouldn’t survive cash drought: ECB

The ECB’s test of 103 lenders laid bare some weak spots in the euro zone’s banking system at a time of growing fears about an upcoming recession and upheaval in the U.S. money market. It showed that four banks wouldn’t survive six months if they were frozen out of the wholesale funding market and 52 would go under within six months if financial counterparties and some commercial clients took their money out.

Several banks had to re-state their liquidity levels following the ECB’s check, which will now be used by supervisors as part of their assessment.

Read the full article from Reuters +

|

|

|

|

|

|

|

|

|

|

|

| There is much more to this report! McAlinden Research Partners offers Hedge Connection members weekly access to the Daily Intelligence Briefing research for free – click here to view. (You must be logged in first). Not a member? Join today. McAlinden Research Partners is offering a complimentary one-month subscription to receive the Daily Intelligence Briefing – to Hedge Connection clients/friends. Activate yours by contacting Rob@mcalindenresearch.com and mentioning “Sent by Hedge Connection” |

|

|

|

Leave a Reply