|

Headwinds Plaguing Solar Industry as Renewables Slide

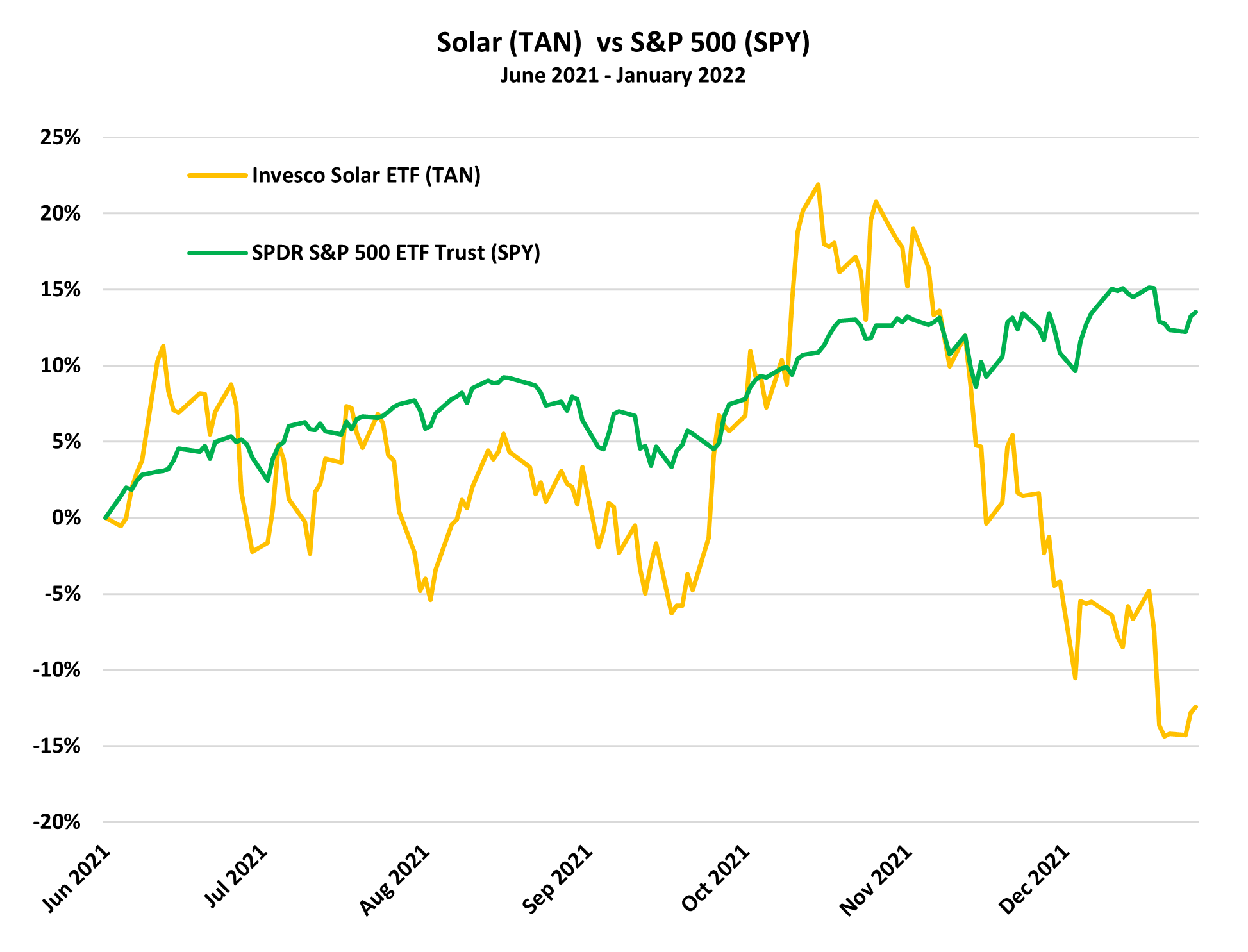

Supply chain disruptions hampering economies across the globe have certainly taken a toll on the solar industry as raw material shortages and higher costs proved to stick around over the last few months.

According to Solar Industry Mag, trade policy uncertainty in Asian countries including Malaysia, Thailand and Vietnam have created significant shipping disruptions for importers. Petitions for anti-dumping and countervailing duties on solar cells were recently dismissed, which have sparked further logistical challenges and subsequent price increases.

Near-term solar deployment has been strained by the fact costs have risen across all market segments, writes the Solar Energy Industries Association. A major contributor to rising costs has been the price of polysilicon through 2021, a key raw material used to make photovoltaic cells in solar panels.

Polysilicon prices have more than tripled since bottlenecks began, rising over 200% in 2021 and slowing the pace of renewables projects.

Further, some investors have been spooked by new rules proposed by the California Public Utilities Commission (CPUC) which essentially reduces payments granted to solar customers for the excess solar power they generate. This incentive program has been an integral part of the renewable energy transition in California, in which there are more than 1.3 million solar customers.

Per CNBC, solar companies and advocacy groups have sounded the alarm, saying reduced subsidies could significantly dampen the growth of solar energy, as it not only reduces payments but adds additional monthly charges for customers. The CPUC holds the stance this new policy modernizes California’s rooftop solar program and allows lower income customers to access to clean energy.

Similarly, on a macroeconomic front, the looming threat of rising interest rates have taken a toll on high growth industries, especially capital-intensive solar stocks. OilPrice.com reports that higher interest rates can put pressure on renewable energy projects due to the amount of capital that is often funded with debt, leading some investors to shun growth companies in favor of defensive value plays.

However, most, if not all of these headwinds have the potential to be temporary setbacks and could turn around at the start of the new year.

Solar Sell-Off Looks Overdone as Difficulties Expected to Subside

Despite recent troubles, the solar slump appears overdone, and the sector could be primed to stage a comeback in the first half of 2022.

Wood Mackenzie recently predicted that the supply chain problems that drove up the cost of solar power equipment last year will ease throughout 2022.

As previously mentioned, polysilicon prices surged last year and were a key factor in slowing new utility scale solar projects. Fortunately, Bloomberg reports those struggles are going to be fixed, clearing the way for a renewed boom in clean energy technology.

China is currently spending billions on new factories to produce polysilicon, and global capacity has already improved by more than 25% just in the last two months. Bloomberg notes global polysilicon production will double by the beginning of 2023, which should certainly help depress runaway raw material prices.

Tony Fei, analyst with BOCI Research Ltd., has said China’s multi-billion dollar expansion will help remove a key bottleneck in the solar value chain, noting that solar panel supply will be vastly boosted in the coming years. Polysilicon prices have already fallen roughly 16% from early December, showing improved manufacturing capacity could be beginning to pay off.

Regarding California’s controversial proposal that would enact dramatic changes for rooftop solar users, Governor Gavin Newsom recently said the state still has work to do. The San Diego Tribune reports that Newsom was quoted saying he believes changes need to be made to the proposal, opening the door for potential amendments to ensure the growth of solar power.

Further, rising interest rates have certainly sent investors running towards value stocks, yet Bloomberg notes that analysts from Goldman Sachs and UBS believe equities may ultimately weather higher interest rates and resume their rally. JP Morgan and Blackrock analysts said this week that it is time to buy the “arguably overdone” dip, which could benefit high growth stocks like solar whose valuations were crushed over the last two months.

All in all, the recent setbacks for solar stocks appear overblown and are expected to subside in 2022. Additionally, projections for solar investment and installations are projected to remain high next year.

2022 Projections Look Promising for Solar Energy Development

A November report from the Clean Energy Technology service at IHS Markit predicts global solar PV installations to rise more than 20% in 2022, with more than $170 billion invested into the sector next year.

Similarly, CleanTechnica projects utility-scale solar generating capacity to grow by 21.5 GW in 2022, which would account for nearly half of all new US electric generating capacity next year.

Conversely, Wood Mackenzie lowered their 2022 forecast for US solar capacity by 7.4 GW to 22.2 GW, a 25% decrease, citing supply chain pricing challenges. However, the company recently put out a note that predicts solar supply chain struggles to ease throughout the year which could offset near term setbacks.

Meanwhile, the Build Back Better Act muddies the water for these projections as if it were to pass, could add 44 GW of solar power capacity over the next four years, presenting a massive growth opportunity for solar companies. And while Wood Mackenzie has lowered their growth projections, the solar industry just installed 130,000 systems in Q3, a record high for one quarter, amid the same supply disruptions and price increases cited by the energy research & consultancy firm.

Solar energy still has a clear path forward as clean energy continues to take center stage and renewable energy capacity is increasingly expanded. Despite the recent pullback, solar installations should continue to climb and play a crucial role in the clean energy transition. |

Leave a Reply