By Daniel McConvey, Rossport Investments LLC

I am neutral to mildly cautious on gold prices at current $1700 levels for the rest of this year. However, I am constructive on gold after 2023 and I am positive on gold developer company stocks over the next three to five years at current levels. I should note that my bias on gold has tended to be too conservative during my three decades in the gold investment space.

My Thoughts on Gold

Low interest rates and Quantitative Easing (“QE”) were good for gold during most of the first two years of Covid. Now central bank moves to aggressively raise interest rates and unwind QE are bad for gold. Headwinds are added by the stronger US dollar and the stress on emerging market consumer pocketbooks. In fact, our bearish worry is that we see some similarity now to the markets of the Asian Currency Crisis of 1996-1999 when emerging markets cratered, some Asian countries had material negative gold demand, several central banks sold gold, and gold producers sold gold forward. All this sent gold on its way to 20 year lows. While we don’t expect this storm to reoccur, some elements of it might. We think that emerging market economies will continue to be hit hard by higher interest rates, fuel prices and food prices that will reduce gold offtake in those countries.

However, offsetting these headwinds in these abnormal times are a number of factors that could generate a rebound in gold prices. First, global geopolitical instability is growing with Russia’s attack on the Ukraine that is rocking the global order. Second, emerging market turmoil may not be all bearish for gold. There is currently a financial crisis in Sri Lanka caused at least partly by the increase in debt, fuel and food costs. I think there is a good chance of more of these crises occurring in other emerging market countries with limited help from a distracted western world. It could even happen in European countries stressed by gas shortages. While, as noted, these economic crises would hurt local gold demand, it may shake confidence in fiat currencies and increase gold buying in the western world. Third, US midterm elections bring uncertainty after the chaos of the last US elections that raised worries about America’s commitment to democracy. Fourth, western sanctions that have frozen Russian owned US dollar assets have increased the appeal for many of owning gold. Fifth, while I think the dollar will continue to strengthen this year, I think it will weaken from these strong levels starting sometime in 2023. Finally, sixth, some western central banks’ credibility may be questioned if they find it difficult to raise interest rates at the same time their governments are handing out subsidies. Credibility is not a word I recall having heard used in decades in describing the US Federal Reserve or the ECB. Suddenly I am hearing it a lot. A loss of central bank credibility amounts to a loss in confidence in fiat currency which would be very bullish for gold and gold equities.

The Opportunity with Gold Developers

I believe analyzing Gold Mining Projects is my greatest strength and I think that currently there are opportunities in the gold developers space. I define gold developers as companies focused on delineating, permitting, financing, and building a mine. I think there is currently a greater than usual number of good quality gold developers who have projects that are likely to become mines. Gold developers share prices have been decimated year to date and are now, on average, trading at 50% of their NAV or less according to broker estimates. Part of the reason for their share price drop, besides the fall in the gold price, is the material increase in, and uncertainty concerning the capital cost estimates to build the mining projects. This is a legitimate worry. Building gold mines is capital intensive. Current forecast NPV projections based on spot gold prices are significantly less robust than they were a year ago. There is a significant risk that the projects the developers own don’t get built, don’t get bought out by a major gold mining company, or don’t make robust returns if they are built by the current owners. However, taking a longer term view, I think it is likely that a combination of more robust gold prices and a rebound in confidence in cost estimates will make many projects robust.

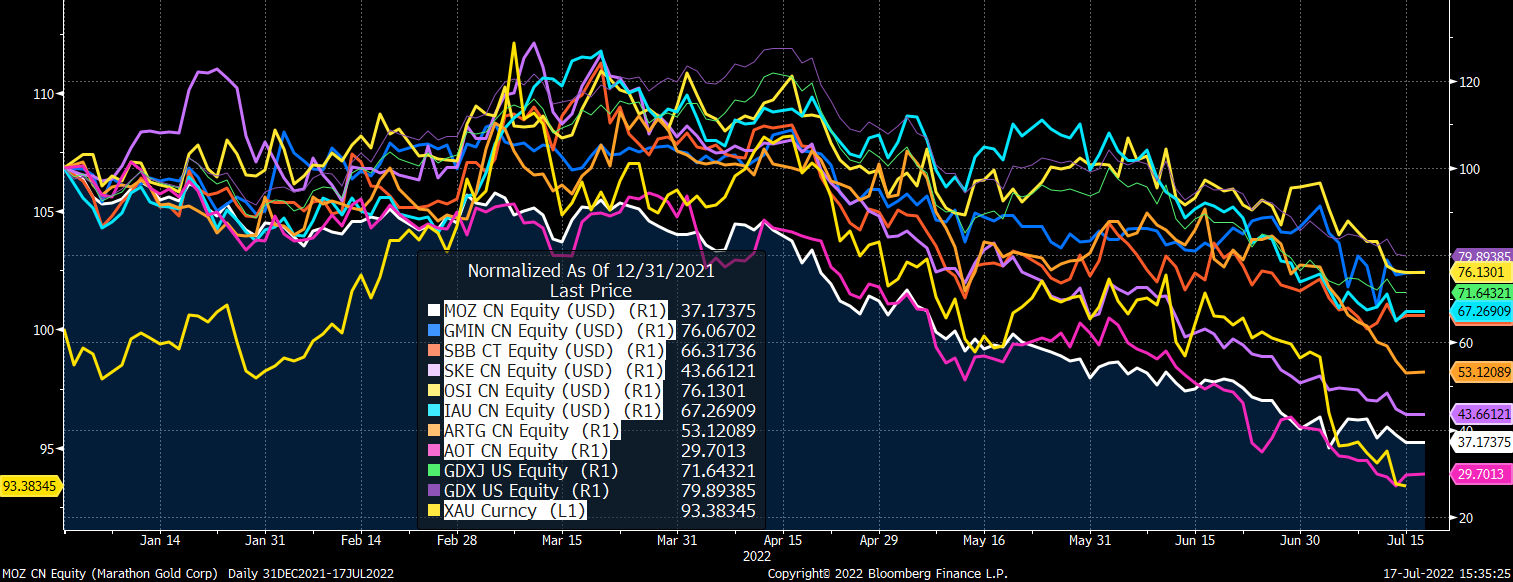

Gold, the Van Eck GDX and GDXJ Mining Indexes and Eight Gold Developers YTD to July 15

Looking at the above graph, year to date gold prices through July 15 were down about $120/oz or 7%. $100 of that downdip has happened since June 30. Major gold company stocks as represented by the Van Eck GDX index are down 20% equal to the drop in the broader MSCI World Metals & Mining Net Total Return Index. Junior gold producers, who are a major focus for us, as represented by the Van Eck GDXJ index are down 28%. There is no index for gold developers. However, the average of the eight advanced gold developer stocks (the 1st 8 tickers on the legend) in the above graph are down about 44% and some have been crushed. I hope to visit two of these developers this summer. Importantly, all eight of these developers are of good to very good quality in our view and, of key importance, are either permitted or expected to be permitted in the next roughly two years. If I am right in my optimism concerning future gold mining economics, owning a basket of these stocks should generate attractive returns over the next three to five years.

Rossport Investments LLC specializes in the metals and mining sector. If you would like more information on our work and views, please contact Daniel McConvey at (908) 578-0840 or by email at daniel.mcconvey@rossport.com.

Note: Past performance is not necessarily indicative of future results. Forward-looking statements reflect the Investment Manager’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond the manager’s control. Investors are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document.

Leave a Reply