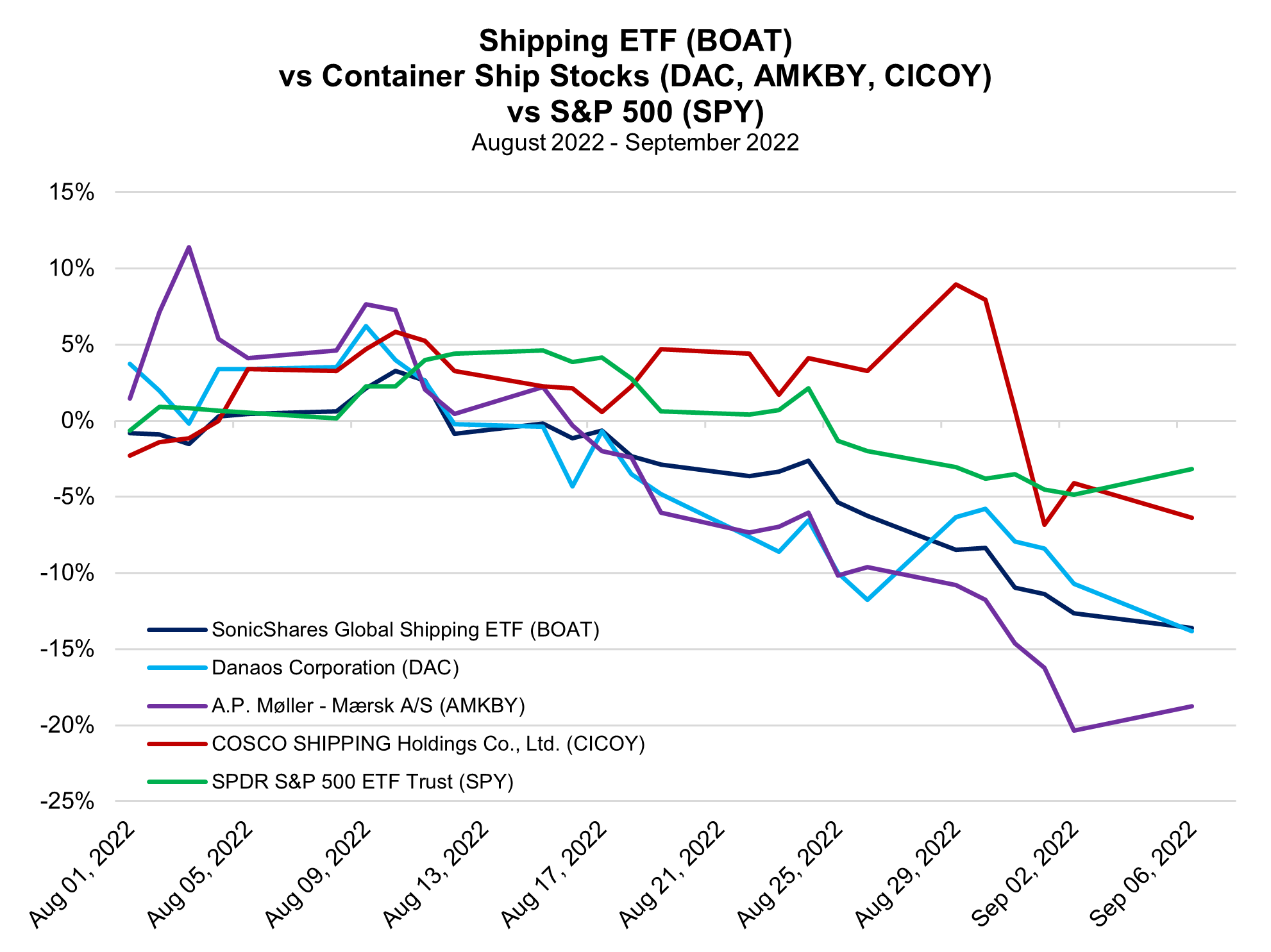

|

The second quarter of 2022 yielded another round of massive financial gains for container shipping, marking a seventh consecutive quarter of record high income for the industry. The quarter’s $63.7 billion was up $35.1 billion, equivalent to 123%, from the same period last year. The sustainability of that trend is now coming into question, however, as shipping rates are beginning to slide amid weakening trade flows in and out of key markets like the US and China.

As The Wall Street Journal notes, the cost to ship a 40-foot container from China to the US West Coast stands around $5,400 per box, down 60% from January, according to the Freightos Baltic Index (FBX). A container shipped from Asia to Europe costs $9,000, 42% less than at the start of the year.

Freightos’s website shows its Global Container Freight Index peaked around $11,100 in September 2021, but has now dipped to below $5,300. The boom in rates through 2020-2021, along with the spate of record profits, spurred a shipbuilding splurge by container shippers. That is likely to play a role in tamping down on those rates.

Container fleets are growing more quickly than they have in some time, expanding the scarce space available aboard ships. In June, the order book for container ships became larger than both the tanker and bulker orderbooks in deadweight tonnage (DWT) for the first time ever, notes Clarksons Research. Additionally, The Maritime Executive reports shippers like MSC, Hapag-Lloyd, and ONE are going bigger than ever with their new orders, now planning the introduction of their first 24,000 twenty-foot equivalent unit (TEU, a measure of how approximately how many twenty-foot containers can be transported) vessels.

The container fleet orderbook is now equivalent to 28% of on-the-water capacity, according to Clarksons. “Over the upcoming 24 months, we clearly see that supply growth will outpace demand growth,” said Hapag-Lloyd CEO Rolf Habben Jansen last month, addressing rising ship orders on an analyst call.

It hasn’t helped that demand from some of the most critical shipping markets is simply starting to slump.

Per CNBC, the World Trade Organization’s (WTO) latest Goods Trade Barometer shows the volume of world merchandise trade has plateaued. Annual growth for the first quarter of the year slowed to 3.2%, down from 5.7% in the final quarter of 2021.

Part of that can likely be chalked up to rising inventories relative to sales dampening the need for more orders from some of the largest retailers in the US. The overall inventory to sales ratio for retailers reached its highest level since February 2021 in June. However, if you narrow that down to general merchandise retailers, which includes big box and department stores like Walmart, Target, and Macys, their inventory to sales ratio has jumped to a more than 15 year high in recent months.

On the surface, the latest US trade data looks pretty good – but a closer look shows the country is likely experiencing a slowdown in international demand for its goods, as well as a weakening of consumer demand at home. According to data from the Bureau of Economic Analysis (BEA), the US’s trade deficit narrowed by $10.2 billion to $70.7 billion in July. That was the thinnest trade deficit since October 2021. Total exports managed to grow 0.2% MoM to a new all-time high of $259.3 billion as a rise in exports of services offset a decline in goods shipments. However, that increase in exports was the smallest since January. More importantly, imports declined -2.9% to $329.9 billion.

It makes sense that export growth would slow, given relentless strength in the US Dollar throughout 2022, which makes US exports more expensive for foreign buyers, but the pace at which it has declined points toward a flatlining or maybe even negative readings in the months ahead.

The downturn in import growth is counterintuitive, considering a stronger USD makes foreign goods cheaper for American buyers and should bolster import demand under normal conditions. With the US having already experienced contraction in gross domestic product (GDP) over each of the last two quarters, a downturn in imports of international goods is the latest sign that consumer demand is beginning to wane.

Per the National Retail Federation’s (NRF) Global Port Tracker, US ports covered by the NRF handled 2.18 million TEU in July. That was down -3.1% from June and -0.4% YoY, only the third annual decline in the last two years and the first since December 2021. The tracker’s projected numbers for the rest of the year, highlighted by Just Style, indicate each month for the rest of 2022 will experience YoY declines. Total shipments for the second half of the year are expected to total 12.6 million TEU, which would indicate a -3.1% plunge YoY.

The latest data from China’s General Administration of Customs showed the country’s exports and imports lost momentum in August. Exports rose just 7.1% YoY, down from an 18.0% gain in July, the first slowdown since April. On a monthly basis, outbound shipments actually declined by -5.4%, their first downturn since January. Per Reuters, inbound shipments rose just 0.3% in August from 2.3% in the month prior, well below a forecast 1.1% increase and the slowest pace of import growth in four months.

A whirlwind two years for shipping, characterized by backlogs, port congestion, and massive trade flows around the world is likely coming to an end due to global economic headwinds and new ship supply gradually entering service. Profits may remain elevated for a while, given the fact that demand is just starting to cool off, but a more sustained downturn would undoubtedly have a more profound negative impact on the shipping industry. |

Leave a Reply