Contributed by Pulak Sinha, Founder and CEO of Pepper

‘Network Effects’ is the defining phenomenon representing the modern digital economy. With the growth and dominance of the FAANG (Facebook, Apple, Amazon, Netflix and Google) stocks over the last 2 decades, Network Effects have been identified as the overwhelming creator of value in the economy. They have propelled companies to grow exponentially, leapfrog competition, create defensible moats and dominate entire economic segments.

Most people intuitively grasp the advantages of strong networks. The economic theories underpinning these effects are recent in origin but provide a fascinating view of how organizations of the future can compete in the future.

For example, the Netflix platform has very strong indirect network effects. The more movies and TV shows on the platform, the more subscribers value the service. Users need to feel like they are getting access to high quality, new and exclusive content in order to see value in the product. Because of this, in 2018, Netflix plans to spend $8 billion dollars on content in order to secure high quality and exclusive content from providers.

This article discusses this phenomenon What are Network Effects? Why is it important that investment managers leverage this effect to build their franchises? How would they go about it?

What is a Network Effect?

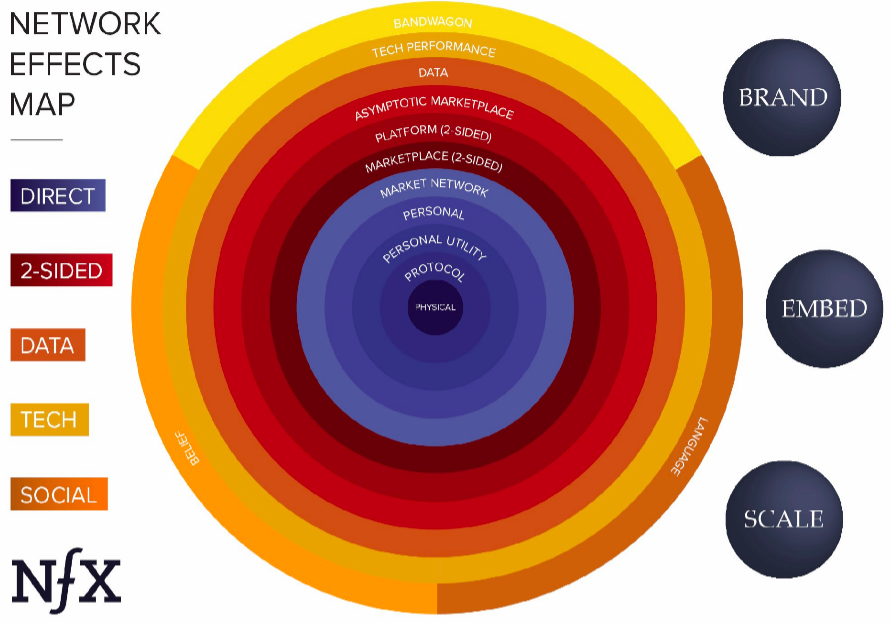

There are many definitions on what constitutes Network effects. The famed financial strategist and thinker Michael Mauboussin has put it the best:

“A network effect exists when the value of a good increases because the number of people using the good increases. All things being equal, it’s better to be connected to a bigger network than to a smaller one. Adding new customers typically makes the network more valuable for all participants because it increases the probability that everyone will find something that meets their needs.”

Put simply, the sum of the whole is way bigger than the individual parts. As more people join the network with more goods and services, the value of the network grows exponentially.

The Economics of Network Effects

In this extremely interesting case study done over the past 23 years, network effects have accounted for approximately 70% of the value creation in tech.

In this wide-ranging study over 334 companies, started since 1994, that went on to become over 1 BN started since 1994 were part of this study.

Microsoft’s Excel, Apple’s ioS, Google’s many platforms, Uber and many other have provided case studies on how networks have been built and leveraged to add value to both the supply side and demand side of products and services. Companies that can leverage networks can grow exponentially.

How Investment Managers Can Build their Own Networks

Complex networks exist in every business. They are simply not formalized using a technology platform. The Investment Manager already works with a network of partners, investors and service providers. This is akin to Network Effects with Local actions, which is another well studied phenomenon. Between these external resources the investment manager can:

● Source new deals

● Structure the deals

● Price the Deal

● Finance the deals

● Manage the deals

● Raise new capital

● Investment monitoring

In the business of investment managers, making the right deal and getting the right investors are two of its most expensive investments. The power of networks can dramatically reduce the costs associated while providing better outcomes. As asset allocators, investment managers, consultants, investment banks and outside counsels start joining a tightly controlled network group they start adding value by providing critical information. The products and services start becoming more valuable as more people join the network. A carefully curated network can add immense value to every other player in this network.

For example: A Real Estate Manager is formalizing a new deal in the infrastructure sector in one of the emerging markets. He will need a host of local partners who can help him validate the deal. They could involve local analysts, lawyers, auditors, partners and a lender for the deal. This new network can start becoming more valuable as they can uncover new deals or get involved in other transactions. The investment manager benefits by entering a new geography.

These networks form and work like Constrained Networks and have a different dynamic then a typical social network which allows unconstrained participation. The unconstrained nature leads to spamminess and less collaboration. A constrained network can be leveraged to become more collaborative and work around specific projects.

In constrained networks “Affinity between participants, and the value of trade between those participants, matters.”

Platforms for Building Networks

Current generation platforms like Pepper are helping companies build network effects into their target segments business model. They are creating a playbook for investment managers to bring each of these partners together in creative partnerships.

We are building the steps to leverage the Network effect:

1. Understanding that the products and services involved are complex and specialized.

These products and services require complex interactions and are often played out over

the long term.

2. With each complex need, the services required are unique and the expertise each player

brings to these marketplaces matter.

3. Players collaborate around one or more products. Oftentimes one initial collaboration

leads to longer term partnerships.

4. Referrals to new partners are highly valued and bring the needed trust.

5. The players working together on a collaborative SAAS software platforms increase the

transaction velocity and overall satisfaction.

Building strong networks allows every partner to get stronger and add more value over time. Networks can be valuable but to reap the benefits the products must be valuable to each participant in the network. Hence a Linkedin network is not the solution for investment managers. The noted VC Bill Gurley in his post asked this question:

“Can the marketplace provide a better experience to customer “n+1000” than it did to customer “n” directly as a function of adding 1000 more participants to the market?”

If the answer is “Yes” to the investment manager, he should be building the network for tomorrow.

Pulak Sinha is the Founder and CEO of Pepper, a technology provider, designing the next generation of digital infrastructure for investment managers, incorporating the latest in Cloud, Artificial Intelligence, Open Architecture and User Interface Technologies. Before leaving to start building the digital platform that would become Pepper, Pulak Sinha was a founding member of GSO Capital Partners — currently one of the largest credit hedge funds. Pulak has also gained valuable expertise in the field of regulatory risk, market risk and credit risk management for large banks, having worked at Citigroup, Bank of America and Credit Suisse. He has an MBA from Columbia Business School and an undergraduate in engineering from IIT in India.

Leave a Reply