By Aladin Abughazaleh, Founder & CEO, ATA RiskStation, LLC

Introduction

Fund Managers and Asset Allocators are challenged with viewing risk from two, but not necessarily opposite, perspectives. Asset owners are tasked with keeping funding promises to beneficiaries over long-periods of time. Years of depressed interest rates have made achieving the allocators’ return targets much more difficult. Fund managers seek to deliver attractive risk/reward performance and compete to raise and retain assets. While both the fund managers and asset allocators have strong incentives to balance risk and reward, the stakes of this delicate dance can become more challenging at the tail end of an old bull market that is exhibiting rising volatility. Structured thinking about risk within a framework that is grounded in reality, humility and skepticism could be very helpful to both sides.

Overcoming Invisibility Risk and Funding Gaps

Not every strategy or manager is in a race with the stock market. Unfortunately, many excellent strategies are commonly overlooked by both wealth advisors and institutional investors (and their consultants) when they are eliminated from consideration by a return filter applied somewhere in the review process. Structurally hedged strategies such as equity long/short, market neutral and arbitrage, and many other conservative long-only or broadly diversified portfolios are all vulnerable to this “invisibility risk.” Managers need to more effectively tell their risk/reward story in a way that is relevant to meeting the goals of asset allocators.

Asset allocators are in a race with their actuarial assumptions and funding promises which are not always covered by recent portfolio returns. This gap between funding promises and portfolio results must be addressed one way or the other. Here are some potentially career limiting options for addressing this funding gap:

- Break promises to beneficiaries and lower benefits

- Consume principal to pay benefits and allow the plan to become underfunded

- Increase plan contributions by reducing corporate earnings

- Increase plan contributions by raising taxes to support public plans

- Dial up risk to boost returns and hope that nothing bad happens on your watch

Separate from the return challenge, senior executives at pension plans, endowments and foundations operating with limited staffs and budgets are still expected to oversee large externally-managed portfolios while providing timely and actionable performance and risk reporting to oversight stakeholders. Plan managers must be clear-eyed about the risk analytics they rely on and advocate.

False Precision: The Implications of Ex-Post and Ex-Ante Analysis

Ex-post analysis is backward looking. It seeks to measure what has already happened and present the results to decision makers so they can make inferences about portfolio return, risk and risk/reward.

Ex-ante analysis is forward looking. These techniques seek to project potential future portfolio outcomes based on a given set of assumptions, scenarios and historical data. Like weather forecasting, you look at the data, make some assumptions, run your models to make your best guesses about the future. Also, like weather forecasting – there are no guarantees.

For both types of analysis, humility and skepticism are essential to maintaining perspective. The risk of false precision is quite high since software empowers the user (or model) to make wild guesses and present the results accurately to eighteen decimal places. The results can look quite official without necessarily providing a solid foundation for robust conclusions.

Stability of the Strategy Risk Profile: Focus on Holdings vs. Returns

How do we assess the stability of a strategy’s risk profile over time? The goal is to understand how risks embedded in a strategy have been rewarded (or not) by the markets over time.

Many ex-post techniques focus on measuring the volatility of historical portfolio returns by assuming that more volatile return streams imply more risk taking. While this logic can provide useful insights, it does not always catch excessive risk-taking that was not punished by the markets because the manager’s bet worked out and was not captured by logging a loss in the track record. We can argue that if the manager routinely assumes large risks, their luck will eventually run out and the track record will ultimately show it. With long track records, that may be true but a very long bull market can potentially reward excessive risk-taking for a decade or more – until that bull market finally sputters.

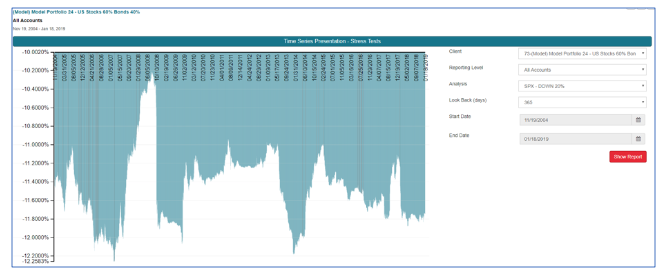

Some ex-ante techniques focus on measuring the risks embedded in the actual portfolio holdings. The chart above shows a portfolio’s risk profile for a single day for a series of stress scenario projections. This is a simple portfolio of 60% stocks / 40% bonds. Focusing on a single scenario, this analysis projects a portfolio loss of approximately 11.7% for a 20% drop in the S&P 500 (similar to the October 1987 meltdown of 23% in a single trading session). The chart below focuses on risk profile stability over time.

The chart immediately above shows the daily “track record” for the above scenario based on the daily portfolio holdings going back to 2004. It allows the manager to place in context the current risk projection with the extremes over time (best was -10.2% and worst was -12.2%). In other words, the risk profile for this strategy, for this particular scenario, has been stable over time and has remained within a 2% range for fourteen years – including the Financial Crisis.

Key Point: Even when asset allocators do not have access to the individual portfolio holdings, the analytics above offer powerful benefits to both the allocator and the fund manager. While allowing the fund manager to maintain the confidentiality of portfolio holdings, it empowers a timely and constructive conversation about risk that can reinforce the asset allocator’s confidence in both the manager’s transparency and the fund’s strategy.

Risk Track Records: Drawing Conclusions

Focusing on the daily risk associated with portfolio holdings can provide deeper insights into how the strategy’s risk profile changes over time. Even if the manager gets lucky when risk spikes are rewarded with positive returns, there is a clear audit trail that the risks were, in fact, assumed. Properly structured, this “risk track record” for any scenario, combined with the manager’s normal return performance track record, can help fund managers more effectively tell their story while allowing asset allocators to be more aware and deliberate about the risks they choose to assume.

Changes in a strategy’s risk profile are not always associated with a manager choosing to assume more risk. Rising instrument correlations generally and increasing market volatility can result in larger forward-looking risk projections based on portfolio holdings. The market environment can also make it more difficult to execute a strategy. For example, borrowing stock for initiating short positions can become more difficult or expensive during periods of market stress. Ex-ante risk analysis focused on portfolio holdings can flag a portfolio’s rising Beta with the market by showing larger daily risk projections as the portfolio gets “less short.” Charts showing daily portfolio-level risk projections and the trend in those projections over time are still valuable to asset allocators, even when they do not have access to the underlying positions because the change in the trend can trigger constructive and timely manager/investor conversations.

From the manager’s perspective, these ex-ante risk analytics can offer a great opportunity to differentiate their offering by providing a level of transparency that reinforces client confidence in both their strategy and risk oversight. There is no better time for proactive managers to emphasize transparency and risk-awareness than the potential tail end of a very old bull market.

Aladin Abughazaleh is a former asset allocator and a three-decade veteran of both alternative investments and financial technology. You can reach Aladin at aladin@atariskstation.com ATA RiskStation™ provides market-leading cloud-based risk analytics to wealth advisors, fund managers and institutional investors. Website: http://atariskstation.com/

Leave a Reply