By Daniel McConvey, Rossport Investments LLC

Note: All prices in this article are in US$ unless otherwise stated.

Outlook for Precious and Base Metals amidst Trade War

We are updating our commodity precious metal versus base metal preference as of the end of May 2019 in the shifting trade war world, identifying two stocks we like and explaining why we are taking some profits on Alacer Gold Corp. (ASR Cdn $4.07 as of May 31, 2019 on the TSX). Alacer was our “Best Idea” presented at the Hedge Connection event held on December 3, 2018.

Our beginning of the year outlook for 2019 was one of first half uncertainty with the trade war. However, we anticipated a resolution of the trade war by mid-year. With that scenario we were positive on gold equities for the first half and more positive on base metal prices for the second half of 2019.

The failure of China and the US to reach a trade resolution and the escalation of tensions with the US government action against China’s Huawei Technologies Co. have raised global risks. While we still think there is a good chance that a trade deal is reached, the growing global risks and uncertainties relating to this dispute are supportive of gold. So are Iran-related threats, seemingly countless other political tensions and an increasingly benign US interest rate outlook. While base metals stand to see a large rebound from very depressed levels if global tensions abate, we are increasingly concerned about a hit to global metals demand. We believe gold equities are a safer investment in this increasingly uncertain world.

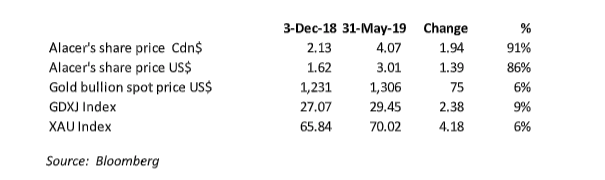

Despite a slight increase in the gold price and these growing uncertainties, year-to-date gold equity indices (the XAU and GDXJ) are near the relatively depressed levels where they started the year (see table below).

In the gold equity space, we focus largely on the midsize companies and the developers. Two companies that we like now are Centerra Gold Inc. (CG Cdn $7.74 on the TSX) and Dundee Precious Metals Inc. (DPM Cdn $3.74 on the TSX), quoted as of 5/31/19. Both these companies trade at a discount to their NAV and both will benefit from material cash flow increases in the next 18 months from new mine startups.

Alacer Gold Corp.– “Best Idea” Six Months Later

The rest of this article is a six month follow up on our “Best Idea” presented at the Hedge Connection event held on December 3, 2018. Our “Best Idea” was a strong buy on Alacer as it was trading at a deep discount to our NAV and the construction of their new autoclaves played directly into our core investment strength of determining if a project would be constructed and commissioned at or near plan. Alacer’s share price was Cdn $4.07 as of 5/31/19. Its 52-week range is roughly Cdn $2-$4 and it has increased from Cdn $2.13 to Cdn $4.07 since December 3, 2018. Our 5% NAV at $1300 gold is currently about $3.00 ($4 Cdn) up from $2.50 at $1200 gold in December. We continue to give it limited credit for some promising exploration upside within its mining area footprint.

Alacer’s head office is in Denver. It trades about 1 million shares a day. Its market capitalization is about $860 million and its attributable net debt including restricted cash is about $170 million as of March 31, 2019 (excluding capitalized leases) giving the company an EV of just over $1 billion. The performance data of the stock since my December presentation with some comparatives are in the table below:

When we presented on December 3, we thought the chances were good that this stock could double in the ensuing 18 months as it commissioned its new gold process circuit, generated material free cash flow, paid down a chunk of its debt, increased its NAV through exploration, possibly re-launched its dividend and grew its multiples with recognition that its operating skills punched above its weight class.

When we presented on December 3, we thought the chances were good that this stock could double in the ensuing 18 months as it commissioned its new gold process circuit, generated material free cash flow, paid down a chunk of its debt, increased its NAV through exploration, possibly re-launched its dividend and grew its multiples with recognition that its operating skills punched above its weight class.

Alacer’s sole operating asset is its 80% owned Çöpler gold mine in Eastern Turkey. Çöpler has been in operation for about a decade. Running out of easy to treat oxide ore a few years ago, Alacer made the decision to build a new process plant that, among other things, pressure oxidizes grey colored sulfide ore under high temperature and high pressure into rusty red oxide ore in two small submarine sized vessels called “autoclaves”. Once oxidized, extracting gold from the ore is relatively simple. There are only about a dozen gold autoclave circuits globally and they add a complexity and risk for investors. Construction was completed in October 2018 and the circuit commissioning had just begun when we visited site in November. Commissioning continues but commercial production is expected to be announced in the coming weeks. The plant cost Alacer almost $700 million to build which was more than its market capitalization when I presented on December 3. As a result of building the project, the company had gone from having substantial net cash three years ago to having $250 million of consolidated net debt at year end. The downside was clear. Material start up issues for the plant would impact cash flows and worry the market about pending debt repayments. A disastrous scenario could result in a distressed equity issue or worse.

We didn’t think that would happen and we saw material share price upside. Here are the reasons:

1. Most importantly, we expected a relatively smooth start up. We had studied the project for

years. I knew the autoclave process from my days at Barrick. We consulted with experts.

Finally, when we visited site in November, we liked what we saw;

2. Second, Alacer was in the early days of delineating a material deposit called Ardich that is in trucking distance from the existing process facilities. Ardich ore is mainly oxide and easy to treat and we were expecting it to contribute materially to our NAV growth; and

3. Third is what we will call “Our Mid 2020 Vision” in which:

- Çöpler’s autoclave circuit is producing in excess of 200,000 ounces per year;

- Ardich is in production;

- 20% FCF yield on Alacer’s December 2018 share price;

- a deleveraging story with the pay down a chunk of Alacer’s debt;

- a company per share NAV in excess of Cdn $4 with exploration success;

- a likely dividend declaration; and finally

- a multiple boost by proving its operational strengths in the Çöpler ramp up.

So where are we at the end of May 2019? The bottom line is that Alacer seems to be firing on nearly all, if not all, cylinders.

In the first quarter of 2019, despite being in a commissioning stage the company generated a small profit and about $30 million of free cash flow. The company produced a surprisingly strong 89,000 ounces of gold in the quarter which annualized would be in the upper end of its 320,000 to 380,000 ounce guidance. 37,000 of those ounces were pre-commercial production ounces from the autoclave circuit which should improve quarter on quarter throughout the year. The majority of the 89,000 ounces came from oxide ore. Oxide production was aided by having multiple sources including stockpiles available. While oxide throughput is expected to fall off the rest of the year, we expect that Alacer’s total production will be in the upper end of their guidance or maybe better. The company may re-assess guidance at the end of the second quarter.

The 37,000 ounces from the autoclave circuit is a solid result. There have been teething issues in commissioning but not major ones. Last month the company shut down one autoclave for planned inspection. This shutdown was something we were waiting for as new autoclave circuits often need partial or full relining or other fixes after start-up issues. The vessel was found to be in excellent shape. As a result, the shutdown period was shortened and the planned inspection of the second autoclave was pushed out six months to early 2020. We worry some on this inspection delay, but it does show how confident management is after this April inspection.

It is hard to exaggerate the importance of this autoclave ramp up. The stock had been trading at a huge discount to its peers because of market skepticism in the company’s ability to commission this circuit successfully. The period of commissioning and ramp up is far from over. Risks remain. However, our confidence on this ramp up continues to grow. We expect a commercial production decision in coming weeks and a detailed update on the circuit with second quarter reporting.

On Ardich, the company announced a maiden resource in mid-December of 300,000 indicated ounces. On April 30th it announced it had more than doubled that resource to over 600,000 indicated ounces. However, a quarter of those ounces were sulfide which are unlikely to be treated for several years. Ardich is on track with our expectations, although we are hoping for slightly better than currently estimated oxide grades. Ultimately, we expect Ardich to provide a material increase to the Çöpler area’s 4 million ounces of reserve. We expect more exploration updates late in the year.

On all of our Mid-2020 Vision items for Alacer (see above), everything is roughly on track and in some areas better. Ardich may take longer to get into production but this would likely be offset by feed from other areas.

However, despite all the good news, Alacer is no longer a deeply discounted story. It is trading near our $3 NAV. While we expect that NAV to grow with exploration and development plans, Alacer has rerated. We think there are more discounted stories out there which we plan to discuss in future write-ups. Our worries in taking profits center around more possible material share price appreciation on free cash flow realizations in 2020, exploration, delivering, and a continuing production, earnings, free cash flow growth story that exceeds our solid expectations.

*****

Rossport Investments LLC specializes in the metals and mining sector. If you would like more information on our work and views, please contact Daniel McConvey at (646) 722-4119 or by email at daniel.mcconvey@rossport.com.

Note: Past performance is not necessarily indicative of future results. Forward-looking statements reflect the Investment Manager’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond the manager’s control. Investors are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document.

Leave a Reply