By Andy Chakraborty and Uzi Hadar, Duo Reges Capital Management LLC

Article 1 of the US Constitution tells us that Congress shall have the power “to regulate Commerce with foreign Nations, and among the several States.” Regulation around the world, whose purpose is “to make regular,” as in repeatable, predictable, and understandable is a source of repeatable, predictable, and understandable noise to the investment process and is an underexplored source of investment opportunities.

Let’s start with what regulation is and is not. Legislative action usually provides a regulatory “framework” — rules and goals that inform the boundaries and objectives of professional regulators. The frameworks, from Dodd Frank to Net Neutrality, typically garner the public interest and comments that end in announcement, but they aren’t really the end of the regulatory process. These frameworks are more in the realm of public policy, or dare we say it, politics.

The impact of detailed technocratic rulemaking and enforcement actions, and the capital markets’ reaction to them present opportunities for investors. To clarify, we are excluding from our mental model already well explored government-related investment plays such as when armies of research teams with PhD/MDs analyze molecules for FDA approval, or institutional trading and activist funds analyzing a government as a counterparty when in pursuit of a sovereign debt.

The effect of regulation typically has a negative bias—over time, regulations are more of a source of fear rather than greed for the markets. Of course, that’s completely within how we all think about the world, a well-documented cognitive bias, hindsight bias, or our need to feel like we knew what was going to happen all along. The market reflects this bias as it views legal proceedings, where we use the words “not guilty” instead of “innocent” in most cases (e.g. it is common to view someone found not guilty as simply having had a good attorney).

Biases slip into the algorithms and machine learning/artificial intelligence tools used by investors because many are hidden or implicit. As more of modern life runs up against the hard edges of deeper human-human, computer-human, or computer-computer interactions, regulations will increasingly have impact on our activities, both visibly and invisibly. Regulations alter industries’ evolution, accelerating some aspects, slowing others, as well as simultaneously leveling playing fields or entrenching current positions through rules that shake up the status quo or memorialize it through blessing certain standards and practices.

The markets don’t know what regulation will do, but we might have a way to think about the problem. In dealing with the very technocratic details of rule-making and enforcement actions, the OECD has a detailed process they propose for evaluating regulation (at a high level, focused on consistency, transparency, accountability, targeting, and proportionality). This thoughtful approach is applied inconsistently at best. Compounding this problem is the rising tide of international regulatory conflict– will China and the US end up with divergent 5G and web services technology stacks? Will extra-territoriality such as the EU GDPR effectively apply to all developed market websites and services? Can California and the Federal government both regulate fuel efficiency?

Death and Taxes

Even though the regulatory outcomes are not always certain, we know regulatory action is coming, and the OECD toolset does help us understand the key elements of the regulatory feedback loop, notably where both discretionary/human and systematic/machine learned trading might fail.

The solution is to be like the remora, the fish that attaches to sharks. The market, functioning as the shark, over time figures out most regulations and prices them appropriately and captures much of the value. However, by applying statistical/algorithmic tools to break apart regulatory proportional intent from short and medium-term market reaction captured from heightened volatility among other signals, “remora” investors can unlock mismatches between what the market thinks a regulatory enforcement action is telling it and the message that the regulator meant to send.

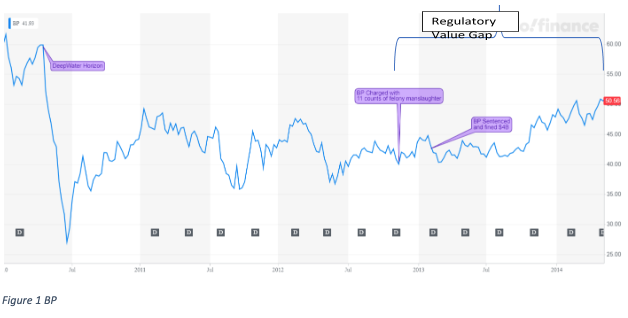

Big, headline-grabbing events aren’t the best place to look for repeatable sources of value, but even in these spots, untapped value exists. British Petroleum’s infamous Deepwater horizon Gulf of Mexico disaster resulted in landmark fees and criminal prosecution of over $4B in impact. The portion after the news event is really the “news horizon,” while we are most interested in the 12-18 months after the charges are filed, the “regulatory value gap.” We’ll forget about the actual finalized sentence, as the regulatory action is the volatility driver for the market. Without any belief about magically timing the market, returns would have ranged up to 25% for the approximately 18-month regulatory value gap—the window in which we see regulatory effects persist (e.g. increased volatility).

Similarly, the old Imperial Sugar firm (NASDAQ: IPSU, acquired in 2012) suffered a significant refinery fire in May of 2008. OSHA leveled its 3rd largest fine ever up to that date at $8.7MM in July of 2009 and the market punished the value of the firm, falling below book value, a key indicator for an asset-heavy firm such as a refinery. Through understanding the embedded signals in the July 2009 event, investors would have had the opportunity to generate a return of up to 15% within the regulatory value gap.

In general, we can work to solve this by mapping each of the areas that will be regulated with the underlying regulatory regime (the goals, tools, processes, adjudication and personnel involved), the potential sources of conflict to the regulatory intent, and the size and scope of rule-making or enforcement action/fine. This framework will create an opportunity by allowing investors to find openings in overlapping spaces of market behavioral biases (e.g. abnormally high or low implied volatility), and the structural issues created by the rising tide of factor, passive, and algorithmic/machine learned trading.

The value gaps of the past are morphing. Our research suggests that good places to look for these gaps are coming from growth in Machine Learning/Artificial Intelligence usage not merely in technology, but applications in health care, law enforcement and personal privacy/data aggregation. Growth in data aggregation/control and ownership of data, Internet-of-Things/distributed devices, autonomous devices (robotics and vehicles), cloud computing, augmented reality and Mobility/5G are also key areas that we expect to show potential regulatory value gaps. These technologies are maturing to the point where regulations will start to catch up and increasingly alter the innovation cycle, just as it has been for other arenas, inexorably, like death and taxes.

Duo Reges Capital Management LLC is a Long-Short Hedge Fund unlocking potential regulatory value gaps driven by hyper Innovations. www.duoreges.com

About the authors

Andy Chakraborty is a Founder, Managing Partner and Co-Portfolio Manager of Duo Reges Capital Management LLC. Previously, Andy was Chief Data Scientist at Amazon S3 and Amazon Retail Systems. Prior to that, he led data science teams at Microsoft, as well as driving corporate analytics and finance at Microsoft and Sprint. Andy holds an MBA from the Darden School of the University of Virginia.

Uzi Hadar, CFA, is a Managing Partner and Co-Portfolio Manager of Duo Reges Capital Management LLC. Uzi is a seasoned Private Equity professional with significant capital markets background and a fundamental deep-value acumen. Uzi holds an MBA from the Darden School of the University of Virginia.

Leave a Reply