Contributed by Anthony Maniscalco, Managing Partner and Head of Strategic Capital Group, at Investcorp

Background on GP Minority Investing

GP Minority Investing (or “GP Staking”) is the acquisition of a minority equity interest (typically less than 25%) in the management companies and general partnerships of alternative asset managers (“GPs”). Unlike investing as a limited partner in a fund, GP minority investors have exposure to the GP, and benefit from the overall cash flow generation and growth of the GP as a whole as compared to solely investments as an LP in a fund.

Evolution of GP Minority Investing

Prior to the 2008 financial crisis, GP minority stake investing was episodic, and a relatively infrequent practice. Activities in this space were primarily executed by banks seeking hedge fund minority stakes to realize business synergies (e.g., prime brokerage, sales and trading, etc.) and/or institutional investors looking to acquire stakes in private equity firms to reserve access/ capacity in future fund vintages. GPs typically sold primarily to obtain financial diversification and tax benefits.

Post crisis, GPs increasingly appreciated the broader advantages of having a minority partner. Similar to how many private equity firms support portfolio companies, GPs recognized the potential benefits of having partners with the ability to provide capital and add strategic value, while still allowing GPs to retain control and autonomy over their businesses. These buyers however became limited in their ability to continue to pursue minority investments (e.g., banks became more regulatorily constrained). As such, there was an unmet need for access to capital in this market resulting in the establishment of funds dedicated to GP minority investing. The mandates of the initial GP staking funds coming out of the financial crisis targeted hedge fund managers. Over the last several years, GP staking has evolved, expanding into multi-asset class strategies, especially private equity and private credit. Activity has also been focused over the last several years on the largest GPs given the need for the new stake buyers to deploy large amounts of capital based on the amount of capital raised. Activity has increased awareness of the strategic and financial merits across all alternative asset managers of selling a stake in their business. These benefits are also widely understood and accepted by the market, and investors in the underlying funds.

Key Factors Driving GPs’ Demand Broadly for Capital

Strong Underlying Environment for Alternative Asset Managers with Favorable Market Dynamics

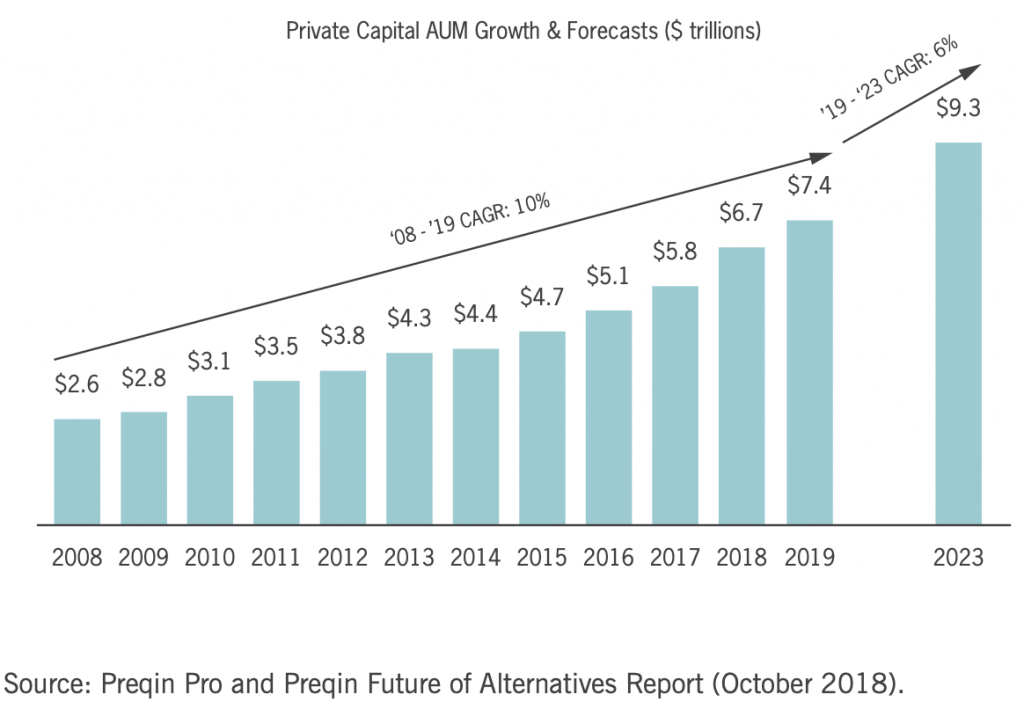

The alternative asset management industry has experienced substantial growth over the last ten years driven by factors such as increased allocations by institutional investors seeking strong risk-adjusted returns and the growth of the retail wealth base. These dynamics have propelled the entire alternative asset management industry, with Private Capital AUM (i.e., private equity, private credit, real estate, and infrastructure) reaching $7.4 trillion as of June 2019.

Market research suggests that long-term growth prospects for the industry remain robust. According to Preqin, Private Capital strategies are anticipated to reach $9.3 trillion in AUM by 2023.

While we recognize that the continued spread of coronavirus is creating near term volatility and economic uncertainty, conditions that are driving strong secular demand for private market alternative investments are only becoming more pronounced including:

• Low interest rates that are continuing to decline globally, and which are expected to remain low for the foreseeable future.

• Private markets’ outperformance compared to public equity markets, which are experiencing extreme volatility.

• Select investors with defined liabilities needing to allocate more to private market strategies to achieve acceptable yields and returns.

Allocations are further anticipated to increase across all primary Private Capital strategies. Source: Preqin Investor Update: Alternative Assets (H2 2019)

Leave a Reply