By Daniel McConvey, Rossport Investments LLC

Background and Perspective

Gold spiked to new all-time highs of US$2070 and Euro 1740 last week and is currently trading about US$1940 and Euro 1640 after a sharp correction in the past two days. That correction has modestly muted our more cautious view we had heading into this week.

Forecasting gold is always dangerous because one can’t predict the future. We recall reading about a gold trader who lost his job after heavily shorting gold in December 1979 at around $500 after the price about doubled in the prior six months. Then the Soviets invaded Afghanistan and gold quickly went to over $800.

Our historical bias has admittedly been cautious. Gold has moved higher than we had anticipated despite our pessimistic view of the geopolitical world. However, whatever your view, the main purpose of this paper is to point out challenges for major sustained gold upside over the next few months that the market may be forgetting. Some in the market are calling for gold at $2500 and higher in the next year. That could happen but in our view it would likely take one or more additional forces. A huge weakening of the US dollar could be one. Any move towards negative US interest rates could be another.

Our View

We are neutral on gold from current elevated US$1940 levels at current exchange rates in the run up to the November US Presidential elections. In the medium term (through 2022) we believe gold prices will stay elevated and could spike significantly higher especially with a Trump re-election, but will average below current prices. In the longer term beyond 2022, we believe prices will fall as current bonanza margins, if sustained, will incentivize increased production. We are reducing our gold equity exposure at least temporarily as we look for better opportunities elsewhere in the mining space. We are neutral in the short term because despite the very recent correction and supportive factors, we think gold has risen too far too fast and is overbought on the back of mainly US ETF buying. Again, we think gold may need another catalyst or two to move materially higher from here against the forces we discuss below. Of course in this world we could get those catalysts. Anything can happen in this highly uncertain world especially in the run up to, and after math of, the US presidential elections.

Below is a list of the bullish and bearish factors for gold followed by some more in-depth analysis of a few of these factors.

Gold has been in the midst of a near perfect storm. That perfect storm supporting higher gold prices is caused by temporary and longer term factors that include:

- Major human suffering, surreal feelings that come with social distancing, and global economic uncertainty as a result of the global COVID-19 pandemic;

- Unprecedented western world government and central bank responses to COVID-19 which include: a) huge stimulus spending; b) the related assumption of materially higher sovereign debt levels; c) commitment to near zero interest rates for years; and d) commitments to buy or backstop prices of enormous amounts of bonds including some corporate bonds;

- The resulting impact in government bond yields with the US 10-year treasury yield dropping to about 0.5%;

- Huge gold ETF buying, mainly by US investors, as a result of these factors. The rise in global equity markets has aided this as investors have had a recovery in wealth that allows them to buy ETFs;

- The withdrawal of US global leadership and the major weakening of western world alliances;

- Serious tensions between the US and China and more recently India and China;

- Anarchy in US city streets with the Black Lives Matter (“BLM”) movement since the police killing of George Floyd in Minneapolis on May 25th;

- Worries of chaos with mail in voting in the upcoming November US presidential election;

- COVID-19 related mine supply disruptions which could result in a 3-5% fall in 2020 mine production;

- In addition to these mine disruptions there have been shortages of physical gold in the US due to COVID-19 related refining and shipping disruptions. This has added a scarcity/sentiment factor to the desire to own gold;

- And lastly the expectation of a weaker US dollar which would support US dollar gold prices even if gold prices in other major currencies level off or fall.

The above factors are hugely supportive of the gold price. However, the challenges and threats for gold to continue its strength from here are numerous and include:

- The fading of short term bull factors like gold shortages, hopefully social distancing, and possibly BLM protests;

- Forecasts for the upward creep in government bond yields albeit from a low base;

- Overcoming an expected historic fall off in jewelry demand (about half of total gold demand in recent years) as gold prices rise and income shrinks;

- High expected jewelry recycling and lower physical investment in emerging markets countries ravaged by COVID-19;

- Sustaining the historic level of gold ETF buying of the last few months;

- Possible profit taking by investors and possible hedging by producers;

- Less central bank gold buying (for example, Russia) and the possibility, albeit a small one, that a central bank may decide to sell opportunistically into current high prices;

- A growing likelihood of a successful COVID-19 vaccine in 2021;

- And growing odds (currently around 60%) of a democratic sweep in November which would likely bring a more stable political and monetary world (albeit with higher taxes) as 2021 begins.

We are going to expand on three of the above factors to which we think the market might not be giving enough weight.

- Emerging market demand will be devastated. We don’t think the market appreciates the fall off in emerging market demand we think is taking place. While China, Vietnam and others have handled COVID-19 well, many emerging market countries such as India and Brazil are suffering badly. India in recent years has consumed 500-700 tonnes or about 10-15% of the world’s gold. This year its GDP is expected to drop for the first time in decades. The government does not have the funds to effectively pay people’s salaries unlike in the Western World. Weddings are being postponed and gold prices have skyrocketed, negatively impacting the demand for gold. We expect to see a huge fall off in jewelry demand and would not be shocked to see net disinvestment of gold bars and coins. This happened in Thailand in the second quarter according to the World Gold Council.

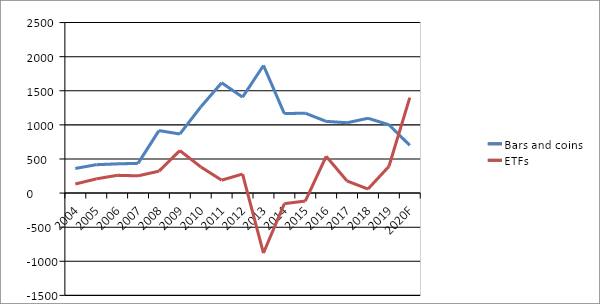

- We expect ETF demand to weaken. ETF demand YTD to July 31 was 900 tonnes, 50% higher than any previous full year and about a third of this year’s gold market by our calculations. ETF demand has been fickle since the gold ETFS began in 2004. As the graph below in Exhibit I indicates, ETFs have been the main driver of the increase in the price of gold so far this year. We think that this buying strength may abate as the COVID-19 management situation improves and if the BLM movement results in less confrontation.

Exhibit 1: Global Bar and Coin and ETF Gold Demand in Metric Tonnes

The global gold market is about 4,500 tonnes. Bar and coin demand has been much more stable that ETF demand. Bar and coin demand made a step change after the Global Financial Crisis and may do so again after the financial stresses of COVID-19. The recent record buying of ETFS has been US driven. In addition to other factors we discussed above, the buying strength may be partly fueled by US centric factors like the relatively poor management of COVID-19, the BLM movement protests and political chaos. We think that some of those factors will likely abate. Source: GFMS and Rossport estimates.

3. Current bonanza gold mining margins will incentivize production albeit three to five years out. In most other currencies the price of gold had already broken historical records. The below graph from Bloomberg shows the gold price in US dollars, the Euro, Canadian dollars, Australian dollars and the South African Rand:

Exhibit 2: Gold prices in US$, Euros, Cdn$, Aus$ and SA Rand – 2009 to present

Source: Bloomberg.

If current gold prices and exchange rates remain, chances are high that mine production will grow materially in the next 3-5 years. High margins will incentivize production. Gold prices could fall by US$200 from current levels and margins would still be robust. Cost inflation is expected to stay low in at least the short term due to low energy prices and slack in the labor and supply chains. Recent COVID-19 related expense elevation should be temporary as companies become smarter at managing it and ultimately, a vaccine arrives. With bonanza margins artisanal production (estimated at about 20% of global production or over 600 tonnes) will be the first to grow, then old mines will reopen and then new projects will be developed. Gold mining engineering firms and contractors globally will be very busy. This is not a factor for supply this year. In fact production may fall marginally this year with COVID-19 disruptions absent a fast artisanal response. Beyond 2021 it is an issue. Some of the production may be accelerated by the hedging of production on some projects.

We will leave gold equities for a future write-up. Although we have reduced our gold equity exposure it is likely temporary as we believe the gold price will stay elevated and high gold mining margins will persist in the medium term. We are now focused on picking the winners from the losers from gold mining developers.

In conclusion, the increase in the price of gold has been backed by many supporting factors especially the unprecedented central banks stimulus as a result of COVID-19, debt concerns, and numerous geopolitical events that have taken place this year. In the short term, the price of gold will continue to be supported by major uncertainty and events in the lead up to, and aftermath of, the US elections. However, the expected devastation of emerging market demand, better management of the COVID-19 crisis, a possible Covid-19 vaccine in 2021, and a possible slowdown in ETF buying are challenges for major sustained gold price appreciation from current levels.

***************

Rossport Investments LLC specializes in the metals and mining sector. If you would like more information on our work and views, please contact Daniel McConvey at (646) 722-4119 or by email at daniel.mcconvey@rossport.com.

Note: Past performance is not necessarily indicative of future results. Forward-looking statements reflect the Investment Manager’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond the manager’s control. Investors are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document.

Dave Norris

Todays rally could be short lived. It is typical of the first opening of a new year and new government. I think you nailed it on the mid term. After Biden begins, who knows what his policy’s will do to change gold’s demand. In the long run I believe gold will go up because of the abundance fiat currency now being printed.