Contributed by Daniel McConvey, Rossport Investments LLC

As shareholders of TMAC Resources Inc. (“TMAC”) we are disappointed with the January 5, 2021 news of the proposed buyout of the company by Agnico Eagle Mines Limited (“Agnico ”) for Cdn $2.20 per share or just under Cdn $300 million. While the offer is Cdn $0.45 per share higher than Shandong’s May offer that was struck down last month by the Canadian government on national security concerns, we think history will view this transaction as a steal relative to current gold mining valuations. While TMAC was at risk of bankruptcy in the depths of the March-April 2020 market panic when Shandong made its uncontested offer, that is not the case now. We bought shares of TMAC seeing a two plus year recovery story to much higher share price levels and wish it was remaining independent.

The following is the background in a nutshell. TMAC which operates the Hope Bay gold mine in the Canadian arctic conducted an effective auction process early last year that coincided with the onslaught of the Covid-19 pandemic. Mine operations were cut in half and there was the threat of having to suspend operations completely. Given poor liquidity and panicking markets, bankruptcy was feared by many in the market. TMAC’s share price fell to a low of Cdn $0.45 on March 30, 2020 down 90% from the Cdn $5 levels of six months before. On May 8, Shandong, the only bidder, agreed to buy the company for Cdn $1.75 per share. Markets have improved and site operations have steadied albeit at reduced but profitable rates. On December 21, 2020, the Canadian government rejected the Shandong deal. Two weeks later on January 5, 2021, Agnico agreed with TMAC to buy the company for Cdn $2.20 per share by way of a rare and expedited plan of arrangement that effectively assigns Agnico the Shandong deal including the timing but with the higher price.

In this write up we will first look at the history of TMAC’s arctic Hope Bay Mine. Then we will look at the challenges the company faces. Third, with the help of a graph, we will look in more detail at the set of circumstances that lead to the share price freefall early in 2020 and has kept it down. Finally, we will look at why we think TMAC’ value is much higher than it is being sold for.

There are three admissions we want to make up front:

First, Rossport has been buying TMAC at depressed prices in the last few months and admittedly is benefiting from the recent share price appreciation. TMAC recently became one of our largest positions before last week’s offer. Our thesis was that the Shandong deal would not be approved by the Canadian government. Then TMAC would have the necessary time in a more stable environment to refinance some or all of its Cdn $175 million of debt due June 30, 2021 and ramp up operations again over the next two years during which time the share price would, we think, recover to pre 2020 prices.

Second, although we are not happy with the proposed takeout or the price, we view Agnico as the cream of the crop North American gold miner. They have arctic experience. They do things right and have been doing so for decades. Hence the confidence we have in Agnico from an ESG perspective and doing right by the people of Nunavut and Hope Bay.

Third, with its current resources we don’t see Hope Bay as a Tier 1 mining asset yet. Hope Bay will grow but as discussed below it has its challenges too.

Background of Hope Bay

Hope Bay has been explored for decades by several companies. Newmont bought the project in 2007 for Cdn $1.5 billion. To date another roughly Cdn $1.5 billion has been spent at the project. In 2013, Newmont floated the asset privately and TMAC did its IPO in 2015. Newmont has remained a 25+% shareholder ever since. Hope Bay has three deposits. Doris and Madrid are on the coast connected by an 8km all weather road. Boston, which is the largest and likely best deposit is 50km away and needs infrastructure to develop. Doris is a high grade but smaller deposit developed first due to its grade and relative ease of access.

The problematic Doris mill (process facility) started processing ore in 2017. The choice of mill supplier was influenced by the timing and ease of getting the mill parts to site in the annual ice free late summer sea lift. The equipment deliveries were able to meet the sea lift time cut off deadline and were easily sent in ship containers. However, the mill choice was a huge mistake. The mill has been more problematic treating what is conventional gold ore than any we can recall. Production has suffered. That said, there is new internal optimism that, with moderate capex, the mill performance can continue to be improved and capacity increased.

The following are other challenges for TMAC especially as a continued standalone company:

- Significant capital is required to restart underground development at Madrid and to catch up on development at Doris after underground mining development was cut materially last year.

- The metallurgy for Madrid and Boston has challenges relative to Doris. Lower gold recoveries are expected.

- The company has Cdn $175 million of expensive debt due June 30, 2021. While some of this debt can likely be pushed out to a later maturity, we expect an equity raise is required in the absence of a buyout.

- Employee retention is a challenge. It is always harder for a single asset company to recruit and retain key technical help and this is made tougher in the arctic. Over half of the work force was laid off last year and there will be challenges re-staffing. Recent layoffs in the Alberta oil sands mitigate these concerns somewhat. Moral is high at site now. However, any uncertainty brought by another company auction process should it happen could result in more key employee losses.

- Other possible buyers are limited due to limited artic experience by most mining companies. Other interested parties may want to joint venture with a partner.

2020 Share Price Crash

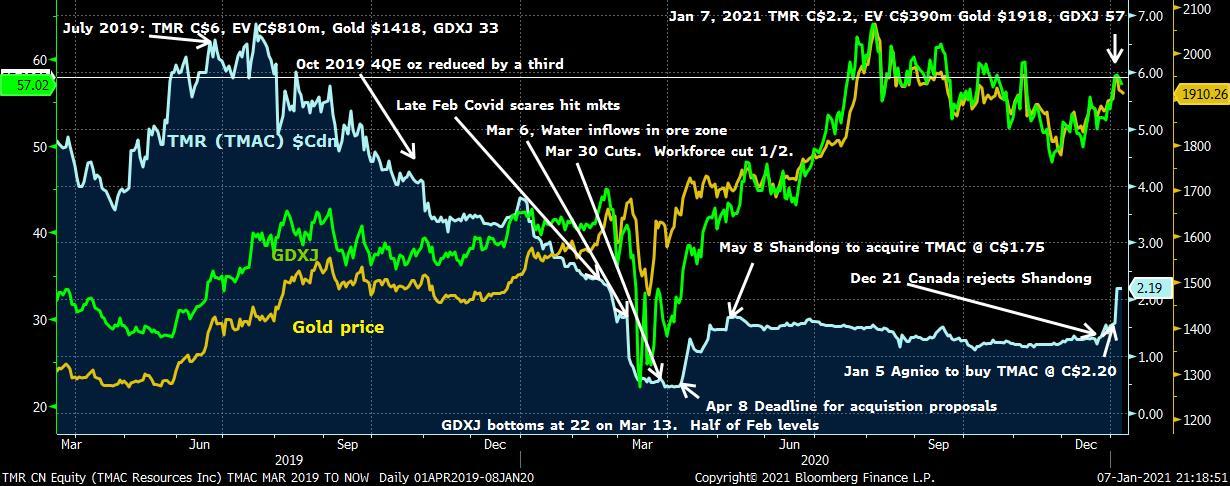

How did TMAC’s share price go from Cdn $6 to Cdn $2 in 18 months in a rising gold and gold equity market? The short answer is it ran into operating problems in late 2019 and early 2020 before getting hit with Covid operational cut backs and a liquidity crisis. As the graph and related caption below show the timing of the company’s sale process which was announced on January 20, 2020 and involved final offers by April 10, 2020 occurred during the middle of the Covid-crisis during which markets crashed and travel to the extent needed was impossible. Although at least one other party was interested they understandably backed off as the earth was shaking. Shandong’s Cdn $1.75 offer was the only one left on the table. Since the Shandong deal was announced on May 8 the share price had languished below that with the worries the Canadian government would reject the deal and force TMAC into another liquidity crisis despite the rebound in gold and gold equity prices. Little company marketing has been done. Exploration has been halted. Sell side and buy side interest has been near silent. Three of the seven sell-side analysts have been restricted since May 2020 or before.

TMAC (TMR) Share Price, Gold and GDXJ (Jr. Miner) Index April 1, 2019 to January 7, 2021

Source: Bloomberg

Looking at the graph above from mid-2019 to January 7, 2021, TMAC’s share price had fallen 63% from Cdn $6 to the current Agnico Offer price of Cdn $2.20 and the enterprise value had fallen from over Cdn $800 million to less than Cdn $400 million while the gold price had increased US$500 and the GDXJ (Van Eck Junior Gold Miners Index) had increased by over 70%. Operational issues, Covid-19 pandemic necessitated cutbacks, liquidity issues, and panicking markets put the company in dire straits in the middle of its strategic review process during March and April 2020. Shandong ended up being the only bidder. Despite its difficulties, TMAC generated free cash flow the last two reported quarters. We don’t think it makes sense that TMAC’s current enterprise value of Cdn $400 million is half of what it was when gold price was US$500 lower 18 months ago.

Two ways of Valuing TMAC

The most simple way of valuing TMAC is using the NPV estimates in the March 2020 Pre-feasibility Study (43-101 technical report filed on SEDAR). That study envisioned expansion capex including a new mill at Madrid of almost Cdn $700 million. Despite the high capex number, using an 8% discount rate the study calculated a pre-tax NPV of Cdn $0.8 billion at US$1625 gold prices (Cdn$2180 using the study’s 1.34 CAD/USD exchange rate). In the study each per ounce US$100 (Cdn$134) increase is worth about Cdn $220 million to the NPV. So at current approximate Cdn $2340 spot gold prices the NPV would be about Cdn $1060 million*. Take away $100 million (approximately 10%) for taxes** and Cdn $100 million of net debt and you get an approximate NAV of Cdn $850 million or about Cdn $6.50 per share. TMAC is not a developer but using more conservative bottom end of developer multiple of 0.5 would give you a Cdn $3.25 per share valuation. We highlight that this calculation is using: 1) an 8% discount rate (whereas analysts discount junior producers at 5%); 2) developer multiples which are more conservative than junior producer multiples; and 3) the bottom end of those multiples.

Critics would argue that last year’s prefeasibility study will end up being light on capex. However, based on our discussions with previous and current management, there are positive changes to consider as well. Recent material success with recovery and throughput in the Doris mill makes a new mill at Madrid in, say, the next 5 years less likely. Spending limited capital to improve the existing mill may improve the economics materially. Further, we expect gold reserves and life of mine planned gold production to grow materially in coming years.

Another way to look at TMAC’s valuation is to look where analysts valued it before last year’s crises. In July 2019 as per the above graph the stock traded at Cdn $6 and consensus target prices were Cdn $8 per share. That was when gold was at US$1400. What’s changed since then? There has been 15% dilution although net debt has actually gone down. Adjust the share price down Cdn $1 for dilution and you still have Cdn $5 but the gold price is US$400 higher. We would argue that the company outlook from here is similar or better than it was in July 2019. While 2020 and 2021 output is lower due to limited supplies and manpower, the company has gotten a grip on its operations. Mill performance is improving. Internal confidence in what is being budgeted is higher. Mine plans are more solid.

Summary

We see TMAC as a very undervalued asset. The circumstances of 2020 with the crunch of the Covid crisis left it exposed and for a while near bankruptcy. Things have materially changed since then. The company has recovered, addressed its operational issues admirably, and has generated positive free cash flow in the last two reported quarters despite processing ore only half the time. We recognize the dilution and other risks present. However, we think that half if not all of the current Cdn$175 million in Sprott debt could likely be extended to December 2021, giving the company time to plan, tell its story, restart some exploration, conduct a new full feasibility study, and continue to execute. In our view, in time, TMAC would likely be worth a multiple of its current share price.

* (((2340-2180)/134)x220)+800)=1063 million

** The effective tax rate in Nunavut is 27%. However, the company has Cdn$360 million of tax loss carry forwards and Cdn $300 million of deductible timing differences. Therefore, we are assuming the NPV of taxes paid will be approximately 10% or less than half of the 27% tax rate.

Our preferred route for TMAC would have been for it to remain a stand-alone company, at least until its share price recovered from the current depressed levels even if that meant short term pain by way of a rights offering or other equity issue in the next couple of months to repay at least some of the maturing debt. If there had to be a transaction, we wished it would have been for half of the asset creating a joint venture where shareholders could have participated at least 50% in future upside.

Hope Bay will likely be a mine for more than 50 years. If this proposed transaction with Agnico closes we hope that it will add huge value to Agnico Eagle. We think most will agree with us that it will.

Rossport Investments LLC specializes in the metals and mining sector and runs a family office. If you would like more information on our work and views, please contact Daniel McConvey at (646) 722-4119 or by email at daniel.mcconvey@rossport.com.

Note: Past performance is not necessarily indicative of future results. Forward-looking statements reflect the Investment Manager’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond the manager’s control. Investors are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document.

Leave a Reply