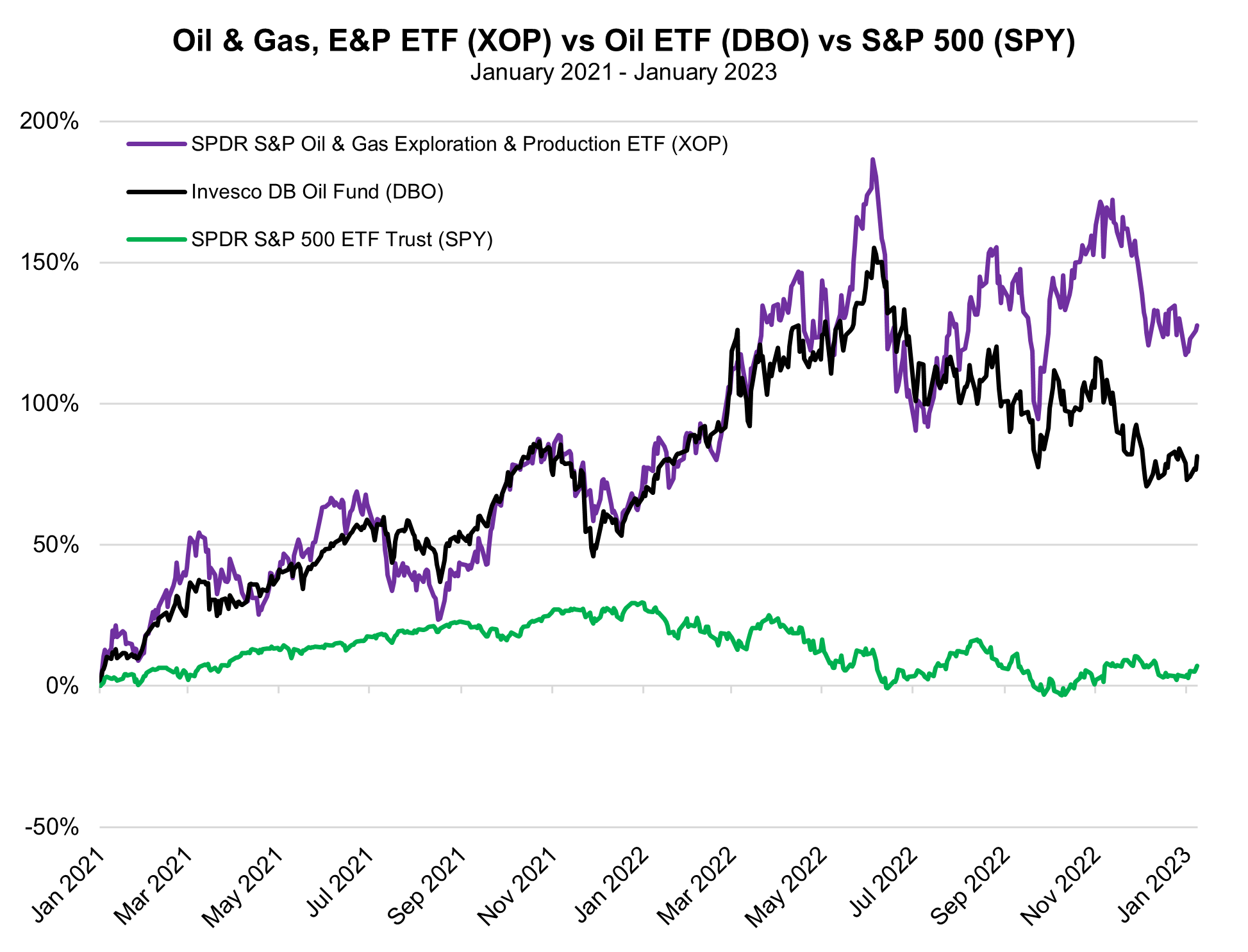

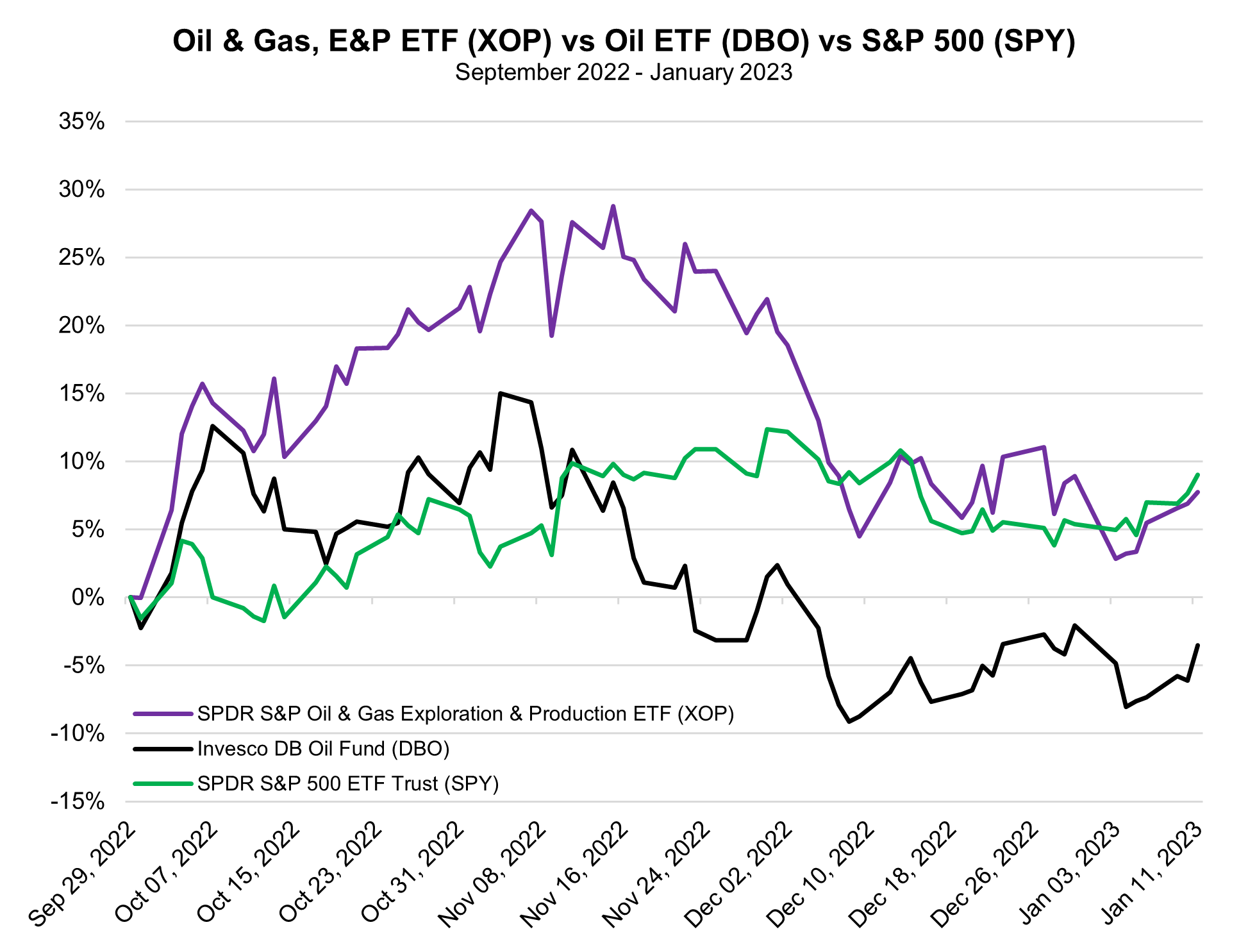

|

Despite a plunge in implied demand to a 20-month low in the first week of 2023, paired with a massive buildup in crude stockpiles surpassing 18 million barrels, oil prices have managed to surge higher this week. Days of supply, which reflects the level of oil in stock relative to current estimates of demand, has made a shocking turnaround in the past several weeks, swinging wildly from a 33-month low of 25.2 in early December to a 19-month high of 29.1 in the most recent week.

That bearish supply data wasn’t enough to derail a fifth straight day of gains for crude futures, which extended their longest winning streak since early October on Wednesday. Part of that can be chalked up to a re-opening of China’s economy as the world’s second largest economy emerges from the economically suppressive “zero-COVID” strategy that was recently abandoned. As of Thursday morning, a soft US CPI print, suggesting prices actually declined -0.1% MoM in December, pushed WTI even higher, close to $79.00 per barrel.

Though commercial stockpiles may have reached a near-term bottom, the continued draining of US emergency supplies has generated ongoing supply risk. The US’s Strategic Petroleum Reserve (SPR), which used to be as large as 656.1 million barrels in 2020, has now been whittled down to its smallest level since 1983 at less than 372.4 million barrels. The combined total of commercial stocks of crude and the SPR closed out 2022 at its thinnest level since 1986. The Biden administration has said they would like to begin re-filling the SPR with fixed-price contracts around $70.00 per barrel, potentially putting a floor below the price of oil. Traders have been aware that WTI crude was nearing the point which the White House’s focus switches from emptying the stockpile to re-filling; essentially, a switch from selling to buying.

However, that switch has yet to occur. After the Biden administration announced they’d be taking bids for a February 2023 delivery worth 3 million barrels of oil, the Department of Energy (DoE) subsequently rejected all offers and told Reuters it would not be “making any award selections for the February delivery window.” It’s unclear if that means the DoE will aim for March instead, or if they are suspending the intended purchase indefinitely, but the department’s protestation seemed to be related to price. Though the Biden Administration has made their desired price point clear, CME crude oil futures do not fall to $70.00 per barrel until June 2025.

The DoE may be getting finicky about price due to a limited amount of funds they have to work with. Through last year’s emergency release, the government sold 180 million barrels at around $96 a barrel, implying $17.3 billion in proceeds. Of that, the Wall Street Journal notes roughly $12.5 billion was stripped away for Congressional use in the latest spending bill. That leaves the DoE with about $4.8 billion of purchasing power. Even if the DOE does manage to refill at $70.00 a barrel, that implies an SPR top-up of less than 70 million barrels, which would only take the SPR back up to 440 million barrels – still similar to 1984 levels.

Despite the pledge to begin re-filling the SPR, emergency stocks are still draining to the tune of millions of barrels per week. More than 3.5 million barrels of crude have been drained from the SPR in the three weeks since Biden announced the US’s intention to begin re-filling the nation’s emergency reserve. If restocking does not take place soon, and the administration chooses to stick with draining the SPR further into 2023, it could increase the risk of a serious energy crisis in the US down the line.

In a further risk to global supplies, Russia and its allies in the OPEC+ coalition have shown they are willing to make significant reductions to oil output to sustain prices, as demonstrated by a massive 2 million bpd cut in October. Prior to the pandemic, OPEC+ would avoid overly aggressive output cuts because the US could backstop production levels and ultimately leverage massive shale output to win a greater market share. However, with US shale about 1 million bpd under previous peak production levels, and the US oil and gas industry hollowed out by more than 100 bankruptcies that occurred in 2020 alone, there is a much smaller threat of the US being able to counter OPEC+ influence in the international market. Goldman Sachs cites OPEC+’s renewed pricing power as a limiting factor to downside risk in crude markets.

|

Leave a Reply