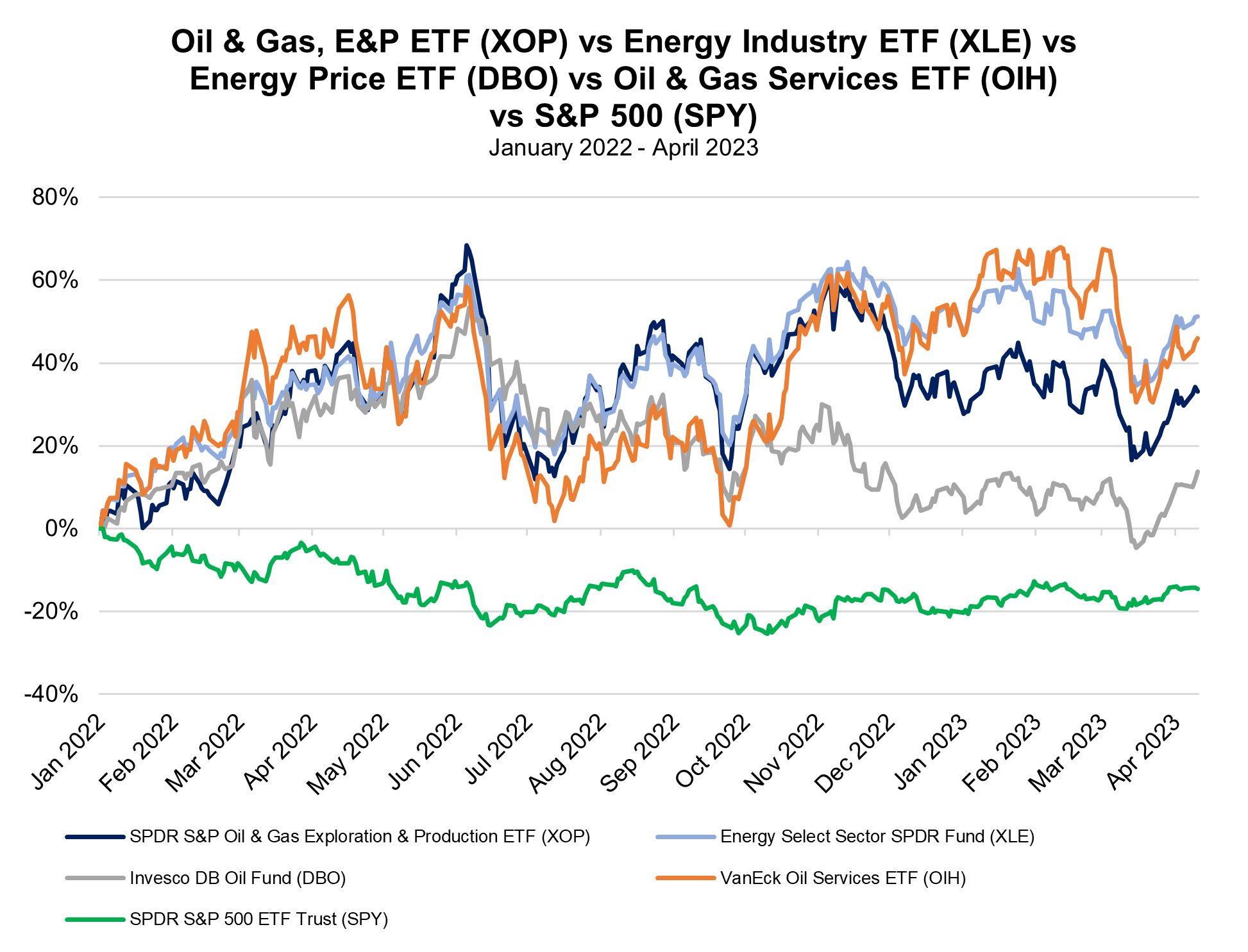

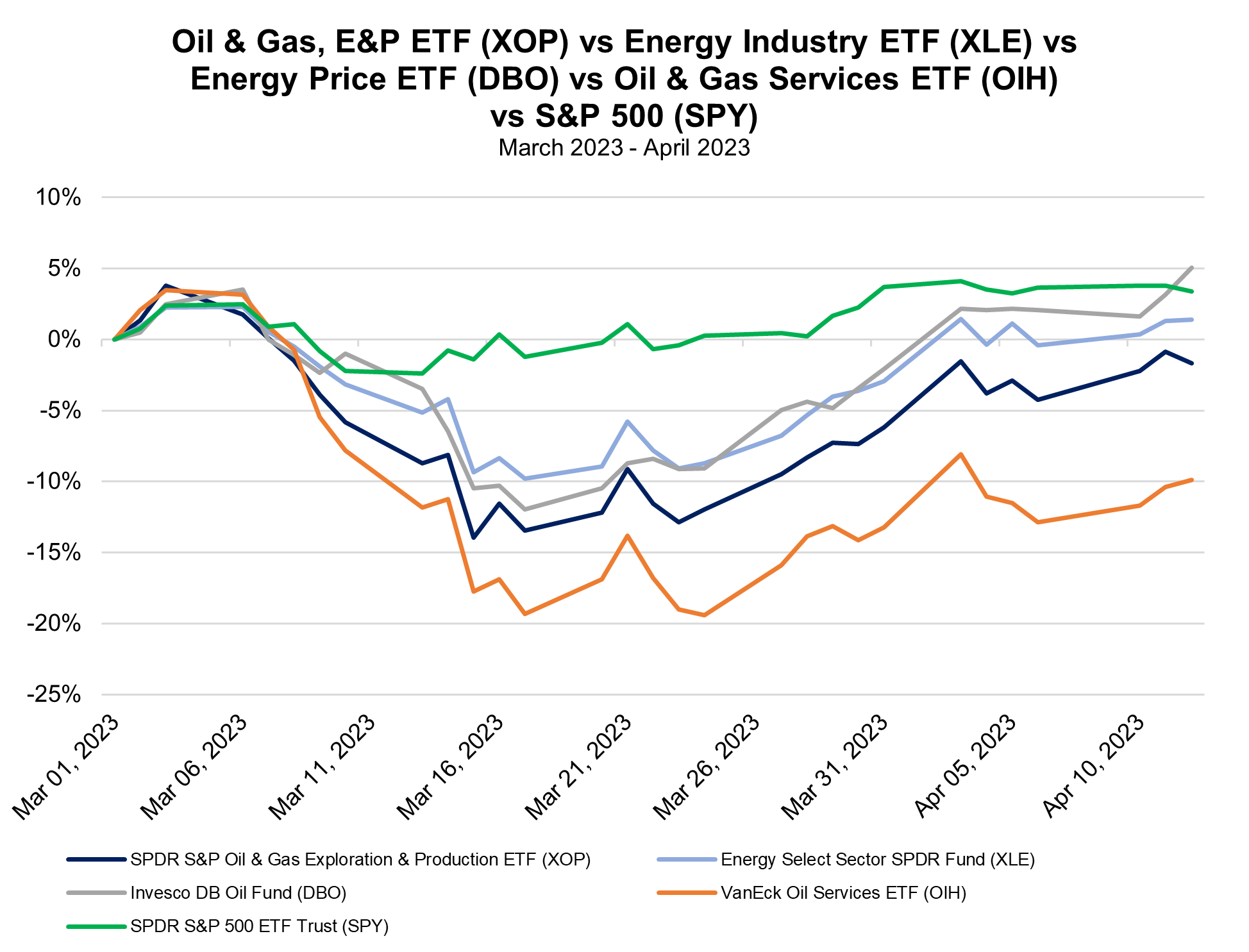

|

The US’s Strategic Petroleum Reserve (SPR), which used to be as large as 656.1 million barrels of crude oil in 2020, has now been whittled down to its thinnest level since November 1983 at less than 369.6 million barrels. Yesterday’s Petroleum Status Report from the Energy Information Administration (EIA) showed a second consecutive draw from the government stockpile, bringing the combined total of commercial stocks of crude and the SPR to a 10-week low in the week to April 7. The majority of the SPR’s decline in the 2022 was related to an unprecedented emergency sale of 180 million barrels, which wrapped up around the start of the new year. In some weeks during that period, the US was dumping more than 8.0 million barrels of SPR crude onto the market to douse flaming hot oil markets.

It took the US just 12 weeks to return to SPR sales of crude oil, with no sign of plans to re-fill the US’s thinning emergency stockpile in sight. As MRP has previously noted, the White House and Department of Energy (DoE) signaled late last year that they’d prepare to initiate a re-filling of the SPR with fixed-price contracts around $70.00 per barrel, but sub-$70 price tags on US benchmark WTI crude came and went with no sign that meaningful SPR purchases were ever on deck. The Biden administration did at one point announce that they’d be taking bids for a February 2023 delivery worth 3 million barrels of oil, but the DoE subsequently rejected all offers to fill the order and told Reuters it would not be “making any award selections for the February delivery window.”

That backpedaling was followed by radio silence on the SPR for several weeks, and then a claim from US energy secretary Jennifer Granholm that it would be “difficult” for the US to go forward with purchases this year due to maintenance at two SPR facilities. This may have been one of the key catalysts behind OPEC+’s recent output reduction of 1.039 million barrels per day (bpd), meant to stem rapidly falling crude oil futures throughout the month of March. Financial Times sources familiar with the thinking of OPEC kingpin Saudi Arabia said Riyadh was irritated that the Biden administration ruled out new crude purchases in such a public way, likely exacerbating downward pressure in oil markets and essentially eliminating a demand-side catalyst many traders may have been pricing in around the $70.00 per barrel level.

The Saudis and several other nations within the OPEC+ syndicate, therefore, may have felt forced to shock the market with an unexpected intervention, which ended up launching prices on WTI crude back above the $80.00 mark. Oil has held those gains and, as of yesterday, surpassed $83.00 per barrel for the first time in 2023. With the addition of the recently announced curbs on supply, OPEC+ will have reduced their 2023 crude oil production targets by roughly 3.657 million bpd through the month of May. According to Reuters calculations, that is equivalent to roughly 3.7% of global demand.

The reaction to cuts by OPEC+ by the White House has thus far been tepid with Granholm reiterating yesterday that the Biden administration plans to refill the SPR soon, but would like to re-fill it at lower oil prices. That re-filling would still be difficult, however, as the US is now stuck selling a mandated 26 million barrels of SPR supplies in fiscal 2023, on top of any other releases that may be in the works. “We cannot sell and take in (crude oil) at the same time,” Granholm said.

Though prices remain relatively extended compared to most of the decade prior to Russia’s invasion of Ukraine, they are subdued enough to have a deflationary effect on broader measures of price inflation going forward, which is the US’s primary concern regarding monetary policy. This time last year, WTI crude was trading north of $105.00 per barrel and continued on in the triple digits through the end of June. If oil prices remained around current levels, the YoY change would be in negative territory until mid-November. Digging into March’s CPI reading, the energy component of the index showed a -6.4% decline on an annual basis, the first time its been negative in 27 months.

Avoiding a further run-up in crude prices from current levels would likely depend on a stable supply-demand balance going forward, but that bet is increasingly tenuous. In a new OPEC report, released this morning, the cartel projected that demand for crude oil is expected to rise by 2.3 million bpd this year. Though the western world is languishing under high interest rates, China is still recovering from its bout with demand-crushing Zero-COVID policies last year. Data on China’s crude oil imports in March showed a surge of 22.5% YoY to the equivalent of 12.3 million bpd, their highest level since June 2020. Interestingly, Reuters notes that the data also showed refined product exports out of China jumped 35.1%, suggesting thirst for gasoline and other finished energy goods was quite robust internationally.

The US has been forced to rely on SPR releases due to a continual struggle to recover and expand domestic production capacity since its energy industry, particularly shale drilling, was thrown on its head in 2020 by more than 100 bankruptcies in that year alone. Prior to the COVID-19 pandemic, OPEC+ would avoid overly aggressive output cuts because US producers could quickly backstop production levels and ultimately leverage massive shale capacity to win a greater market share away from the syndicate. However, with US field production still 800,000 bpd under previous peak production levels, OPEC+ can now act more ambitiously to further their own goals and disregard potential blowback. Pioneer Natural Resources CEO Scott Sheffield believes that the US may eventually recover production above the 13 million bpd threshold, but he’s noted that it will be at a “very slow pace,” taking two and half to three years to match the previous record level.

|

Leave a Reply