Guest post contributed by Warren Fisher of Manole Capital Management, LLC.

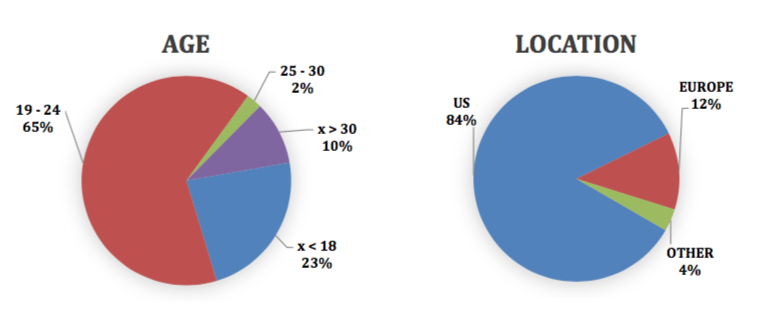

In January and February of 2018, Manole Capital conducted a financial services survey specifically targeting the thoughts and opinions of millennials. Over 175 individuals participated, with nearly 90% under the age of 24 years old. 65% were between the age of 19 and 24 and 23% were 18 or younger. In terms of demographics, 84% were from the United States and 12% were from Europe. For additional information about our survey audience, please contact Manole Capital directly.

Series #1: Banking

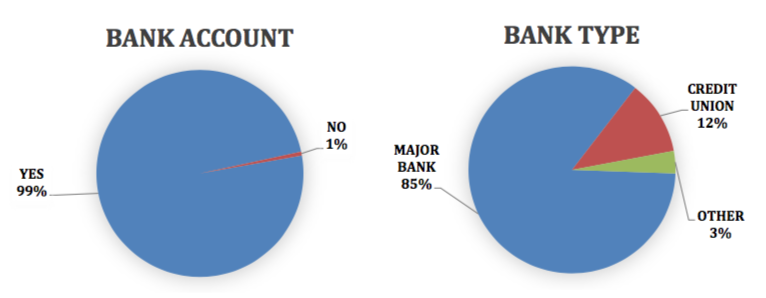

The first series of questions we asked regarding their thoughts and usage of traditional banking services. For 30 years, we have heard that we are going to a “paperless society”, but we are still guilty of printing out documents. For nearly as long, the banking community has worried about younger generations no longer needing a traditional bank account. Well, our first question simply asked if they had a bank account. 99% of our survey said Yes. We then wanted to inquire the type of financial institution they were beginning a relationship with. When asked what best describes your banking relationship, nearly 85% indicated it was a major bank. 12% of those surveyed were banking with smaller credit unions and 3% were with online banks.

Banking:

The most insightful questions regarding the important banking relationship were our next two. We continue to hear comments from banks regarding the usefulness of their physical, branch locations. In a recent sell-side survey, 44% of respondents still identify branches as their most preferred channel for standard banking transactions. A Novantas study found that 60% of Americans prefer to open a new checking account in a branch. This makes sense to us, as people often want financial services on demand and on their own terms. While digital channels are becoming more popular, as our next few survey notes will show, we continue to see surprisingly resilient consumer preference for traditional banking services.

On the low-end and predominantly in rural markets, a financial institution can spend $1 million dollars to purchase land and construct a banking branch. In more metro areas, while land is not purchased, the costs of construction and rent can be much higher. When banks do open facilities, they are often not building traditional 4,000 square foot branches, but instead are focusing on smaller footprints that are one half to one third of their historical size. Commercial real estate firm Jones Lang LaSalle or JLL estimates that US banks could save over $8 billion dollars annually by downsizing their average bank square footage from 5,000 to 3,000. Banks simply have to become more efficient and begin to leverage and capitalize on the new technology they are heavily investing in. A March study, from the Board of Governors of the Federal Reserve, illustrates this point perfectly. It found that more than half of smartphone owners had used mobile banking services in the past 12 months.

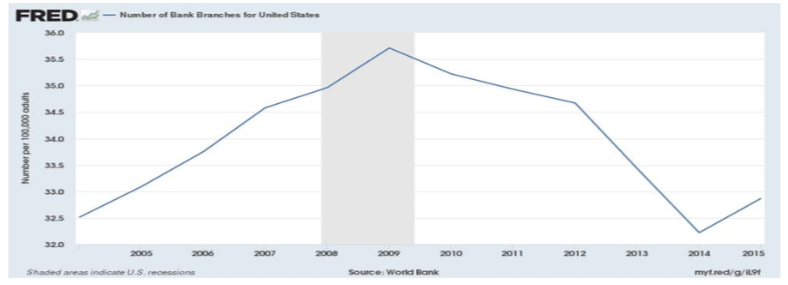

At its recent Analyst Day, JP Morgan indicated a goal of opening 400 new bank branches over the next 5 years. As it expands into 20 new markets, JP Morgan is using its branch infrastructure to attract new customers. We believe that most financial institutions are beginning to re-access their physical footprint and are taking a different tact. The overall number of bank branches continues to decline. JLL estimates that bank branches in the US will decline by 20% over the next 5 years. As the World Bank chart below indicates, the number of US bank branches essentially has not grown over the last decade.

Branches

According to the Federal Deposit Insurance Corporation or FDIC, the United States has just around 95,000 bank branches. Since the Financial Crisis in 2007, the number of bank branches have declined by roughly 8%. In the US, the 10 banks with the most branches accounted for almost 1/3rd of all locations. Not only do these banks have a huge physical presence, but they also dominate in terms of deposits. The top 10 US banks, by branches, also represent over $1 trillion of total deposits.

In our opinion, banks are not just shrinking their physical presence due to industry headwinds and costs, but we believe it is due to the increasing use of mobile banking. We believe the banking battle going forward is not who has the best physical footprint, but rather who has the best mobile applications. Bank of America has estimated that it costs 1/10th as much to process a deposit made through its mobile app, as it does for a teller-assisted deposit. According to JP Morgan Chase, it costs $0.03 to process a mobile deposit versus $0.65 for a branch deposit. If you were an economically savvy financial institution….where would you be investing your capital?

Bank Visits

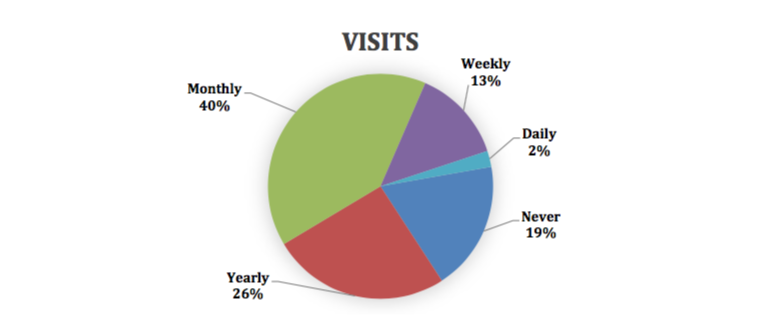

Of our predominantly millennium-aged surveyed individuals, 19% said they “never” visit their bank branch. 26% said they visit a branch once a year. That equates to nearly half of those questioned either never or just one annual visit to a bank branch. 40% said they visit a bank branch monthly, which furthers the point that banks cannot be generating a positive return on investment from their physical locations. While banks must have a physical location to fulfill the needs of certain (i.e.: older) clients, younger generations will not find it necessary or useful to visit a bank branch. Most of these physical visits can be accomplished through ATM visits and check deposits through their cell phones.

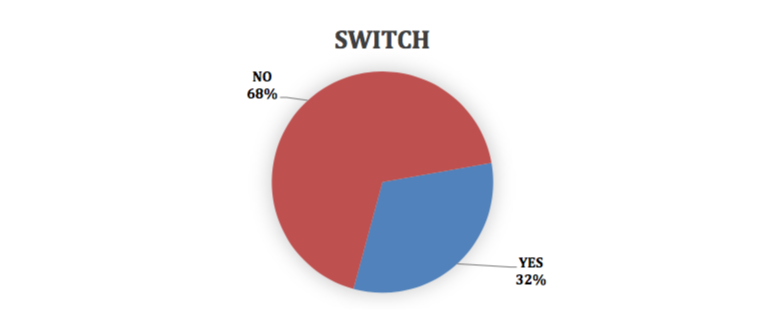

New Entrants

Our favorite banking question was whether or not millennials would be willing to switch from a traditional bank to a major technology company that offered banking services. If Apple or Google or Facebook were to offer banking services, we thought that the vast majority of millennials would be willing to switch. Wow, were we wrong! Nearly 2/3rd’s of those surveyed were not willing to switch to their favorite technology company for banking services.

Banking Conclusions

From our survey we can conclude several things. First, millennials are still feeling the need to open and create a relationship with a traditional bank. When choosing, most are going with major banking institutions. As we suspected, their usage of physical bank branches was not terribly high. This seems to be understood by most banks, that are opening fewer and fewer costly physical locations.

Perhaps our most surprising takeaway was their lack of confidence in major technology companies to provide traditional banking services. We would have thought millennials would be willing to make the switch to an Apple or Google or Facebook, if those entities could provide the necessary banking services to their loyal customers. While strict regulatory rules exist that would prevent these technology players from taking deposits, we do not believe our survey respondents chose “no” due to regulatory rules. There clearly seems to be some “separation of church and state” for younger individuals.

Our biggest takeaway is that millennials are looking for best of breed for any of their interactions. They would prefer to get their hardware from Apple, conduct search through Google and interact with friends on Facebook and Instagram. When it comes to banking, most would prefer to build a relationship with a traditional financial entity. In the future, we believe banks will shift from traditional bank branches and physical locations towards a more digitally based distribution model.

Our portfolio is heavily exposed to companies that provide the key ingredients for banks to offer new technology and services to their customers. This valuable technology is often white-labeled under a bank’s name, but are not developed or managed in- house. For example, products like online banking, remote deposit or check capture and mobile payments are often provided by core, bank outsourcers.

Our next few surveys will be published shortly. Questions asked will focus on the use of cash, ATM visits, and associated fees. Following that series, we will publish our thoughts and findings on data gathered on mobile payment usage, and peer-to-peer payments. Lastly, our fourth series survey will publish the results on brokerage accounts, bitcoin and cryptocurrencies. Stay tuned…

Disclaimer

Firm: Manole Capital Management LLC is a registered investment adviser. The firm is defined to include all accounts managed by Manole Capital Management LLC. In general: This disclaimer applies to this document and the verbal or written comments of any person representing it. The information presented is available for client or potential client use only. This summary, which has been furnished on a confidential basis to the recipient, does not constitute an offer of any securities or investment advisory services, which may be made only by means of a private placement memorandum or similar materials which contain a description of material terms and risks. This summary is intended exclusively for the use of the person it has been delivered to by Warren Fisher and it is not to be reproduced or redistributed to any other person without the prior consent of Warren Fisher. Past Performance: Past performance generally is not, and should not be construed as, an indication of future results. The information provided should not be relied upon as the basis for making any investment decisions or for selecting The Firm. Past portfolio characteristics are not necessarily indicative of future portfolio characteristics and can be changed. Past strategy allocations are not necessarily indicative of future allocations. Strategy allocations are based on the capital used for the strategy mentioned. This document may contain forward-looking statements and projections that are based on current beliefs and assumptions and on information currently available. Risk of Loss: An investment involves a high degree of risk, including the possibility of a total loss thereof. Any investment or strategy managed by The Firm is speculative in nature and there can be no assurance that the investment objective(s) will be achieved. Investors must be prepared to bear the risk of a total loss of their investment. Distribution: Manole Capital expressly prohibits any reproduction, in hard copy, electronic or any other form, or any re-distribution of this presentation to any third party without the prior written consent of Manole. This presentation is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use is contrary to local law or regulation. Additional information: Prospective investors are urged to carefully read the applicable memorandums in its entirety. All information is believed to be reasonable, but involve risks, uncertainties and assumptions and prospective investors may not put undue reliance on any of these statements. Information provided herein is presented as of December 2015 (unless otherwise noted) and is derived from sources Warren Fisher considers reliable, but it cannot guarantee its complete accuracy. Any information may be changed or updated without notice to the recipient. Tax, legal or accounting advice: This presentation is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Any statements of the US federal tax consequences contained in this presentation were not intended to be used and cannot be used to avoid penalties under the US Internal Revenue Code or to promote, market or recommend to another party any tax related matters addressed herein.

Leave a Reply