Contributed by Daniel McConvey, Rossport Investments LLC

In our last thought piece Visiting Mine Sites – A Vital Key to Investment Due Diligence we discussed the importance of mine site visits. This article discusses our views of the nickel market, and also reports on what we have learned from our site visits to nickel plants in China and Indonesia. We conclude on where we think the floor to the nickel price may be and where upside is limited. We then review opportunities to profit from our conclusions.

Nickel spiked to over $50,000 per metric ton (“tonne”) in May 2007, rising 10 fold from its earlier decade lows. That spike marked the beginning of Chinese involvement in the production of a simple but new nickel pig iron (“NPI”) product that has since placed a seemingly ever lowering ceiling over the nickel price. Last year, we decided to go to Asia in an effort to determine how low that ceiling could go. NPI was, and is, produced cheaply in China and more recently in Indonesia. Chinese production uses imported Indonesian or Philippine ore. NPI is then used as feed stock for stainless steel. Stainless steel accounts for more than two thirds of current nickel demand. Historically, the majority of nickel produced was in the form of refined nickel, mined from sulfide ore, concentrated in a mill and then smelted and refined to 99.99% nickel metal. Producing usable nickel products such as nickel matt from oxide ores has been done for decades. However, volumes have been limited due to the fact that oxide ore cannot be concentrated and processing oxide ores has been metallurgically more challenging. About 10 years ago, three large plants were built by three different western mining companies that process oxide ores using High Pressure Acid Leach (“HPAL”) or similar processes. These projects have been dismal failures. Capital costs averaged over $80,000 per tonne of annual capacity. The capital cost blow outs and seemingly perennial “startup” issues that these projects experienced were nothing less than mind blowing. As a result, we don’t expect another Western mining company to build another such plant in the foreseeable future. That is what makes the Chinese foray into NPI so remarkable. Why were they able to find a way to successfully process oxide nickel ore when western companies experienced disasters? That is a story for another time. Suffice to say, some Chinese companies can build good quality capacity for less than $20,000 a tonne of capital cost and they can produce NPI for well less than $10,000 per tonne of operating cost.

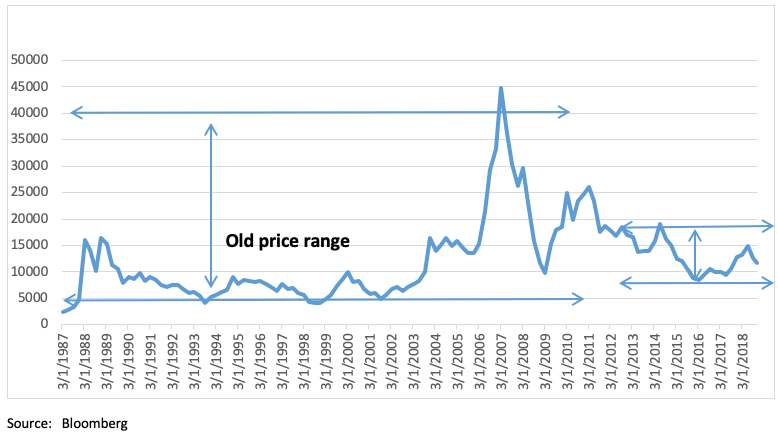

Nickel price per tonne (1987 to present). How much has NPI narrowed the nickel price trading range?

What did we do?

In April 2017, we visited NPI plants in Indonesia and China. We also visited the Jakarta offices of two Chinese NPI producers and a major nickel matt producer. One of these companies was building a stainless steel mill in Indonesia beside their NPI plant. Building the plants side by side allows for about $500 per tonne of power savings by transferring hot NPI to the stainless steel mill. During our visit to China the nickel price fell below $10,000 per tonne. There was clearly pain being felt by company representatives we met. The NPI plant we visited in Indonesia suspended operations a couple of months after our visit. Through our visits and through the Chinese market consultants we contracted with, we estimated the NPI cost structure in China and in Indonesia. During the next several months through January 2018 we talked to other experts and one other NPI project builder in Indonesia who was looking for financing. That company has since failed. We also monitored consultant cost reports.

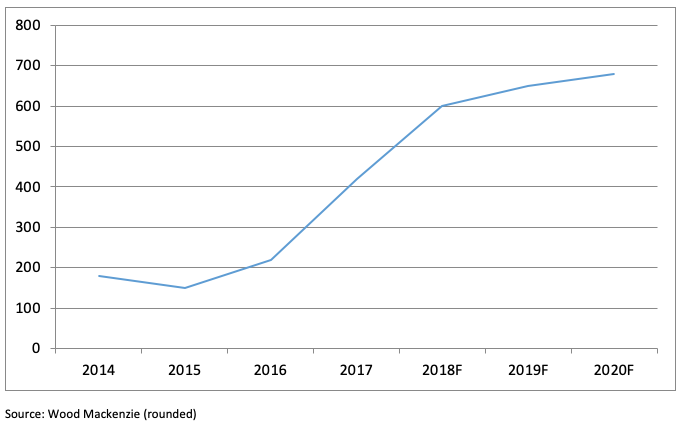

Actual and forecast Indonesian mine production 2014 to 2020 in thousands of tonnes. Global mine production is currently 2,200 k tonnes. As a result, Indonesian mine production is forecast to be more than a quarter of the global total

What did we find?

We found that per tonne all-in sustaining costs (“AISC”) (equal to cash costs plus sustaining capital) is about $10,000 in China and about $7,500 in Indonesia where high grade ore is plentiful. Chinese production comes from imported Indonesian and less desirable Philippine ore. Capital costs per tonne of NPI capacity was about $20,000, which is less than a quarter of the capex cost for western company HPAL processing plants. NPI plants and HPAL plants use very different processes. However, the product is equally valuable in producing stainless steel. We found that the largest Chinese NPI producer was by far the most successful and impressive. The others were mostly struggling especially at then current prices. Expansion plans had been scaled back. We estimated that per tonne incentive prices (i.e. nickel prices that would economically incentivize new capacity) was about $15,000 in China and $13,000 in Indonesia. Assuming it can stay investment friendly for NPI investment and especially Chinese NPI investment, Indonesia is now, by far, the most economical place in the world to add new capacity. Chinese companies can build NPI capacity quickly by western standards. All of this makes Indonesia a swing producer in nickel like we have never seen.

What has happened since January?

As mentioned above, two companies have since not done well. However, the large one has steam rolled ahead and has announced further expansions helped by higher prices. The nickel price spiked to $15,000 in June before falling to below $12,000 at the time of writing. The Chinese RMB and Indonesian rupiah have fallen by about 5% and 10% respectively, maybe reducing costs a little net of some input cost increases. More recently there have been announcements of Chinese companies adding material new HPAL nickel/cobalt production in Indonesia. Unlike NPI, this product is designed suitable for use in batteries for electric vehicles. The low capital cost numbers and the announced speed of building the plants has spooked the market and poured cold water on the positive electrical vehicle story for nickel so prevalent in the market in the past year. However, as per below we are skeptical on these numbers.

What do we think from here?

Assuming that current RMB and IDR exchange rates of 6.9 and 15,100 respectively, do not materially weaken, we think the nickel price floor is likely around $9,000 per tonne. We have high conviction on this. From current sub $12,000 levels we see more upside than downside. Nickel demand growth is expected to be robust in the next decade. Outside of Indonesia incentive prices for new nickel capacity is around $15,000 and many mines are depleting. The recent scare over a possible blitz of new Chinese company financed HPAL battery grade nickel is overdone. The cost and timeframe announced for the biggest proposed plant do not make sense to us and unlike NPI, HPAL is not a technology of known Chinese expertise. Over the next decade, for a whole host of reasons including environmental, foreign exchange rates, labor costs, stripping ratios and ore grades we believe production costs in Indonesia will rise by at least 50% raising the nickel price floor. In our view, if for environmental, political or other reasons production in Indonesia was materially upset in the future, this would shock the market and result in a huge upside to prices. The world will be hungry for increased nickel supply in the next decade or two. That said, in the current Indonesian-Chinese investment environment, medium term spikes in nickel prices will lead fairly rapidly to supply responses with new Indonesian capacity and higher utilization of Chinese NPI facilities. This may cap annual average nickel prices somewhere not far above $15,000 in the next two to three years.

What are some opportunities to profit from these conclusions?

- We seek to invest in nickel producers that can yield good returns at $13,000 per tonne nickel.

- We are looking at public companies that are partnering with the best Chinese NPI producers.

- We will look to go materially long nickel related investments when nickel prices approach our estimated $9,000 per tonne cost floor and look to be neutral to short nickel related investments at prices over $15,000 per tonne. This assumes nickel related investments discount spot prices.

- We will go aggressively long nickel investments if we foresee production disruptions in Indonesia for environmental, political or other reasons.

Rossport Investments specializes in the metals and mining sector. If you would like more information on our work and views on nickel, please contact Daniel McConvey at (646) 722-4119 or by email at daniel.mcconvey@rossport.com.

Leave a Reply