The following post is courtesy of Diane Harrison who is principal and owner of Panegyric Marketing, a strategic marketing communications firm founded in 2002 specializing in alternative assets.

With much active marketing and sales efforts on a long-term pause in 2020, I’ve had several conversations with managers looking to retool their sales story for 2021. Some are coming to market with a new investment product and some just want to expand their selling activities to a wider segment of the market, but all have the goal of coming up with a compelling reason for new investors to give their product a try.

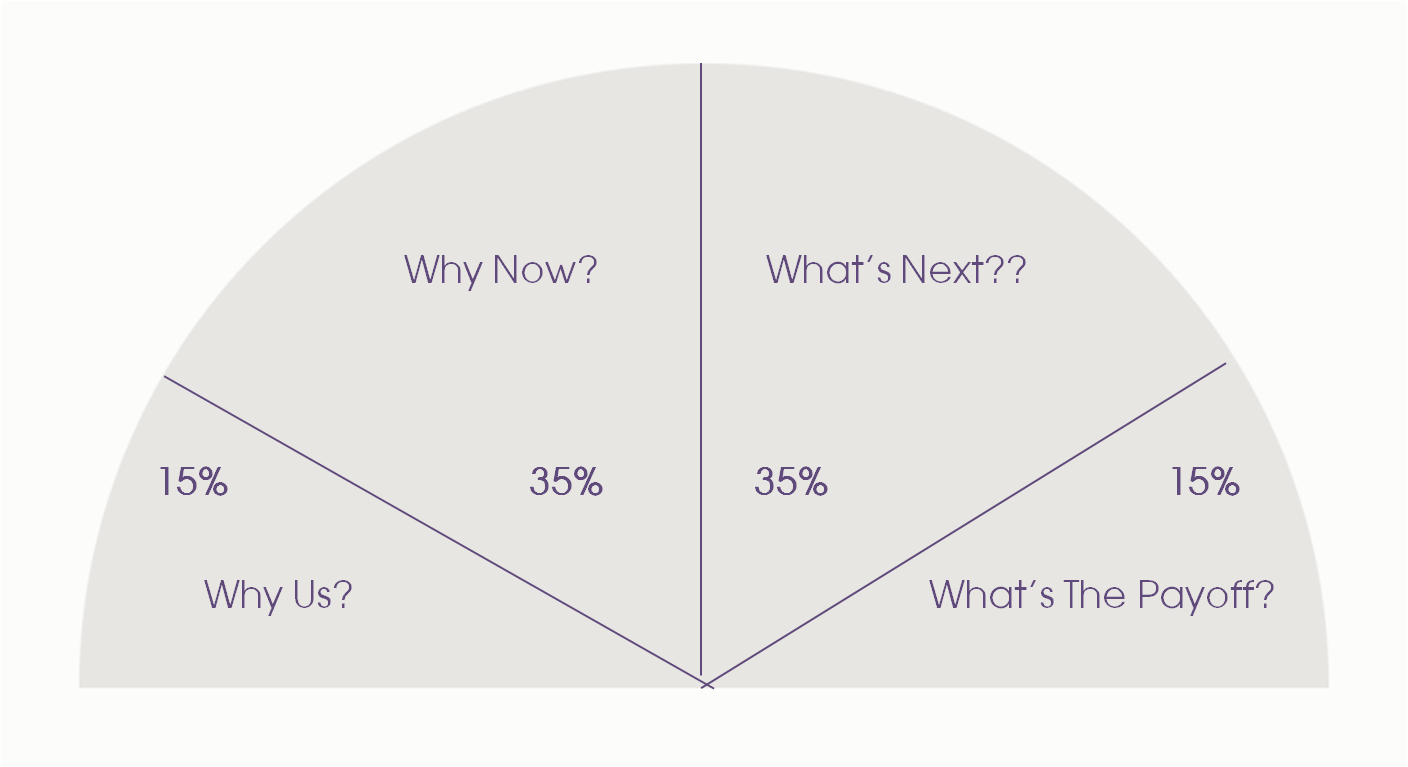

A trend among these managers, both this year and in years past, is to have much too strong an emphasis on telling the story of the past versus painting the vision of where they want to go. New investors are far less interested in what the manager has done for others than they are in understanding what that manager can bring to this new product and a future result as they consider joining forces with them as limited partners. A good balance for telling a solid sales pitch is what I call the 15-35-35-15 balance. The graphic below helps illustrate this weighting.

15%: Why Us? If you consider most sales pitch decks to be 15-20 slides in length, you should be able to devote 2-3 slides to cover the information that falls into this bucket, such as:

- What have we done in the past? This should focus on functional, abbreviated biographical information for key team members that supports the role they will play in the new offering. Save full-on resume data for an appendix or subscription document for those that care to read through all of it.

- Why are we setting up this fund? Most managers take an enormous hit economically when they leave a position working for others to start their own fund and bear the not insignificant costs of doing so. Investors know this, and need to hear from the founders why they undertook such a costly move.

- Where does this fund sit in the universe of offerings? This means the offering needs to sit within some investment bucket that investors can understand. They will need to take funds from somewhere in their holdings to invest in the offering, and that issue matters to them as they consider overall allocation planning.

35%: Why Now? The heart of the pitch resides in the Why Now? and What’s Next? sections. This is creating the construct for selling the product, so 10-12 slides should be devoted to these two sections. Within the Why Now? Portion, managers should answer:

- How do you see the market providing a strong opportunity for this fund effort? If your offering is a specialty fund, or a lesser known approach to the market, you will need to provide this context for its attractiveness to prospects unfamiliar with the sectors or strategies involved.

- What trends support your views on this (supported by industry data, where appropriate)? Most managers are very comfortable with packing their decks with analytical data in support of the research and investment work they are so involved in on a daily basis. However, less is more when using this information to convince investors who will NOT be spending their time poring over such microeconomic data. Pick 3-4 concise industry data to help illustrate the market opportunity and leave it at that.

- How the approach the new offering takes fits into this current climate, creating an ideal time to expand its size. Once you’ve laid out the current market trends and opportunities, explain how you see this new offering fitting into the current climate and how you envision its expansion to an optimal size.

35%: What’s Next? The other main section of a strong pitch deals with anticipatory expectations about the prospects for success in building the fund through its expansion of strategy or implementation. Prospective investors are more than just curious about what is likely to be done once their investment is taken into the fund. Questions that should be addressed in this area include:

- With the additional capital raised, how does that change the fund’s focus on deals to be sought?

- What will more funding do for an examination of the market opportunities than might have previously been unavailable to the manager?

- As the fund size grows, are there internal needs that will be addressed, such as adding more investment/research strength, upgrading operational issues, etc?

This section is one I often see ignored, but it bears repeating that investors, once they reach the stage of considering buying into an investment, want to have an understanding of the growth plans for better deal sourcing, a larger portfolio, access to additional market segments previously unavailable due to fund capital constraints, the build out of both professional staff and operations to keep pace with a larger investment effort, etc.

15%: What’s The Payoff? Finally, there is the information that should close out the final 2-3 slides to give prospects the information they most care about: what kind of return am I getting for my risk in partnering with you?

- A clean summary of net returns (real if the fund has a track record, anticipated if a start up with appropriate footnoting and disclaimers)

- Fund terms and service providers, and any other fund structure information that an investor needs to know before making a final decision on investing

- If there are several classes of shares, that should be explained

- Ii there are hurdles or benchmarks, these should be disclosed

Any other information that you may feel you want to include in a deck should be considered for a back appendix section so it doesn’t cloud the story arc as outlined above. Follow this format and see if it doesn’t sharpen your sales pitch for 2021

Leave a Reply