By Daniel McConvey, Rossport Investments LLC

We are mildly cautious on the gold price for 2021 as we expect some of the factors that drove it to record highs in 2020 will begin to reverse. As the world moves somewhat back towards normal, we think the financial shock and volatility resulting from Covid-19 (Covid) will abate, causing downward pressure on the gold price from current $1,880 per ounce levels. As that happens, we think the huge investor buying on Covid fears (including record ETF buying as per Tables 1 and 2 below) that drove gold to historic highs this year will also abate. This investor buying concern is highlighted in our supply demand section below. That said, while gold mining margins may have some downside from current near bonanza levels, we think robust incentive level pricing may remain for years. While prices can overshoot in both directions, gold prices are likely supported below $1600 (above pre-Covid prices) in 2021 as not all of the financial market damage done this year is going away. Further, gold’s 2020 rise is muted in other currencies with the euro price up now only 14% year to date (see Figure 2 below). We see gold trading mainly in the $1600 to $2000 range in 2021 with the average in the bottom half of that range and with the second half weaker than the first half of the year. A weaker than expected global recovery and/or a further fall in bond yields (see Figure 3) are key risks to our view.

In our mid-August article titled “Outlook for Gold – Challenges for Further Price Appreciation” (https://hedgeconnection.com/blog/?p=11979) we explained why we were neutral gold at then $1940 and €1640. Prices have fallen 3% and 6% to $1880 and €1540 since then. Despite slightly lower gold prices, we have become a notch more cautious as the protests of mid-year and the risks of chaos around the US elections and of a Trump re-election that we discussed in August may be largely (albeit not all) behind us. Also Covid vaccines have progressed faster than we expected then. The light of a more normal world can be seen at the end of the tunnel although there are still clouds outside of it.

In this piece we analyze the gold market in two ways. First, on a largely qualitative level and then on a supply demand level. The later analysis is what makes us more cautious.

Global Views and Assumptions for 2021

The following are our main global views and assumptions for 2021. By next summer herd immunity to Covid will exist in the developed world and hopefully most of the rest of the world before year end. By late summer the world will be traveling again. The global economy will bounce back in a V-shaped recovery. Equity markets will stay fairly stable from current strong levels. Unemployment will continue to fall. President Elect Biden’s administration will have some success restoring and repairing western world alliances and institutions. A more coherent western world voice towards China, Russia and global trouble spots will materialize. Near zero US and Euro short-term interest rates will remain for at least three years. The dollar will weaken from current levels (€ = $1.22 currently) but by less than 10%. Inflation will stay low and the US 10 year bond yield will stay below 1.5% (currently at 0.9%) for 2021. A spike in these yields toward two percent would hurt gold. Finally, Republicans will remain in control of the US Senate after the January Georgia Senate runoff elections putting the brakes on the Democrats hopes of huge stimulus spending and reducing the downside for the dollar.

Part I: Key Reasons for Our Mildly Cautious View

Let’s now look in more detail at our key reasons for our mildly cautious 2021 call:

- The world will move back towards normal as the pandemic begins dissipating bringing an improved economy, a huge psychological lift and less of an urge for safe heaven asset buying. As per Table 1 below, we forecast ETF buying will fall by 500 tonnes (i.e. by half) from estimated 2020 levels. That is over 10% of a roughly 4,500 tonne gold market;

- Geopolitical tensions including trade wars are likely to fall with the expected re-engagement of the US with western countries and alliances;

- US and Euro bond yields should rise modestly, though Euro yields will stay largely negative;

- Annual central bank purchases may not return to their pre-Covid levels of 600-700 tonnes in 2021;

- And finally, we expect mine production will rebound from depressed 2020 levels adding roughly 300 tonnes to the market.

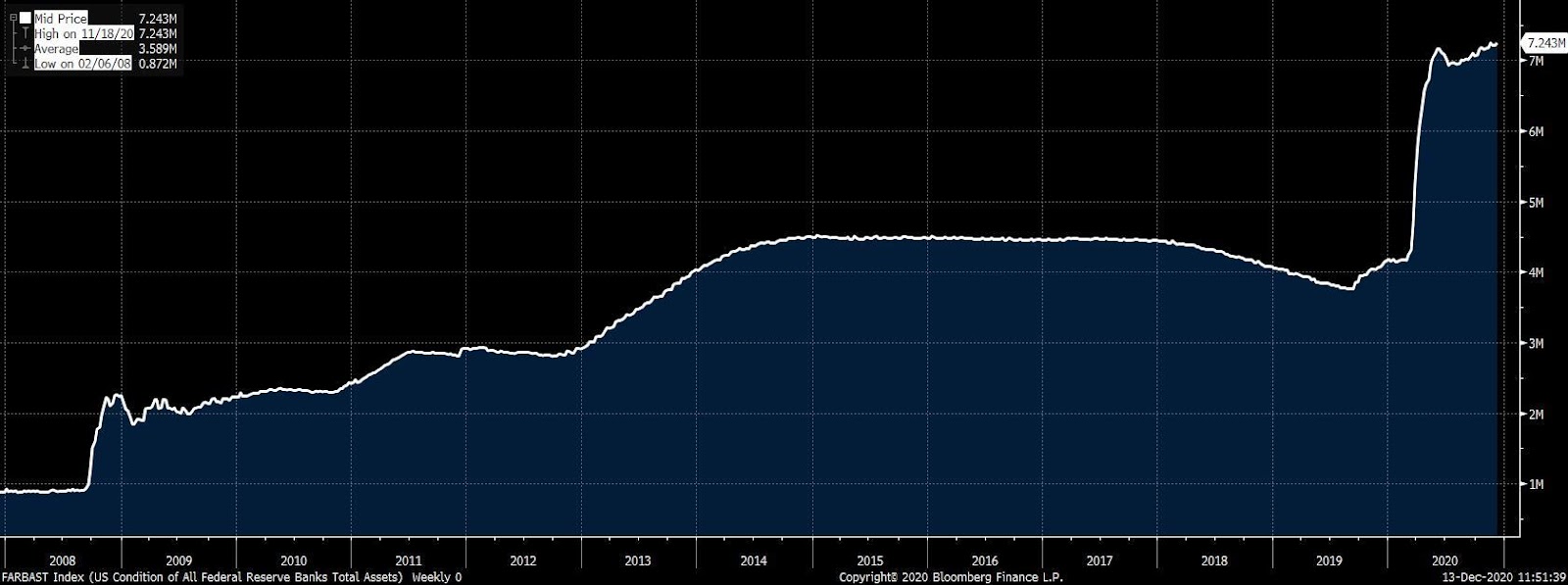

As we stated in August our bias is to be cautious. However, we are far from big bears on gold at current $1880 levels. The deficits and expansion of Western World central bank and government balance sheets (see Figure 1 below) that came with the pandemic are not going away any time soon. This Covid hit is the second hit to these balance sheets in a dozen years and those balance sheets did not recover from the first one.

Figure 1: US Federal Reserve Balance Sheet 2007-2020

The Fed’s balance sheet doubled to $2 trillion during the 2008-2009 global financial crisis and it kept growing afterward with continued “QE”. In massive easing actions during the Covid crisis this year the Fed has come close to doubling the size of the balance sheet again to over $7 trillion. The ECB also continues to aggressively grow its balance sheet. While some of this increase will likely be reversed in 2021, we have seen another step change uplift. This huge increase in central bank assets can only weaken one’s confidence in fiat currency and in our view raises the floor on the gold price and other safe heaven assets.

Aging populations and higher sovereign debt levels make the task of growing GDP and reducing deficits harder. In short, the chances of currency debasement, however remote, are now less remote. And, if we are materially wrong on our many above assumptions, gold could easily surprise us on the upside. On a longer term basis the attractiveness of owning some gold in one’s portfolio may only have gone up with the pandemic despite the rise in prices.

The following are other factors supportive of the gold price. First, while President Trump lost the election his movement is not going away soon. President Trump and his supporters are continuing to challenge the November 3 Presidential election results and seemingly democracy itself. It seems surreal and contagion is a large worry. Second, the large damage done to a once near rock solid western world alliances will not be fully reversed by the Biden administration. The evil genie seems out of the bottle in the form of rogue governments whose actions are now less checked making the world a more dangerous place. Third, the US dollar is expected to continue weakening at least modestly. Fifth, oil prices are expected to rise raising cost curves of gold companies. Finally, as discussed below, jewelry demand especially in emerging markets should rebound from historic lows with the economic recovery and stronger forecasted local exchange rates.

Figure 2: Gold in US$, Aus$, Cdn$ and Euro 2020 YTD

In Euro (white line) and Aus$ (green line) terms gold is now only up 12-13% YTD 2020. Prices are down in all currencies around 10-15% from their early August peaks. However, it is important to remember all prices are still up around 35-45% in all currencies from year end 2018 when prices were about $1280 and €1120. Since early December the dollar has shown new weakness.

Ultimately, over the years increased mine production incentivized by these high prices may bring gold prices down if other factors don’t. However, except for artisanal production which may represent about 20% of the market, a significant step up in global mine production will take years due to long lead times needed for development. Further, an exploding ESG movement may make funding and building some large footprint mine expansions and new mines materially more difficult. Therefore, at least for the next two to three years we think that gold prices will stay at robust levels for miners and make smaller footprint gold projects profitable.

Part II: Gold from a Supply and Demand View

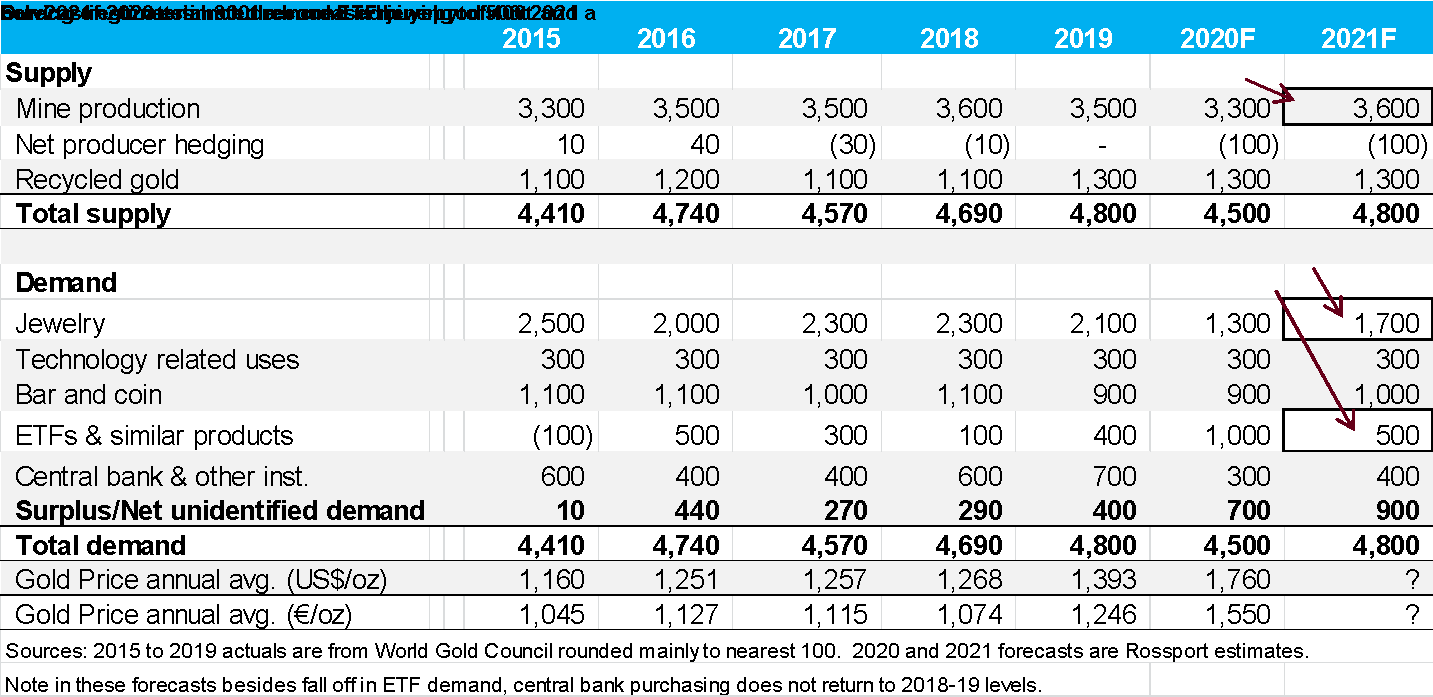

The global gold market as per the table below is between 4,000 and 5,000 tonnes and has been about that for the last two decades. While mine supply has grown about 1,000 tonnes in 20 years central banks have gone from being net sellers to net buyers.

Table 1: Gold Supply and Demand Estimates

Table 1 above is a supply/demand analysis that uses World Gold Council (WGC) rounded estimates for 2015-2019 and our forecasts for 2020 and 2021. Our 2020 forecasts have the benefit of WGC’s September year to date estimates. The “Surplus” (Net unidentified demand) is a force that reflects estimation error on other line items. This estimation error reduces over time as more information becomes available about a given year. The WGC’s September 2020 YTD Surplus is about 500 tonnes making our fourth quarter Surplus about 200 tonnes. These are big numbers as can be seen by comparing to prior years.

These line items estimates range materially in their difficulty. Mine supply and ETF demand are the most supported estimates as a high percent of mine supply is trackable and ETF demand is disclosed. Recycled gold is the softest number being very difficult to estimate. Jewelry demand is again a soft estimate as a lot of jewelry demand comes from India and other countries where jewelry is also an important store of wealth and fabricators are many. Bar and coin demand is mixed in terms of estimation difficulty. The many soft estimates are what leads to the material Surplus or net unidentified demand.

More net unidentified demand appears needed in 2021 if the expected global V- shaped vaccine led economic recovery largely reverses the forces that led to gold’s powerful rise this year. Accordingly, we forecast ETF demand to fall and jewelry demand to rise. As per Table 2 below, ETF demand this year has continued to be primarily US based. Since October global ETF buying has started to fall and positions are now down about 150 tonnes from peak levels. We have ETF investment falling in half to 500 tonnes. We have jewelry demand increasing by 400 tonnes from very low levels. However, we expect jewelry demand to stay below 2019 levels. Our analysis forces out 900 tonnes of needed net unidentified demand. This worries us some and it would worry us more if not for the large 700 tonne unidentified demand this year.

Table 2: November 2020 YTD increase in Gold ETFs in tonnes

North America has accounted for almost two thirds of ETF demand this year.

Note: WGC figures in the above table are slightly higher than recorded on Bloomberg.

Risks to our View

The many risks to our view center on one or more of our above stated assumptions being wrong. The largest upside risk to the gold price would be that the global economic recovery coming out of the Covid pandemic becomes more rocky than expected and more market and geopolitical issues arise keeping central banks easing even more in any way they can. As per Figure 3 below, if the share of global investment grade bonds with negative yields keeps growing, gold could surprise to the upside. Another upside risk would be a larger than forecast fall in the US dollar. Of note, the impressive rise in the gold price from $1775 to $1880 this month was helped by a sharp weakening of the US dollar. Conversely, a downside risk scenario would be that the global recovery happens smoother than expected bringing materially lower unemployment in the US and Europe and an expectation of positive real interest rates coming faster than expected despite current Fed and ECB commitments to keep near term rates low for about the next four years.

Figure 3: Global Negative Yielding Debt Now $18 TRILLION or $27% of Global Investment Grade Bonds

In terms of risks to the upside to our gold view, this graph plays in our minds. $1 Trillion (over 5%) more in bonds tipped into negative yielding territory to reach record levels last week. Clearly, the passing of US elections is not calming all gold market tailwinds. Negative bond yields motivate hard asset buying including gold ETF buying. We expect bond yields to slowly rise in 2021 and thus this graph to turn. If that does not happen gold could surprise on the upside.

Rossport Investments LLC specializes in the metals and mining sector. If you would like more information on our work and views, please contact Daniel McConvey at (646) 722-4119 or by email at daniel.mcconvey@rossport.com.

Note: Past performance is not necessarily indicative of future results. Forward-looking statements reflect the Investment Manager’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond the manager’s control. Investors are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document.

Leave a Reply