Contributed by Warren Fisher of Manole Capital Management

Over the next weeks, we will address some FINTECH-specific issues. The first is retail trading, the arrival of Wall Street Bets and the upcoming Robinhood IPO. The next FINTECH theme is digital currencies, Bitcoin and the Coinbase IPO. The third topic is digital, mobile and contactless payments, as well as details from the 2020 holiday shopping season. The final FINTECH topic discusses how FINTECH companies are “nimble”, Visa’s failed acquisition of Plaid and the emergence of BNPL (buy now, pay later).

FINTECH Theme #1 Trading

Before we discuss retail trading and the explosion of volumes, we should start by addressing the IPO and SPAC marketplace. Clearly, the capital raising “window is open”.

IPOs & SPACs

As we discussed in last quarter’s newsletter, the SPAC (special purpose acquisition companies) and IPO (initial public offerings) markets are “on fire.” According to Dealogic, 2020 was a record year for the US IPO market, as companies raised $167 billion through 454 offerings. The prior full-year record was set in 1999, during the Dot Com era at $108 billion. Capital raised by SPACs last year more than quintupled, across over 200 offerings (per S&P Global data). January 2021 was the best January for IPOs in more than 25 years, with 116 companies raising $39 billion. Over the last 3 months of 2020, 39 SPACs announced transactions. These SPACs climbed an average of +5.4% on the day of their announcement and were an average of +16% higher over the next month (per Dow Jones market data).

Affirm (ticker AFRM) is a BNPL (buy now, pay later) company that we will discuss later in the newsletter. After the enormous success of its early January’s IPO, which more than doubled from its initial offering price, we envision the 2021 market for FINTECH IPOs should remain strong.

Other FINTECH companies are taking the SPAC route, with Social Finance or

SoFi as a recent example. SoFi agreed to be acquired by a SPAC (Social Capital Hedosophia Holdings), with an implied valuation of $8.65 billion. The SPAC purchasing SoFi immediately advanced +63% upon the annuncement. SoFi has 1.8 million members and started as a student-loan refinancing business. It has received preliminary approval from the US Office of the Comptroller of the Currency to receive its much sought-after national bank charter and has branched into mortgages, personal loans, credit card refinancing, insurance and investing accounts.

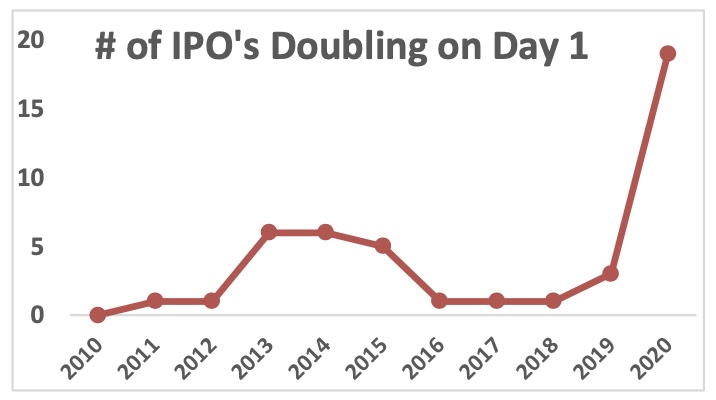

The banks that manage the IPO process are supposed to equally weigh supply and demand dynamics to ensure the company going public raises as much money as possible. However, brokerages are signficantly underpricing these deals and have underappreciated retail interest. By underpricing the initial price, these brokerages are doing a disservice to the newly public company by not raising as much capital as it should have received.

Nineteen IPOs have doubled on their first day of trading this year, significantly more than in any year over the last decade. It looks like these banks have significantly underestimated demand, to the detriment of their now public company clients.

Two of 2021’s potentially largest IPOs are both in our FINTECH space – Robinhood and Coinbase.

Trading Volumes

We believe that this growth was spurred by a historic event in the fall of 2019. While there have been commission-free trading shops around for years, the announcement by Schwab (ticker SCHW) on October 2nd, 2019, to permit commission-free trading was historic. We believe this action by Schwab was recognition of the strong account growth (primarily in the Gen-Z demographic) from upstart rival Robinhood. Once Schwab went commission-free, TD Ameritrade (ticker AMTD), E*Trade (ticker ETFC), Fidelity (private) and others quickly followed. This ultimately led to industry consolidation, as Schwab bought TD Ameritrade for $26 billion and Morgan Stanley purchased E*Trade for $13 billion.

The retail investor is back, so individual investors need to be considered and better understood. Although some retail accounts might be small in size, they collectively have become a powerful force. Historically, institutional and professional investors were the main cohort that mattered to publicly traded firms. Now, according to Citadel Securities, individual investors account for roughly 20% of the daily stock-market activity which is double its market share in 2019.

Overall, volumes soared in 2020, and many online brokerages catering to individual retail traders drove this growth. Specifically, equity and options experienced huge increases in volumes last year, with year-over-year increases of +55% and +58% respectively. In 2020, equities averaged 10.9 billion shares per day, while options climbed to 27.7 million contracts per day, both all-time records. Sandler Piper research shows that TRF (trade reporting facility) volumes are on record pace. In January of 2021, average volumes are over 2x the average in 2019. On January 27th, US equity share volumes set an all-time record of 24.5 billion shares traded. In addition, US equity options volumes also set a record of 57.1 million contracts.

All trading is not equal. While equity trading is “free,” option trading still remains quite profitable for the online brokers. Brokerages also earn revenue from margin loans, securities lending and PFOF (payment for order flow). The website Wolfstreet reports that margin debt last month stood at a US record of $778 billion, up over +40% year-over-year.

Besides commissions, the capability to fractionalize trade stocks (down to $1 increments) is an interesting trend worth watching. With dozens of stocks in the hundreds per share and seven companies in the S&P 500 with share prices above $1,000 per share, fractional investing is a wonderful opportunity to make certain popular stocks more accessible to smaller, retail investors. It isn’t just the high-priced and popular stocks that are being traded in fractions. By mid-January 2021, six of the top 10 most active stocks were all priced under $1 per share. These 10 stocks traded a combined 2.6 billion shares or roughly 18% of the entire stock market.

Retail trading in certain names has obviously increased volatility. Over the last week or two, many “hot stocks” have experienced intraday volatility over 70%, compared to the overall market (using the S&P 500) of 1.5%. On certain days recently, these companies have made up a whopping 4% to 8% of total shares traded (per Piper Sandler Research).

Retail Traders

Once the online brokerage industry embraced commission- free trading, a new generation of investors emerged. Millennials and Gen-Z investors flocked to firms like Robinhood, with their mobile-based trading platforms that are simple to navigate and use. Wall Street, with traditional sell-side research, has lost a considerable amount of market share to newer FINTECH brokerage firms.

As retail consumers became enthralled with the stock market, they opened more than 10 million new brokerage accounts opened at firms like Fidelity, Schwab, TD Ameritrade, Robinhood, E*Trade, etc. By the summer of 2020, Robinhood was doing an average of 4.3 million trades per day, which exceeded the 3.8 million at TD Ameritrade, 1.8 million at Charles Schwab and 1.1 million at E*Trade.

In our opinion, the mentality of the new retail investor is very much anti-Wall Street. They have a healthy distrust of “the suits” and boring index funds. Plus, these investors seem to enjoy stock picking and tend to conduct their own version of research through real-life experiences. Without the worry of annoying commissions, these investors can transact when they want on whatever device they wish. We have no idea when these volumes will slow, but we do believe that the zero-commission trading environment helped spur this new trend.

Wall Street Bets

Normally, when the Fed decides on monetary policy, it is the financial story of the day. On January 27th, 2021, the Fed decided to leave its monetary policies in place, with no announced changes to its interest rates. It stated that it is nowhere near exiting its massive support for the economy and repeated its pledge to maintain its bond buying program. Policymakers had a cautious tone, as they worried about an economic slowdown and the overall pace of the recovery.

The market yawned at the Fed’s comments and instead was focused on several million traders on Reddit, known as Wall Street Bets. Across Wall Street, this group of retail traders is having a meaningful impact on a few heavily shorted stocks. Whether through equity purchases or out-of-the-money options, this group has dramatically pushed certain positions higher, to the detriment of a group of hedge funds that are short the names. Eye-popping rallies, by companies once left for dead, are the talk of Wall Street. A war has broken out between short-selling hedge fund professionals, who are losing billions, versus individual retail investors. By using social media, this new powerhouse has piled into hot stocks and overloaded trading platforms from Robinhood to TD Ameritrade to Schwab and E*Trade.

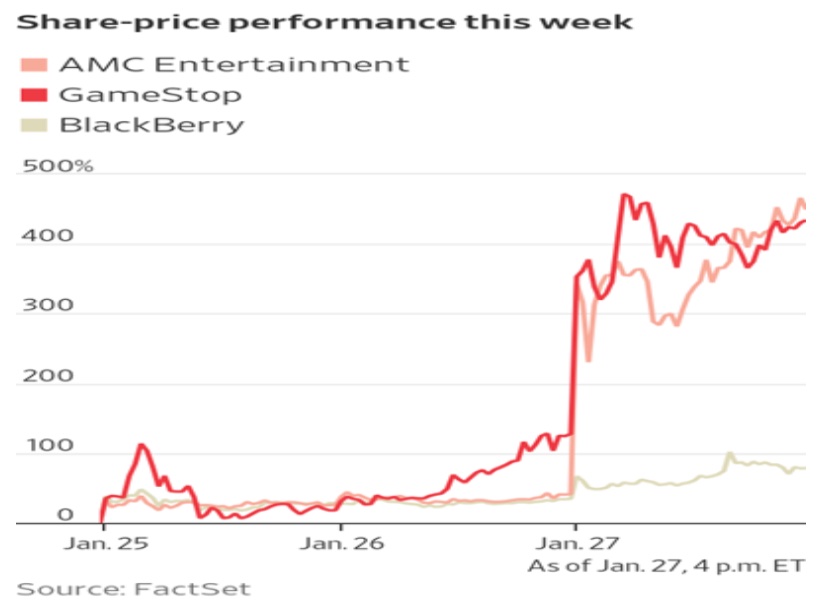

Just take a look at this 3-day chart for Gamestop (ticker GME), AMC Entertainment (ticker AMC) and BlackBerry (ticker BB). On Wednesday the 27th of January, AMC rose +301% and GME climbed +134%. Heck, BLIAQ, the company responsible for liquidating Blockbuster’s operations, somehow doubled. How crazy is the market getting? Well, there is a small Australian mining company called GME Resources. Despite trading on the Australian exchange, it has a ticker of GME (just like Gamestop). The mining company saw a +20% increase in its stock price last week, as the retail crowd mistakenly purchased the wrong GME.

The price action in these stocks is completely divorced from the fundamentals of their businesses. This can happen for a few days, maybe even weeks, but eventually the fundamentals of a business begin to drive stock price performance. In our opinion, it shows the power of the retail investor base and how individuals can still influence the market. Is this a shift away from large, institutional players? Is this the start of a bigger trend or just a passing, but fascinating curiosity? How long will it last? Will a pullback happen? Absolutely! Stocks cannot climb +1,750% year-to-date (as GME did) without a fundamental reason.

Every good story needs a couple of main characters. During with GME’s meteoric rise, then chaotic decline (and whatever happens next), the “bad guys” were initially the hedge funds that were short these names. Then, another character surprisingly emerged as another villain. On January 28th, millions of retail traders continued buying of these “hot” stocks on their preferred and favorite platform – Robinhood. When Robinhood restricted trading in GME (and some other heavily shorted names), all hell broke loose.

Robinhood released a statement that said “in light of recent volatility, we are restricting transactions for certain securities to position closing only.” Then, it cited clearinghouse requirements for the trading stoppage, which “exist to protect investors and the markets.” From what we can gather, it comes down to the middle man and clearinghouse capital requirements. When volatility and volumes increase, the clearinghouses for US equity and option trading (the DTC/NSCC and the OCC) can ask brokerages for additional capital. Requiring brokerages to post greater amounts of capital is not uncommon, especially during times of stress and uncertainty. Over the course of a week, Robinhood raised a total of $3.4 billion to shore up its capital base.

Robinhood said, “As a brokerage firm, we have many financial requirements, including SEC net capital obligations and clearinghouse deposits.” As these Congressional hearings take place, we might see the spotlight return to PFOF, as well as how brokers and market makers earn their income.

Washington, DC

We will now have numerous hearings in DC to uncover the details and complexity of Robinhood’s decision. For the Reddit community, Robinhood has quickly emerged as a villain. Because of this, politicians who are diametrically opposed on everything else are now in total agreement.

For example, Congresswoman Alexandria Ocasio-Cortez (D-NY) and Senator Ted Cruz (R-TX) agreed that Robinhood was the latest Wall Street “suit,” as they criticized the trading restrictions on the retail community. Senator Elizabeth Warren (D-MA) added: “We need an SEC that has clear rules about market manipulation and then has the backbone to get in and enforce these rules.” Senator Sherrod Brown (D-OH), is the incoming chair of the Senate banking committee, and she said, “People on Wall Street only care about the rules when they’re the ones getting hurt…It’s time for the SEC and Congress to make the economy work for everyone not just Wall Street. That’s why, as incoming Chair of the Senate Banking and Housing Committee I plan to hold a hearing to do that important work.”

Why are hedge funds allowed to employ 10x leverage and short a stock towards 140% of its capitalization, while the retail community gets prohibited from even buying it? Should herd mentality, momentum or mob rule be curbed? Shouldn’t market forces be allowed to deal with supply and demand issues? Many are wondering why Robinhood and others placed restrictions on purchasing these stocks and have arrived at various conspiracy theories. Some believe Wall Street is protecting its favorite clients, i.e. hedge funds.

Mistakes

Robinhood was not the only online broker to restrict trading in these names, but it quickly became the poster child for how Wall Street suits and institutional players cater only to the rich, not the small, retail trader. Ironically, looking out for the little guy had been Robinhood’s entire marketing persona, which got crushed by this one decision. Robinhood’s stated goals of “democratizing finance” clashed with its decision to prevent the purchase of select popular stocks, exposing a hypocrisy of the global financial system. The retail trading world is now outraged at these perceived unfair trading limits.

With its enormous popularity, Robinhood’s private valuation has exploded higher. Over the last year or two, we have been offered the opportunity to purchase shares in Robinhood (in our hedge fund, the Manole Fintech Fund). Every year, we do a Gen-Z financial services survey on four distinct topics (banking, brokerage, payments and digital currency). Each and every year, our research finds that Gen-Z loves Robinhood and that they are taking material market share from more established incumbants. With our interns producing some excellent research, the question remains – Why were we not enticed to purchase Robinhood?

We have exposure to the growing online brokerage industry through other firms, but Robinhood seems to have struck a chord with the market, especially with Gen-Z. Has Robinhood developed a better mousetrap in the online brokerage world? What’s Robinhood’s real differentiation in the brokerage marketplace? Was it a mistake for us not to acquire a stake in Robinhood?

We struggle with this, because all brokers are now offering commission-free trading. Some others even offer best execution, access to independent research, as well as hundreds of physical offices to speak with a real-life person. With its recent bad publicity prohibiting its traders from buying GME, we aren’t ready to call this a error yet. But we are inclined to continue to study the growing importance of Gen-Z and their perspective on various segments of the financial service industry. This won’t be our last mistake, but maybe just the latest example.

We are reminded of a few quotes from investing legend Charlie Munger, regarding his errors. Munger said, “I rub my nose in my own mistakes. I try and keep things as simple and fundamental as I can. And I like the engineering concept of a margin of a safety. I’m a very blocking-and-tackling kind of a thinker. I just try and avoid being stupid.” He then added, “The single most important thing that you want to do is avoid stupid errors. Know the edge of your own competency. That’s very hard to do because the human mind naturally tries to make you think you’re way smarter than you are.” Charlie, we couldn’t agree more!

Robinhood

Robinhood now has over 13 million accounts and it opened over 3 million new accounts last year, primarily in the attractive Gen-Z and Millennials demographic. Its mobile interface has gamified (is that a word?) the stock market and excited many young investors.

By the end of last year, Robinhood’s mobile-first, easy-to-use platform was prospering. Many Robinhood investors have enjoyed the +70% bounce in the S&P 500 since its late-March low, and some are now utilizing margin loans, leveraged ETFs and options for the first time. Leverage is usually a tough lesson to learn, so we are closely watching how this turns out for many of Robinhood’s accounts, 50% of which classify as “first time” investors.

Robinhood is looking to capitalize on its success to fuel an appetite for an IPO. After securing $1.3 billion in funding in 2020, the implied valuation of Robinhood rose to +$11 billion. Early indications estimate Robinhood’s IPO value could exceed $20 billion, but this is moving wildly based upon the activity of the last week or two. We have heard that over 15% of Robinhood’s accounts have closed due to its handling of the GME issue. Only time will tell if a $5 million, 30-second Super Bowl commercial can heal some of Robinhood’s recent issues.

Leave a Reply