Article contributed by Rodolfo “Rudy” Amoresano, Co-Founder and Managing Partner of Ukraine Finance Partners.

A resounding “YES” is our answer.

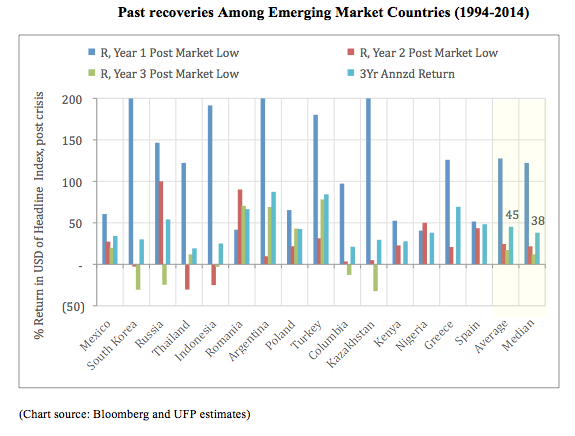

Experienced emerging markets professionals seeking to deploy capital in special situations and distressed assets have always looked to take advantage of financial turmoil.

Emerging markets have experienced their fair share of crises in recent history; from the mid 1980’s LDC defaults, the Mexican Tequila crisis, Asia, Russia, Argentina, Greece… and now Ukraine. During these events, capital outflows are fast, indiscriminate and continuous, asset prices collapse and value is ignored. Ukraine reached this point in 2015-2016 and during the past 2 years started a recovery process.

Ukraine is a country of 45 million people, highly educated, abundant rich soil (“Breadbasket” of Europe”), with excellent geographical position and great IT resources and potential.

Why do we think Ukraine will succeed?

1. The people demand it: it is hard not to experience their commitment and harder to imagine that the Ukrainians that made the ultimate sacrifice for a better country will be rapidly forgotten.

2. Clear sense of what needs to be done: the country needs to continue to implement reforms, they need to attract capital for their rich country to truly prosper.

3. No other option: Ukraine needs financing and the West will only provide it if progress continues. The East is not an option for finance.

4. Willingness of the West to continue its support: in the geo-political field, Ukraine is of great importance. The West will continue its support as long as Ukraine does its part.

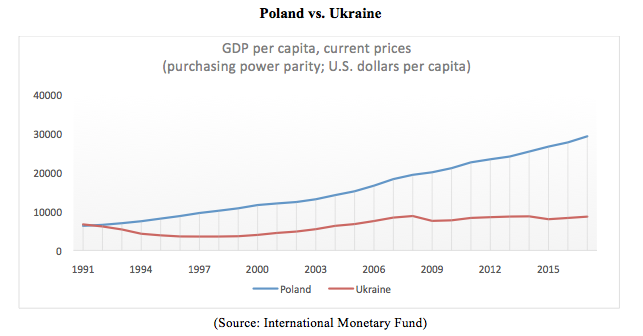

5. A clear view of Ukraine’s potential: Since the collapse of the USSR, Ukraine and Poland, which started relatively from the same macro-economic point, have significantly diverged with Poland integrating to the West and Ukraine remaining under the Eastern/Soviet influence. Today’s Poland GDP per capital stands at $29,251 while Ukraine languishes at $8,656.

Ukraine can be proud of the following achievements during the past 4 years:

· Free elections

· IMF agreement and several disbursements

· Sovereign Debt restructuring

· Continue support from the IFIs

· Reform progress

· Visa entry to EU

· Re-entering the capital markets:

· Moody’s upgrade to Caa (positive outlook) and Fitch and S&P’s both upgrade to B-, with stable outlook.

· A significant improvement in the macro position

BUT a lot needs to be done; anti-corruption reform, privatization… and let’s not ignore the Russians (the top or one of the top issues raised by investors).

We believe that the conflict will continue, unsolved but manageable, for the foreseeable future. We do not envision a scenario where the Russian presence is increased due to three main reasons:

1. The Ukrainian army is much stronger; thus, the cost of any advance would be costlier;

2. There are international observers in place, thus the world will know “live” who is invading whom;

3. The initial effort in the East and Crimea failed to gain support in Ukraine and instead united the country against the Russians.

How should exposure to Ukraine be allocated: debt, equities, private transactions?

First, Emerging Markets are different from developed markets. In developed countries, assets classes can move in opposite ways under severe economic strain. During the recent 2008 financial crises, the USD rallied, treasuries rallied, while corporate credit and equities collapsed. In EM when an economy collapses all asset classes collapse. The opposite is also true, when a country is in recovery, all asset classes recuperate. Given that all asset classes in EM have some common risk denominators, we employ a Capital Structure approach to the country; we choose the asset class(es) that provide the higher returns for the given common risks.

Second, exposure to Ukraine has the benefit of being uncorrelated to global markets, and stands to benefit from the progress in anti-corruption, success of privatizations, cleaning of Non-performing loans in the banking system and the willingness to join the EU.

Finally, we believe investors should employ an investment rather than a trading strategy to capture Ukraine’s turnaround.

Our view on asset classes in Ukraine today:

· Sovereign debt: although we are very optimistic about Ukraine, sovereign debt has little upside (unless an unlikely and significant yield compression takes place) and has the potential to suffer significantly if progress in UA slows down or gets volatile.

· Equities: they are extremely illiquid, there are very few stocks to buy, and control over the business is limited. A negative event or just increased political volatility can produce significant losses added to the inability to exit or at a minimum get significant carry (dividends).

Private transaction: these include mezzanine debt, convertibles, private equity and specific projects. These are the type of investment we believe can protect in case of negative news

· while at the same time present significant upside. We like to position our investment to provide good current yields, downside protection and only participate if we can monitor operational and financial aspects of the business. We insist in the latter to be partners in the venture and be able to bring our know-how, contact and other expertise to increase the probability of success.

Two types of businesses that merit consideration:

· Solar energy: Ukraine is in desperate need of more energy and better-quality energy. Some of the highest subsidies are in place due to the importance of the sector and, if desired, political insurance is available. Excluding political risk, leveraged IRRs in the 25% (in USD) range are reasonable.

· Small-medium size enterprises (“SMEs”): the outflow of capital and the collapse of the banking system have left SMEs starving for financing. Capital may be deployed with adequate current yields, significant upside, the ability to monitor all aspects of the business only to individuals/businesses that meet our western-style stringent requirements. IRR’s in the 25% (in USD) range are reasonable.

The author: Rodolfo “Rudy” Amoresano is Co-Founder and Managing Partner of Ukraine Finance Partners and has over 30 years of experience in emerging markets including during all of the crises since the mid-80’s.

Leave a Reply