Guest post contributed by Warren Fisher of Manole Capital Management, LLC. You can read Part 1 here.

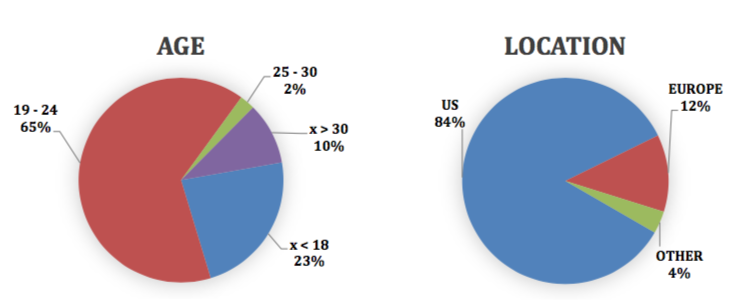

In January and February of 2018, Manole Capital conducted a financial services survey specifically targeting the thoughts and opinions of millennials. Over 175 individuals participated, with nearly 90% under the age of 24 years old. 65% were between the age of 19 and 24 and 23% were 18 or younger. In terms of demographics, 84% were from the United States and 12% were from Europe. For additional information about our survey audience, please contact Manole Capital directly.

Series #2: Cash

In his life of crime, bank robber Willie Sutton made off with an estimated $2 million dollars of ill-gotten gains. He was a resourceful robber, using disguises and dressing like a policeman, window washer, maintenance man and even a bank guard. His famous quote for why he constantly robbed banks was “That’s where the money is.”

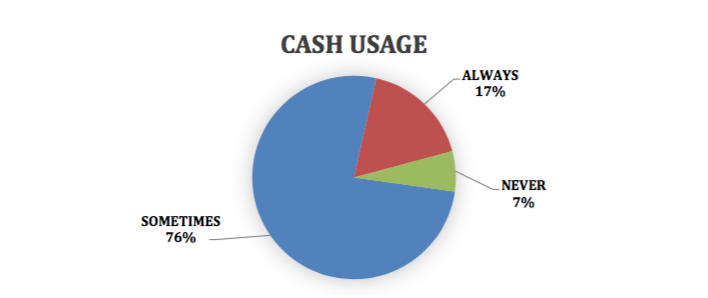

Our second series of questions revolved around millennials thoughts and use of cash. Over 75% of those questioned still “sometimes” use cash. More surprising to us, is that nearly 1/5th of millennials choose to “always” use cash. We continue to use less and less cash in our daily lives, but there is still a decent percentage of millennials that choose to solely rely on cash. Interesting…

“No Cash Accepted”:

In June of last year, we published a note titled “No Cash Accepted”. To read that note, just click here or visit our website at www.manolecapital.com, under the “Research” tab. Our grand takeaway was the secular growth of electronic or digital payments is an unstoppable force across the globe. We discussed the declining trends in cash usage and detailed how more and more retailers were choosing to not accept cash.

We highlighted that cash usage has a cost and that some individuals were continuing to use cash for illicit economic activity and to bypass taxes. We highlighted 5 key drivers for electronic payment growth, which were the displacement of cash and check, the proliferation of eCommerce, the inability of banks to serve all clients, an increase in merchant acceptance and the growing availability of new market channels. We provided rationale why these factors gave us confidence in the future growth of electronic payments. With nearly 20% of millennials choosing to use “only cash”(per our survey)… could we be wrong?

Secular Growth:

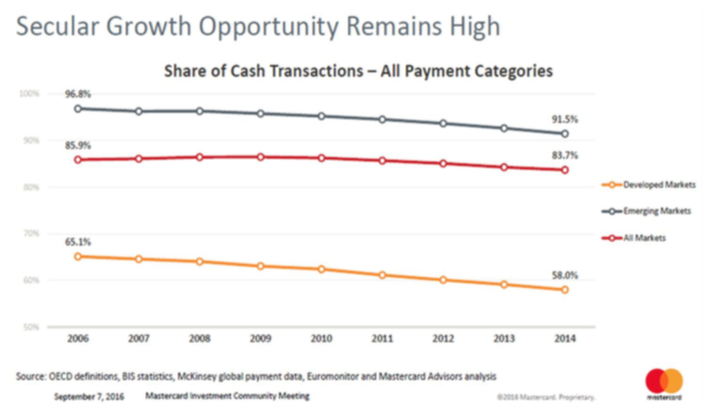

As the chart from Mastercard and McKinsey below indicates, the secular growth of cards and digital payments remains high. Over the last decade, and across all markets and categories, the share of cash transactions has declined from 86% to under 84%. This is not massive shift, but a slow and steady migration away from cash and towards cards and digital payments. The shift is more pronounced in Emerging Markets, but even Developed Markets are surprisingly still cash centric.

We asked our group of 5 University of Tampa interns / students their thoughts on this surprising response. They came back with a few key reasons that “cash only” could have been chosen. First, some students do not have traditional bank accounts and some do not have access to debit and credit cards. Currently, there are 2.5 billion people underserved by banks, with 1 out of 13 US households still not using a bank (per a recent US Federal Reserve study). Over the next few years, as these students graduate and get employment, many will join traditional financial institutions.

Secondly, some students simply prefer to use cash to better monitor their cash flow. Historically, students would employ credit and rack up significant debt. More and more students are choosing to utilize cash and to only spend what they have. This helps them stay away from credit cards and its potentially dangerous debt spiral. This is often cited as the same reason people are gravitating towards debit. Debit card usage continues to steadily climb, and it is an excellent, more modern-day version of cash.

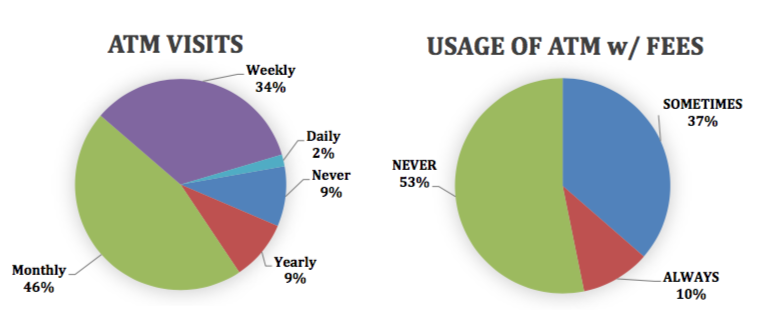

ATM Visits:

In the US, there are currently 425,000 ATM machines. For perspective, the US is roughly 15% of the world’s 3 million ATM’s. In the US, roughly half of ATM’s are owned by financial institutions and the other half are independently owned. By our logic, if cash usage was growing and becoming more important to millennials, ATM visits would need to be rising.

Our survey results found that over 18% of millennials either never go to an ATM or go only once a year. The largest percentage, at 46%, visit an ATM every month. We believe this is not terribly different that our own usage of cash and a ATM. What is somewhat surprising, especially considering the fees associated with ATM usage, was over 1/3rd of millennials visit an ATM every week.

Our next question asked attempted to address the issue with fees. We asked how often you use an ATM where you must pay a fee. The answer was quite clear. Over 1⁄2 of millennials refuse to pay a fee when using an ATM. These results give us some comfort that cash usage is not a millennial trend to necessarily ruin our secular growth of digital payment theme. Instead, these results can be explained away with logical dialogue with our interns and understanding where those surveyed are in their lifecycle.

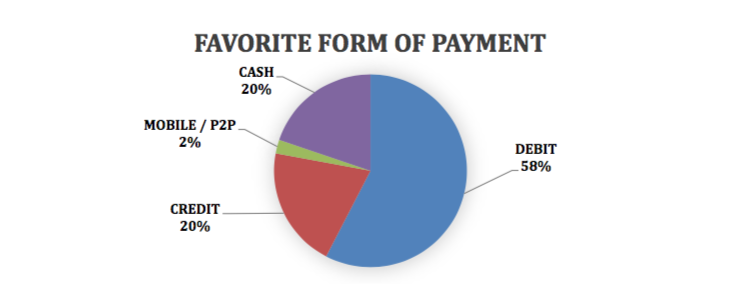

Favorite Choice of Payment:

Our favorite question in this survey was “What is your preferred choice of payment?”. With over 40% of our FinTech portfolio exposed to the payments industry, this clearly had the potential to impact our thinking. In fact, as of the end of February, our portfolio was had 21% exposure to “Payment Networks” and 20% exposure to “Acquirers and Processors”. The results of this question were quite surprising to us.

Debit at 58% was high and, in our opinion, somewhat expected. As we mentioned above, debit can be a wonderful way to monitor cash flow and keep debt from escalating. With 20% choosing credit, that brings card usage to over 3⁄4 of millennials favorite form of payment. This is wonderful to hear for our portfolio and its large percentage exposure to the payments industry.

The surprising answers, at least to us, was the very low mobile and peer-to-peer percentage at only 2%. While nobody selected pre-paid as their favorite form of payment, we were anticipating more millennials would prefer to use their mobile phones and/or P2P payments. Maybe millennials aren’t that dis-similar to older generations as we thought?

Once again, we are surprised with 20% selecting cash. Just like the stubbornly high percentage of purchase transactions that continue to occur in cash, some millennials prefer physical currency. Couple this with the 17% of millennials that “always” use cash and one can expect physical currency to be around for decades to come. We certainly take note of this trend and it will be something we continue to monitor. Either way, cards are the dominant and favorite form of payment for millennials. We believes this bodes well for our FinTech portfolio.

Cash Conclusions:

Our belief is that electronic payments are a wonderful, long-term growth opportunity. Cash will likely be in existence for years to come, but its use is experiencing a slow and steady decline. Some older generations fear advances in technology or worry about electronic fraud, but it appears that millennials have some of those same fears. There is little doubt that mobile phones and cards will continue to steal market share from cash, but even millennials continue to use cash at a surprising rate. Even as smartphones become more prevalent, more and more purchase transactions are going from cash and check to cards and not necessarily mobile phones. With the advent of easy- to-use, peer-to-peer apps, we would have thought that cash usage would be the least preferred method of payment for those surveyed. Instead, cash is holding steady and indicates that the growth opportunity for mobile and P2P might be slower than we initially believed.

Our next few surveys will be published shortly. Questions asked will focus on mobile payment usage and peer-to-peer payments. Following Series #3, our last note will discuss brokerage accounts, bitcoin thoughts and cryptocurrencies.

Disclaimer:

Firm: Manole Capital Management LLC is a registered investment adviser. The firm is defined to include all accounts managed by Manole Capital Management LLC. In general: This disclaimer applies to this document and the verbal or written comments of any person representing it. The information presented is available for client or potential client use only. This summary, which has been furnished on a confidential basis to the recipient, does not constitute an offer of any securities or investment advisory services, which may be made only by means of a private placement memorandum or similar materials which contain a description of material terms and risks. This summary is intended exclusively for the use of the person it has been delivered to by Warren Fisher and it is not to be reproduced or redistributed to any other person without the prior consent of Warren Fisher. Past Performance: Past performance generally is not, and should not be construed as, an indication of future results. The information provided should not be relied upon as the basis for making any investment decisions or for selecting The Firm. Past portfolio characteristics are not necessarily indicative of future portfolio characteristics and can be changed. Past strategy allocations are not necessarily indicative of future allocations. Strategy allocations are based on the capital used for the strategy mentioned. This document may contain forward-looking statements and projections that are based on current beliefs and assumptions and on information currently available. Risk of Loss: An investment involves a high degree of risk, including the possibility of a total loss thereof. Any investment or strategy managed by The Firm is speculative in nature and there can be no assurance that the investment objective(s) will be achieved. Investors must be prepared to bear the risk of a total loss of their investment. Distribution: Manole Capital expressly prohibits any reproduction, in hard copy, electronic or any other form, or any re-distribution of this presentation to any third party without the prior written consent of Manole. This presentation is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use is contrary to local law or regulation. Additional information: Prospective investors are urged to carefully read the applicable memorandums in its entirety. All information is believed to be reasonable, but involve risks, uncertainties and assumptions and prospective investors may not put undue reliance on any of these statements. Information provided herein is presented as of December 2015 (unless otherwise noted) and is derived from sources Warren Fisher considers reliable, but it cannot guarantee its complete accuracy. Any information may be changed or updated without notice to the recipient. Tax, legal or accounting advice: This presentation is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Any statements of the US federal tax consequences contained in this presentation were not intended to be used and cannot be used to avoid penalties under the US Internal Revenue Code or to promote, market or recommend to another party any tax related matters addressed herein.

Leave a Reply