Contributed by Roy Studness, Portfolio Manager, Studness Capital Management.

Bank and electric utility stocks fit very well together in a portfolio because they are both sensitive to changes in interest rates, but in opposite ways. More specifically, bank and utility stocks move in opposite directions to changes in interest rates – banks generally respond positively to a rise in interest rates, while utility stocks respond negatively – producing a natural hedge. This enables the construction of portfolios that perform well across a broad range of market settings (such as economic expansions and contractions) and provide superior long-term performance.

In addition to the negative correlation between bank and utility stocks, the two industries provide essential services which if these services are interrupted then society suffers. Moreover, these industries are highly regulated which lowers the risk. This allows investors to build portfolios with exceptionally low fundamental business risk which supports more concentrated portfolios.

Opposite Price Movements

Bank and electric utility stocks move in opposite directions to changes in interest rates. Bank stocks respond positively to higher interest rates because the higher rates improve, in the short-term, profitability for many banks as loan rates generally reprice faster than deposits. At the same time, however, higher interest rates cause utility stocks to decline because investors treat utility stocks as bond proxies. So, as interest rates increase investors have more alternatives to get yield, so investors sell utility stocks regardless of the underlying fundamentals.

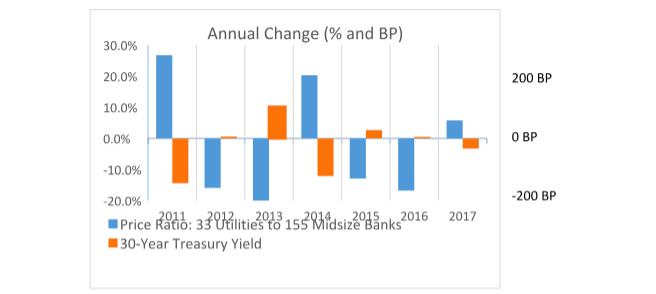

The divergent stock price movements of bank and utility stocks with changes in interest rates can be seen in the following chart comparing changes in the 30-Year Treasury yield with the ratio of the 33 electric utility stock prices to bank stock prices for 155 midsize banks. For example, during 2011-17, a 100 basis point rise/decline in the 30-year Treasury yield typically produced a decline/rise in the utility/bank price ratio of 20% (midsize banks are used to avoid skewness from the large money center banks).

There are two important implications from the divergent price movements of bank and utility stock prices. First, the divergent price movements mean that there are likely always attractive stocks between these two industries. This allows a portfolio manager to specialize on covering fewer stocks but really maintain an expertise in those areas since one of these two industries is usually providing attractive investment opportunities at a particular time. Second, the divergent price movements of bank and utility stocks tend to be greater than the changes in the underlying fundamentals of the companies, which creates mispricings that result in attractive investment opportunities. For example, utility stock prices invariably decline as interest rates increase (as they have been in 2018) because investors treat high-yielding utility stocks as bond proxies and sell the utility stocks as investors have more yield alternatives. At the same time, however, the underlying fundamentals for the electric utility industry have been very strong in recent years and the outlook is for them to remain strong for at least the next several years, if not longer. So, this can create a dynamic where utility stock prices decline due to increasing interest rates in the face of strong underlying fundamentals – a recipe for good investment opportunities.

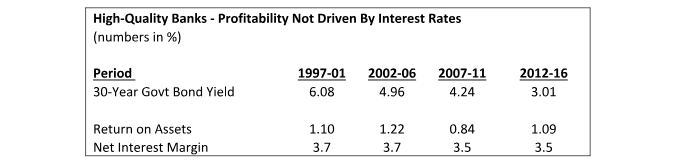

Over the long-term, however, fundamentals for banks and utilities are not determined by interest rates but rather by regulatory outcomes (for utilities) and management acumen (for banks). For utilities, rates are adjusted through rate case filings to adjust for changes in interest rates. For banks, the impact of interest rates is mitigated by competitive forces and it is up to management to successfully navigate the bank to high returns. This dynamic is seen in the table below which examines how “high-quality” banks (defined as banks that consistently earn above 8% ROE) perform over time under different interest rate environments. As the table shows, as interest rates declined significantly over the past twenty years, high-quality banks managed to maintain consistent profitability.

Opportunities in Varied Markets

The divergent stock price movements of bank and utility stocks to changes in interest rates also suggests that investors can construct portfolios that will do well in a variety of economic scenarios with only focusing on these two industries. For example, bank stocks tend to perform well in an economic expansionary environment while utilities are viewed as more defensive and tend to do well in a contracting economic environment.

Low Risk Industries

An important feature of both the bank and utility industries is low risk. More specifically, both industries are highly regulated and provide essential services. In fact, utilities are regulated monopolies which limits the stock downside. Banks, however, are not monopolies and they are subject to intense competition (banks can and do fail). Investors can reduce the risk of owning bank stocks by focusing on those with long track-records of outperformance in terms of profitability and credit quality. The banks with these characteristics tend to have some niche element to their business model that helps insulate them from competitive forces. These niches can vary from product-focused (catering to a particular industry), demographic-focused (catering to an ethnic community), to service-focused (providing a unique service level).

Low Risk vs. Volatility

The low risk nature of the bank and utility industries also allows stocks within these industries with very low long-term fundamental business risk. It is important to distinguish fundamental business risk from stock price movements. Just because a company’s stock price has short-term volatility (and a high standard deviation) does not, by itself, mean that the company itself is risky. As noted earlier, stock prices may move for non-fundamental reasons – such as changes in interest rates – that do not correlate to a company’s long-term operational performance. For example, as noted above, while utility stock prices typically decline when interest rates increase (since investors treat utility stocks as bond proxies), the higher rates actually do not have a significant impact on the utility’s long-term performance because the utility’s rates are adjusted for the higher cost of capital in its subsequent rate cases. So, in the long-term, the fundamental performance of utility companies is not impacted by interest rate movements but in the short-term utility stock prices are significantly impacted by changes in interest rates as investors treat utility stocks as bond proxies.

Concentrated Portfolios

Finding companies with exceptional low long-term risks allows investors to construct more concentrated portfolios. Modern portfolio theory instructs that risk is reduced by owning a large number of stocks. That premise, however, assumes that stocks have similar risk but if one can find stocks with below average risk then the risk reduction benefits of diversification can be achieved with fewer stocks.

Conclusion

Banks and utilities are two industries that provide great long-term investment opportunities because: (1) opposite price movements of bank and utility stocks to changes in interest rates create mispricings; (2) bank and utility stocks tend to well in different economic environments; and (3) both industries have low fundamental business risk which can support more concentrated portfolios. These dynamics provide the foundation for superior long-term portfolio performance.

Leave a Reply