Guest post contributed by Warren Fisher of Manole Capital Management, LLC.

With the flurry of recent political advertisements on TV, we wanted to write a note outlining our short and long-term perspective on the market.

Macro vs Micro Analysis:

Taking a rare macro perspective, we are firm believers that stocks are generally not influenced by one single factor. We have found that there are a host of elements that push and pull stock prices up or down. It is our opinion that earnings are the best gauge for the health of a business and each quarter can serve as a tailwind driving value. In addition to providing details and insights into the fundamentals of a business, quarterly earnings calls afford us, as shareholders, a tremendous amount of transparency. In addition, there are leading economic indicators that assist our analysis and can boost investor sentiment and the relative attractiveness of a stock. It is this confluence of factors that determine the direction of stock prices.

In the past we have opined on tariffs and geopolitical issues, not because we have tremendous insights into their origin, but because these matters tend to impact momentum or cause negative market movements. Often, these matters add tremendous uncertainty into the markets and are a short-term headwind.

Since 2016, we have stated clearly that we will be politically agnostic in our research. Instead of providing commentary that favors one party over another, our main concern is with policy and how it impacts corporate profits and economic growth.

Midterms:

When we were in high school and college, midterms always created some unwanted anxiety. Tests were upcoming, and one’s needed to study and be prepared. We view the political election midterms in much the same way. For the last 6 months, the media has been intently discussing and debating the midterm elections. While we will not attempt to forecast individual, competitive races, we would like to address the market impact of these battles.

The facts are that the president’s party has lost House seats in over 90% of the last 20 midterm elections. Not surprisingly, as Washington’s balance of power undergoes a potential shift in midterm election years, the stock market has historically gotten jittery. We believe that uncertainty can be capitalized upon and no matter what the ultimate outcome is, the best strategy is to stay steady and maintain your investment process, strategy and philosophy.

Volatility:

Not to sound like a broken record, but we continue to expect and anticipate higher volatility. The market experienced a jolt in late January, early February, when the “short vol” trade corrected. While we are not predicting another shock like that, we do envision volatility to steadily increase.

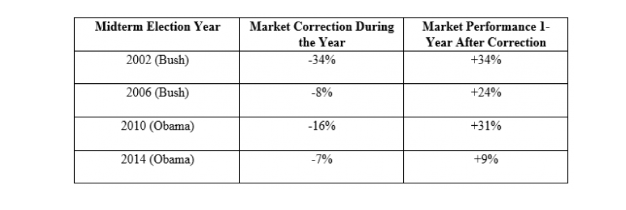

While 2017 was a wonderful year for the S&P 500 (up 21%), 2018 has been much more volatile and uncertain. Year-to-date, the S&P 500 is up 7%. As the chart above highlights, during midterm election years, market corrections occur, and volatility rises. According to Strategas Research, going back to 1962, the average correction during a midterm election year was quite high, down -19%. If one looks at the 6-months pre-midterms (i.e. April to September), the average monthly returns of the S&P 500 have been negative. This seems somewhat “normal” to us, as uncertainty in Washington and what policies will arise, cause the market to take pause.

Quite simply, uncertainty is not a friend of the stock market. When one adds economic issues to that tentative political mix, it is no wonder the market seems skittish. What will happen with Trump’s tariffs and trade battles? Are emerging markets, like Turkey, strong enough to withstand massive currency movements? Will Congress enact new laws or policies in the run-up to any political or power shift? All of these questions increase uncertainty.

We are bracing for a noisy and ugly fight during this midterm election cycle, including comical “mudslinging” and political ads stretching the truth. The midterms should create some headwinds for stocks, but we continue to focus on the positive news surrounding corporate earnings. The job market remains robust, incomes are growing, consumer sentiment is strong, and all of these support a longer-term positive trend.

Follow Through:

When the dust begins to settle, the market will begin to assess winners and losers. As the last column on the chart above shows, the stock market likes the certainty of knowing midterm election results. In the year following the midterms, and often nasty corrections, the stock market tends to move materially higher. Once again, going back 1962, the average lift for stocks following that midterm correction was an impressive +31%. Once the political environment is better understood, the market can begin to focus again on individual business fundamentals.

Bottom line, stocks will likely pause pre-midterms, with heightened uncertainty. Volatility will rise during this period, but post-midterms certainty should benefit equity markets. Once midterm elections happen, and the market gets comfortable with what it can expect from Congress, uncertainty will fade. Corporate profits will become the primary driver of returns. Why are we so bullish? History is a decent guide. Since 1946, the S&P 500 has not declined in the 12 months following a midterm election. In addition, the average return in the year following a midterm election (i.e. from 1950 to 2014) is an impressive +15%. So why would we expect 2019 to be different, especially when the underlying fundamentals of many of our companies remains strong.

Conclusion:

As we mentioned earlier, stock prices are influenced by several factors. History has shown that corrections are to be expected in midterm election years, but they are typically followed by positive returns. We think positioning to capture the benefits of rising volatility, as well as the certainty following midterm results is key to success.

Leave a Reply